Sabitlenmiş Tweet

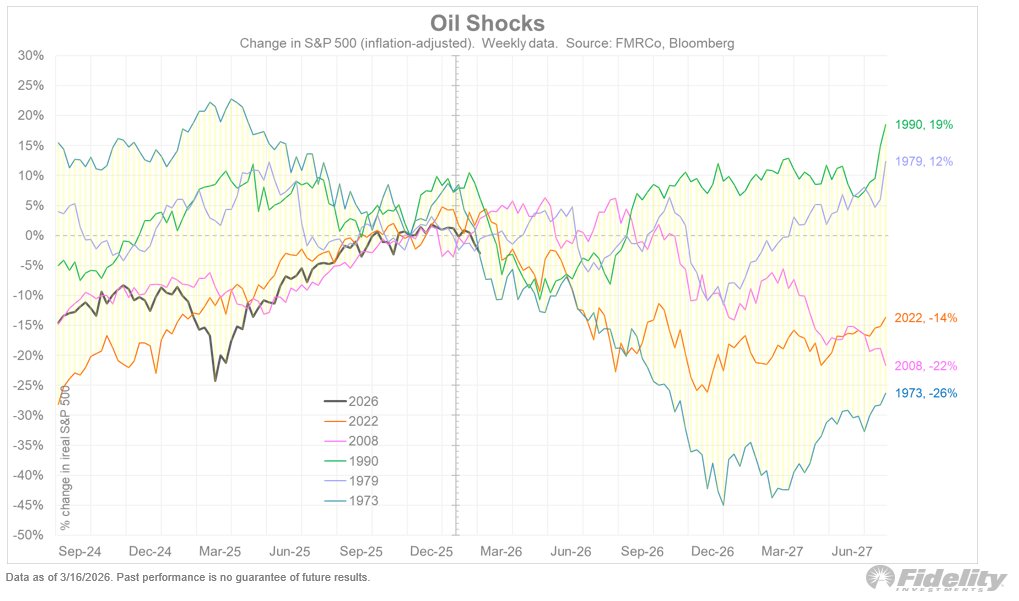

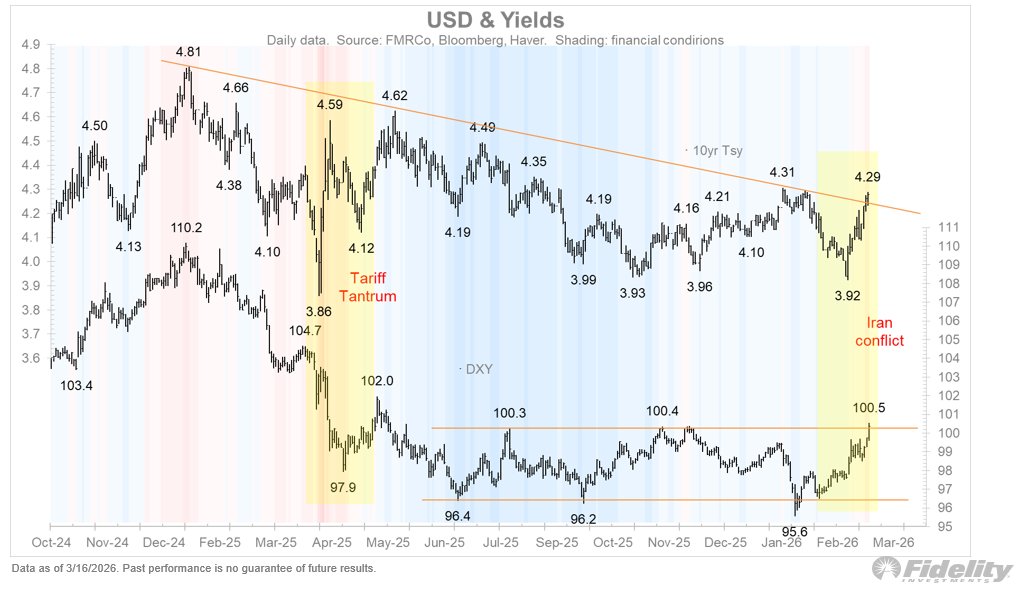

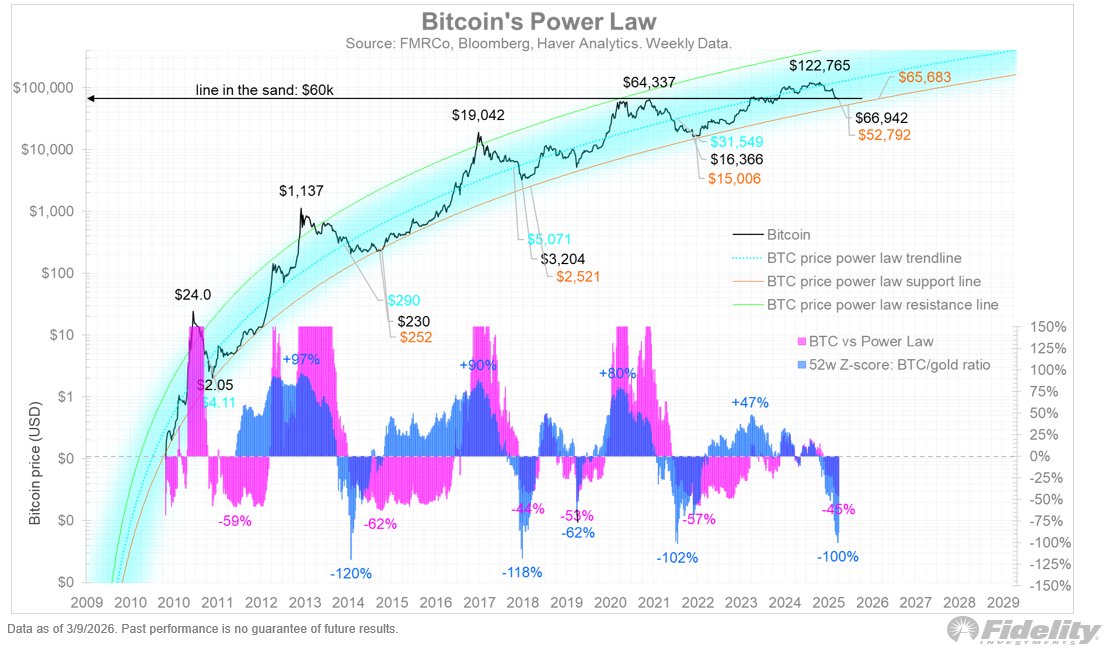

Week 3 is about to get underway for the conflict in Iran, and while we track the traffic through the Straits of Hormuz, we can see some interesting patterns emerging. Some are predictable, like spiking oil prices, rising vols, and downward pressure on risk assets, but others are less expected. Bond yields are up and so is Bitcoin. What does this tell us? We technicians know that when something is supposed to happen but isn’t (or vice versa), there might be a story there. If an oil shock leads to demand destruction, yields should fall instead of rise, while looking past the temporary hit to inflation. And Bitcoin should fall if given its “Dr. Jekyll & Mr. Hyde” personality it acts like a risk asset. But neither are happening.

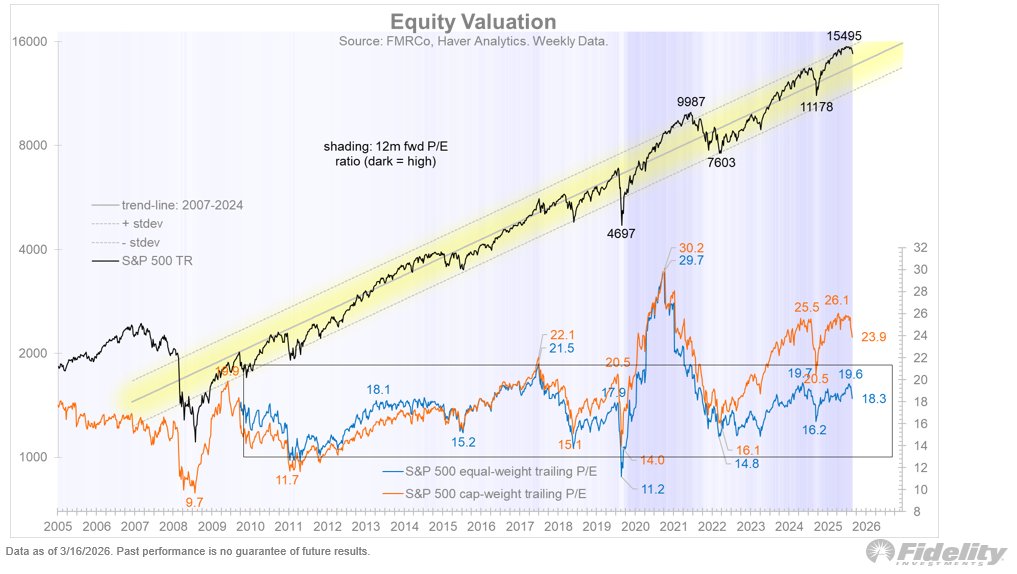

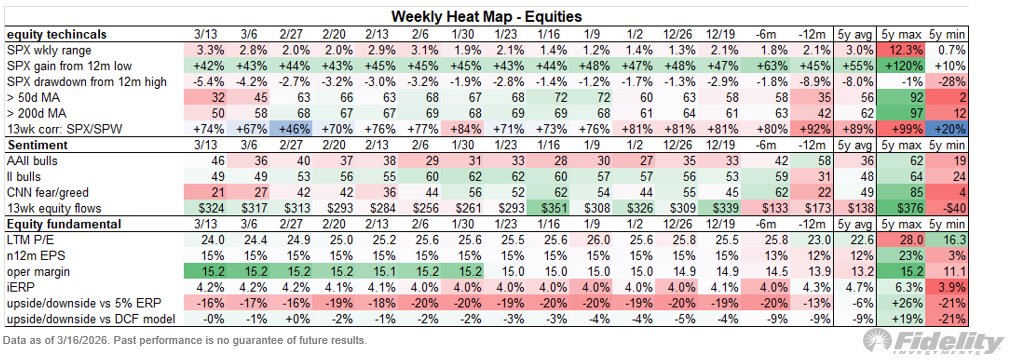

Meanwhile, credit remains under pressure as the crowded but illiquid software/SaaS space is on the hitlist for AI disruption. And while the equal-weighted S&P 500 is not extended on either a price or valuation basis, it may not matter much if the Mag 7 cannot hold support at current levels.

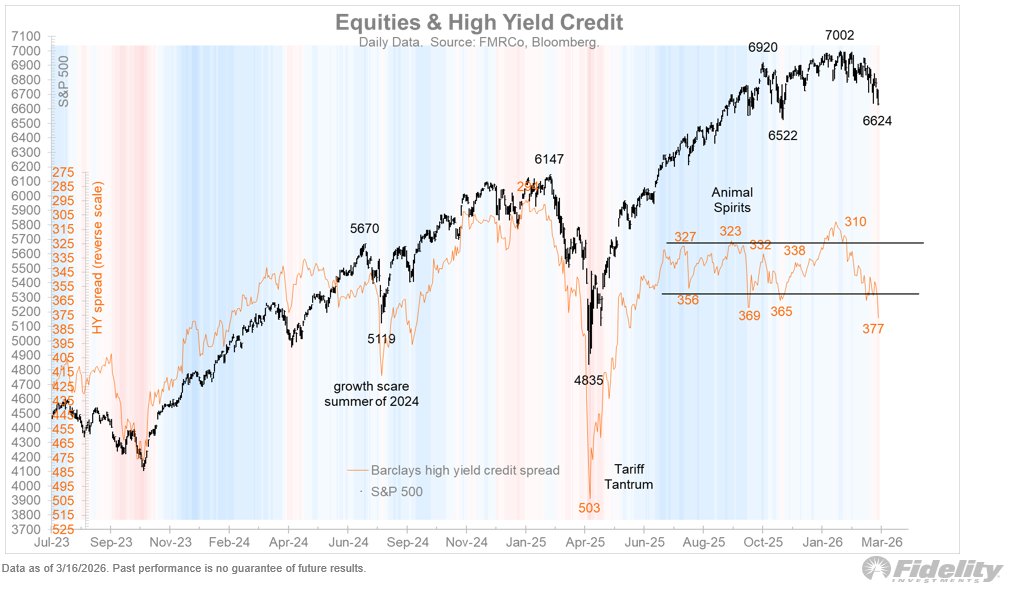

For now, the S&P 500 remains eerily well-behaved with a drawdown of only 5%, but that’s a bit of an illusion. Because earnings are so strong, the modest drawdown is masked by the fact that the P/E ratio is down 11% from the high. That’s probably a better drawdown metric than price.

Let’s explore.

linkedin.com/pulse/tangled-…

English