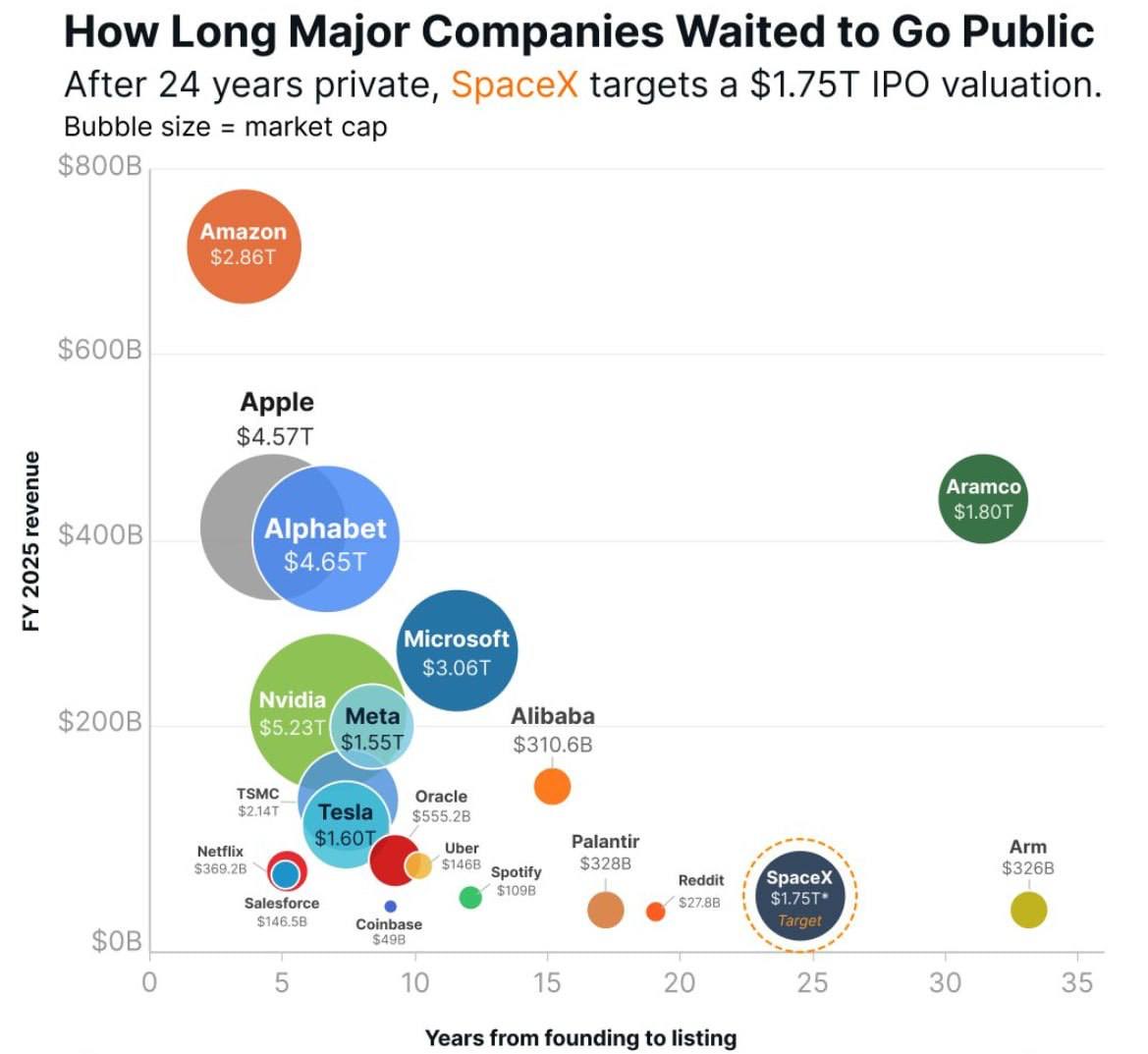

#SpaceX IPO Update

SpaceX (after merger with xAI) is preparing for an IPO in June 2026 with a target valuation of $1.5–2 trillion — potentially the largest in history.

2025 financials:

• Revenue ~$18.7B (+33% YoY)

• Starlink (connectivity): $11.4B (~61% of revenue) — main growth and profit driver

• Launches & government contracts: ~$4B

• AI/xAI: ~$3.2B (still unprofitable)

Starlink has >10M subscribers, but ARPU is declining as it expands into mass markets.

At $1.75T valuation, SpaceX would rank in the global top 10, close to Tesla (~$1.6T), but far behind Nvidia ($5T+), Alphabet, and Apple. The P/S multiple is extreme: 90–125x 2025 revenue.

**Bull case:** Starship succeeds, radically lowers launch costs, Starlink becomes a global monopoly with direct-to-cell, new markets (orbital data centers, point-to-point transport). Musk premium + AI/space hype could drive a massive initial pop.

**Bear case:** The valuation assumes decades of 40%+ CAGR — almost unprecedented. High capex, regulatory risks (FAA/FCC), competition (Amazon Kuiper, China), and AI losses could lead to a sharp correction.

For the valuation to hold post-IPO (and survive 2–3 month lock-up):

- Successful Starship tests + rapid reusability

- Starlink subscriber growth to 20M+ by end-2026 + margin stabilization

- Bullish tech/AI market sentiment, no recession

- Strong execution and clear “platform company” narrative

Conclusion: The IPO will likely be hype-driven (private market already values it at $800B–$1.25T). But sustaining it will be very difficult without concrete Starship progress. Classic high-risk “story stock” — huge upside if everything clicks, 30–50%+ downside if it doesn’t.

Focus on execution, not just vision.

#SpaceX #SPCX #Starlink #Starship #IPO #cryptocurrency

English