Keith

1.9K posts

Keith

@Trader_Keith

Faith/Family/Markets/Investing - buying high quality businesses is key to long term compounding! Posts are personal; not investment advice.

West Coast, Canada Katılım Aralık 2009

148 Takip Edilen296 Takipçiler

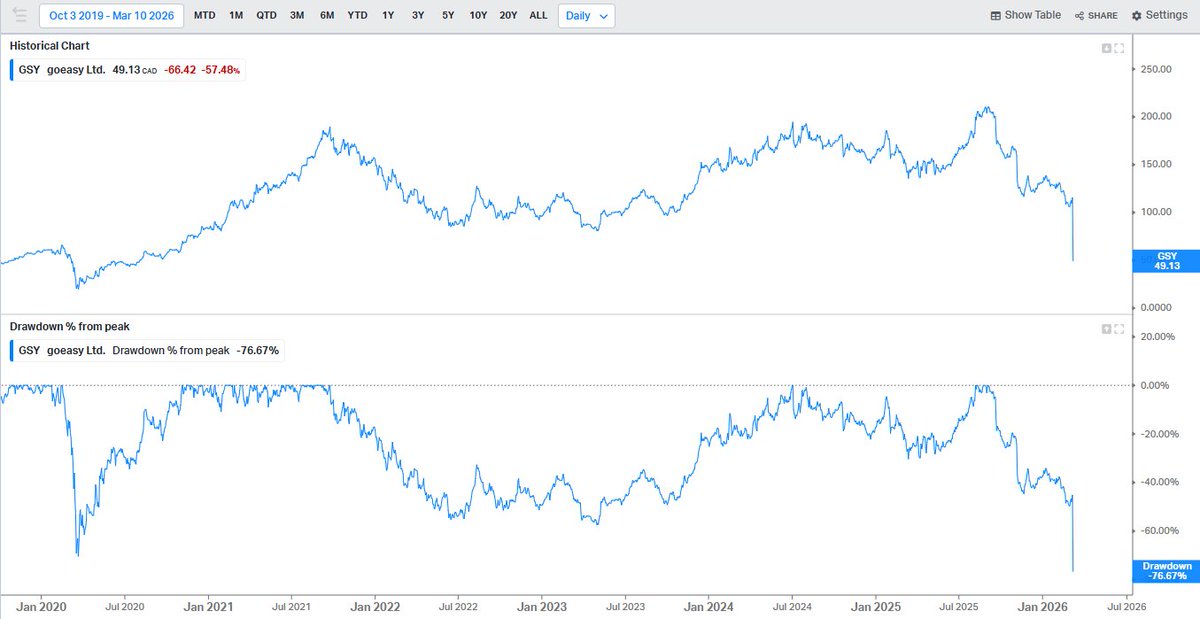

We are short goeasy $GSY, a Canadian subprime lender with easy to borrow stock. Below is a summary of the key opinions in this idea; for the full short thesis including a downloadable PDF, please see the Jehoshaphat Research website.

1) Investors believe GSY has a “secret sauce” of novel, brilliant underwriting. We agree – well, sort of. The secret sauce is accounting, rather than underwriting, creativity. A number of aggressive accounting policies and rule changes have massaged charge-offs, delinquencies, opex, earnings and ROE into more favorable-looking short-term performance.

2) We believe the combination of all these accounting shenanigans has inflated pre-tax earnings by hundreds of millions of dollars, and has delayed a similar amount of charge-offs into the near future. We estimate a ~$300m “snowball” of charge-offs that has been rolled up and will start melting all over the balance sheet in the next few quarters.

3) While an X post doesn’t lend itself to a full laundry list of accounting games (see our full PDF for all these opinions), one that lends itself well to a single image (see below) is GSY suddenly "deciding" to no longer charge off deadbeat car loans at 180 days past due. You can see the immediate effect of this decision on charge-off numbers. This is a great way to be able to tell investors that charge-offs are coming down. And technically, they are!

4) Another fun one: GSY appears to have “re-bucketed” ~8% of its loan book into a lower-risk category, despite no apparent change in credit score. This would probably explain a crash in a key loan loss provision rate in the exact same quarter and since, which we identified by comparing several years’ worth of such data.

5) Why doesn’t anyone talk about unpaid interest receivable at this company? We’ll start the conversation: It’s exploding and it may be the single most useful indicator of borrower stress at GSY. This explosion contrasts sharply with relatively muted past due rates, but dovetails perfectly with the idea of tons of “hidden” past-dues.

6) Investors like GSY for its high reported ROE, of course. But you can scrub the ROE to remove the effect of all these accounting changes and irregularities, and if you do that, you’ll find a business that isn’t even earning its cost of capital. This is to say nothing of the high likelihood of GSY missing earnings dramatically in the coming quarters from all these artificially delayed credit losses. Whether event-driven or deeply fundamental and long-term, there are good catalysts to make this short work.

7) GSY appears to have stopped its vaunted buyback in mid-April, based on daily SEDI data. Maybe that’s just because they think the stock is too expensive...or maybe it’s because their debt level is overextended at the worst possible time, with the company staring down a “backlog” of unreported charge-offs? Whatever it is, pausing the buyback for 5+ months blows up the capital return narrative that certain investors own GSY for.

8) If you follow GSY, you know that the CFO just put in his (short) notice last week. You also know that the longtime CEO resigned from that role at the beginning of this year. Both of these gentlemen pursued unusual stock sales before doing so. This is probably what you’d do too, if your job were soon going to entail having to explain where all these "surprise" charge-offs were coming from. (Maybe this is why GSY hasn’t been able to identify even an interim CFO yet, let alone a permanent one.)

Go ahead and ask the sell-side analysts about this one if you’re inclined, but be prepared to explain a lot to them if you do. 8 out of 9 covering analysts have a “Buy” rating on this sublime subprime lender, so they probably haven’t been exposed to a lot of debate about it before.

We always leave some of the more interesting things for readers of the full report, so we encourage you to visit our website and download the full PDF of our short thesis, paying attention as well to our very important disclaimer. Comments and corrections welcome at our website or our email address.

English