@shome_rajarshi Hi raj , how do you see MTAR , high growth , great sector TAM and moated company but valuation also highly rich

English

Tribhav Chaudhary

1.1K posts

@TribhavC

Btech - NIT ALLAHABAD (MNNIT) , stream - information technology , software engineer , trader , investor .

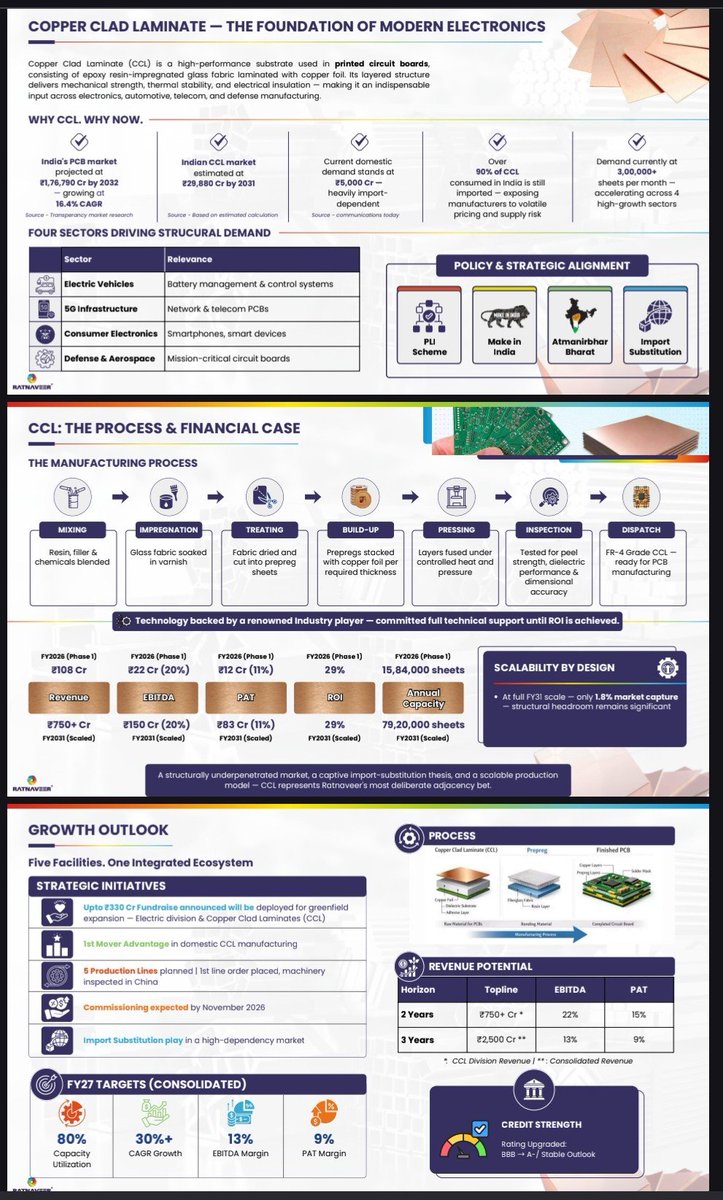

3️⃣ Ratanveer precision engineering limited🔖 Ratnaveer Precision Engineering Ltd manufactures and sells a diverse range of SS products Volume spurt seen on the chart #Ratanveer

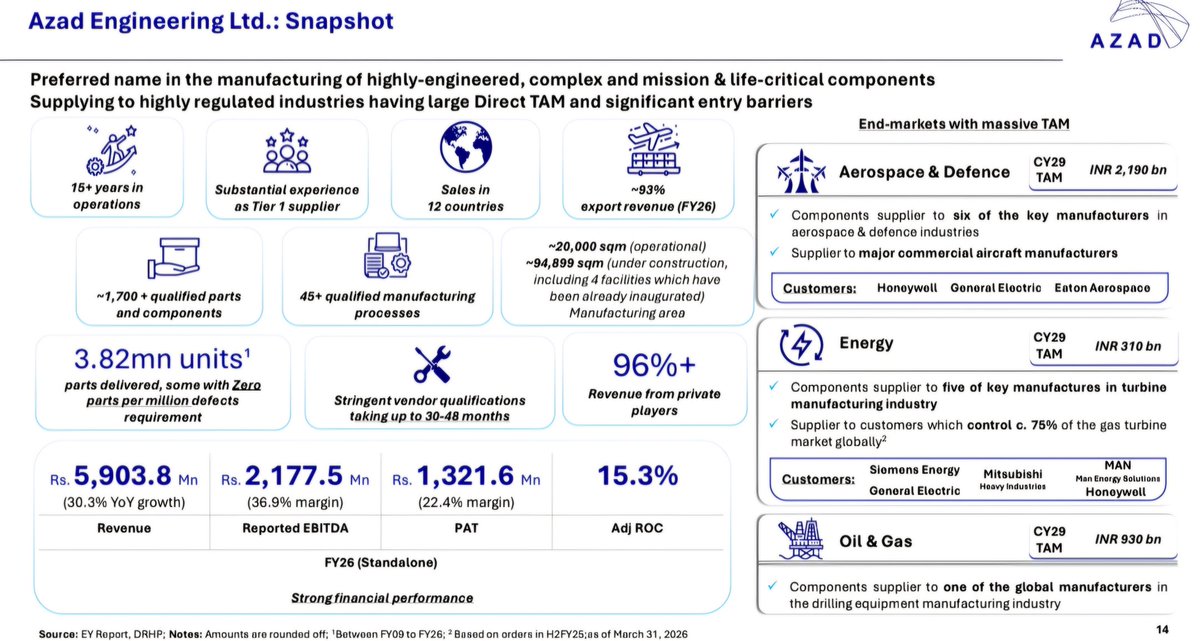

AZAD Engineering - Supplier of highly engineered, mission and life-critical components 🔥 🔶️ Scale & Positioning • 15+ years of operations • Sales across 12 countries • 45+ qualified manufacturing processes • ~93% export revenue in FY26 • 96%+ revenue from private players • Delivered 3.82 million units till FY26, including components with zero parts-per-million defect requirements 🔶️ Industry Presence • Supplier to six key manufacturers in Aerospace & Defence • Supplier to five key manufacturers in turbine manufacturing industry • Customers control ~75% of global gas turbine market • Operates in industries with vendor qualification cycles of 30-48 months, creating high entry barriers 👌👌 🔶️ FY26 Business Mix • Energy & Oil & Gas contributed 81.5% of revenue • Aerospace & Defence contributed 17.2% 🔶️ Management Guidance & Strategic Outlook • Reiterated 25%+ revenue growth guidance for FY27 and over the long term 🚀 • Management expects EBITDA margins to sustain at 33-35%+ supported by continuous operational and flow improvements • Over the next 4-5 years, Energy segment contribution expected at 55-60% of revenues 🔶️ Major Facility Expansion • AZAD inaugurated four dedicated facilities at Tunikibollaram Industrial Park, Hyderabad: >> Mitsubishi Heavy Industries – 7,200 sq.m >> GE Vernova – 7,600 sq.m >> Siemens Energy – 7,200 sq.m >> Baker Hughes – 7,600 sq.m • Manufacturing footprint: >> ~20,000 sq.m operational >> ~94,899 sq.m under construction >> Additional Phase-2 expansion of 67,267 sq.m planned 🔶️ Key Orders & Strategic Agreements • GE Vernova agreement worth USD 112 Mn for advanced gas turbine components • Additional GE Vernova agreement worth USD 53.5 Mn for nuclear, industrial and thermal power industries • Mitsubishi Heavy Industries LTCPA valued at USD 83 Mn for 5 years • Siemens Energy agreement valued at USD 90 Mn • Arabelle Solutions agreement valued at USD 40 Mn • Honeywell Aerospace Phase-1 award valued at USD 16 Mn • Strategic supply agreement extension with Baker Hughes till CY2030 🔶️ Order Book & Revenue Visibility • Total Order Book: Stands at a rolling ~₹6,500 crores, providing 11-12x forward revenue visibility 👌 • Execution Timeline: The ₹6,500 crore order book is slated to be consumed over the next 5 to 6 years 🔶️ Growth Drivers & Strategy • Increasing wallet share from existing OEMs 👌 • Expanding into higher-value products including advanced gas, steam and nuclear turbines • Focus on automation, lean manufacturing and operating efficiencies • Strategic expansion into Saudi Arabia • Building end-to-end manufacturing and integration capabilities • Expansion into landing gears and advanced turbine components 👉 Follow @vishan_29 for more updates. 🔴 Disclaimer: No recommendation. For educational purposes only.

KRN Heat Exchanger Q4FY26 Concall Updates - Bullish 🔥 🗣 "Next 8 quarters will be the strongest growth phase for the company" • New facility >> 6x capacity of existing with 1800-2400 Cr revenue potential >> Utilization in FY27 - 50% and 80% by FY28 • Expanding across Bus AC, DC, Railway, HVAC etc • Datacenter Cooling remains to be a strong area for the company • 95% revenue still from fin n tubes • Talks with Vertiv progressing for Datacenters, Schneider Electric already one of largest customers in DC • Bus AC >> FY27 Revenue- 150-160 Cr >> Market share - 15% • FY27 exports - 2x of FY26 or 200 Cr in North America, Europe etc. • Long term export contribution to be 50% of revenues • All raw material costs are passed onto customers • No competition with Chinese counterparts as KRN is highly customized and application specific 🔴 Disclaimer: No recommendation. For educational purposes only.

MTAR Technologies Ltd Q4FY26 Results:- #Q4Results #Q4FY26 #Stockmarket #Nifty #MTAR Total 306.07 Cr vs 183.09 Cr (+67.17% YoY┃+10.11% QoQ) EBITDA 61.81 Cr vs 34.15 Cr (+81.01% YoY ┃-3.46% QoQ) EBITDA Margin 20.19% vs 18.65% YoY & 23.03% QoQ PBT Ex-Exceptional Items 59.54 Cr vs 18.62 Cr (+219.77% YoY┃+19.36% QoQ) PAT 44.28 Cr vs 13.72 Cr (+222.72% YoY┃+27.66% QoQ) Other Income 16.40 Cr vs 0.03 Cr YoY & 2.41 Cr QoQ Last Q3 Exceptional loss of 3.76 Cr