A look at the AgBiTech Acquisition by @BASF.

In Q1 2026 BASF announced the acquisition of AgBiTech.

One thing to note from their report is the “Investments” line. The AgBiTech acquisition was finalized in Q1 and investments were up ~€120 million YoY, and about the same above the 5-year average for the same period.

In looking at the cashflow commentary there is a call out of the acquisition:

Payments were made in the amount of €124 million in connection with the acquisition of AgBiTech, Brisbane, Australia, and for a purchase price adjustment of €33 million relating to the sale of the global pigments business in 2021.

The statement is confusing to me given the second half of the sentence. However, given the investment and acquisition line item suggesting a ~ €120 million price for AgBiTech, and the line seemingly suggests €124 million in deal price, it seems safe to assume €124 million is the price that was paid.

I speculated on the price paid, and I was way off. But since we roughly know their revenue, and now the value, we can look at revenue multiple paid, which gives a base barometer for other future acquisitions:

AgBiTech seemingly had ~$20 million USD in revenue. Using a USD to EURO of 0.85 we get a revenue of ~€17 million, which means a revenue multiple of 7.3x. Higher than I expected. For context, Corteva acquired Stoller (not biocontrol) for ~3x revenue, Syngenta acquired Valagro for around the same and BASF’s previous large acquisition, Becker Underwood, was for around 4x.

@ShaneAgronomy@UpstreamAg “The most successful incumbents in agriculture are not trying to act like software companies. They are leveraging slow-clockspeed realities to their advantage.” 🔥🔥🔥

Clockspeed, Capital, and Conviction: Considerations for R&D and M&A in Agribusiness

There is a recurring critique that incumbent agribusinesses are "asleep at the wheel" because they do not spend higher percentages of revenue on R&D like big tech or pharma, or don't acquire like other industries. The framing, while well-intentioned, doesn't consider the structural dynamics of large companies and the greater industry incentives.

I believe there are frameworks that can help us understand why we don't see more.

One of those is industry "clockspeed" — a concept coined by Charles Fine in his book by the same name.

Industries have different rates of evolutionary change. Software and semiconductors sit at the fast end, where hesitation is fatal. Agriculture, however, is a slow-clockspeed industry.

In fast-clockspeed industries, the cost of being wrong is high, but the cost of inaction is higher. In agriculture, premature commitment can be destructive.

This is why simply asking for more M&A or R&D is a tactical oversimplification. The most successful incumbents in agriculture are not trying to act like software companies. They are leveraging slow-clockspeed realities to their advantage. They observe market traction, identify "consensus bets" and then leverage their distribution moats to scale these technologies in ways startups cannot.

Capital allocation is not just about spending; it is about disciplined orchestration across all potential uses of capital.

The CEOs who deliver long-term returns are those who resist the pressure to chase growth for its own sake and instead deploy capital based on competitive positioning and internal cash flow. These also tend to be the companies that deliver the better products and outcomes to customers long term, too.

In my latest breakdown, I look at the intersection of clockspeed, capital allocation, and why the disruption narrative often misses the mark in agriculture.

Check out a brief overview of Clockspeed in the video below. @UpstreamAg

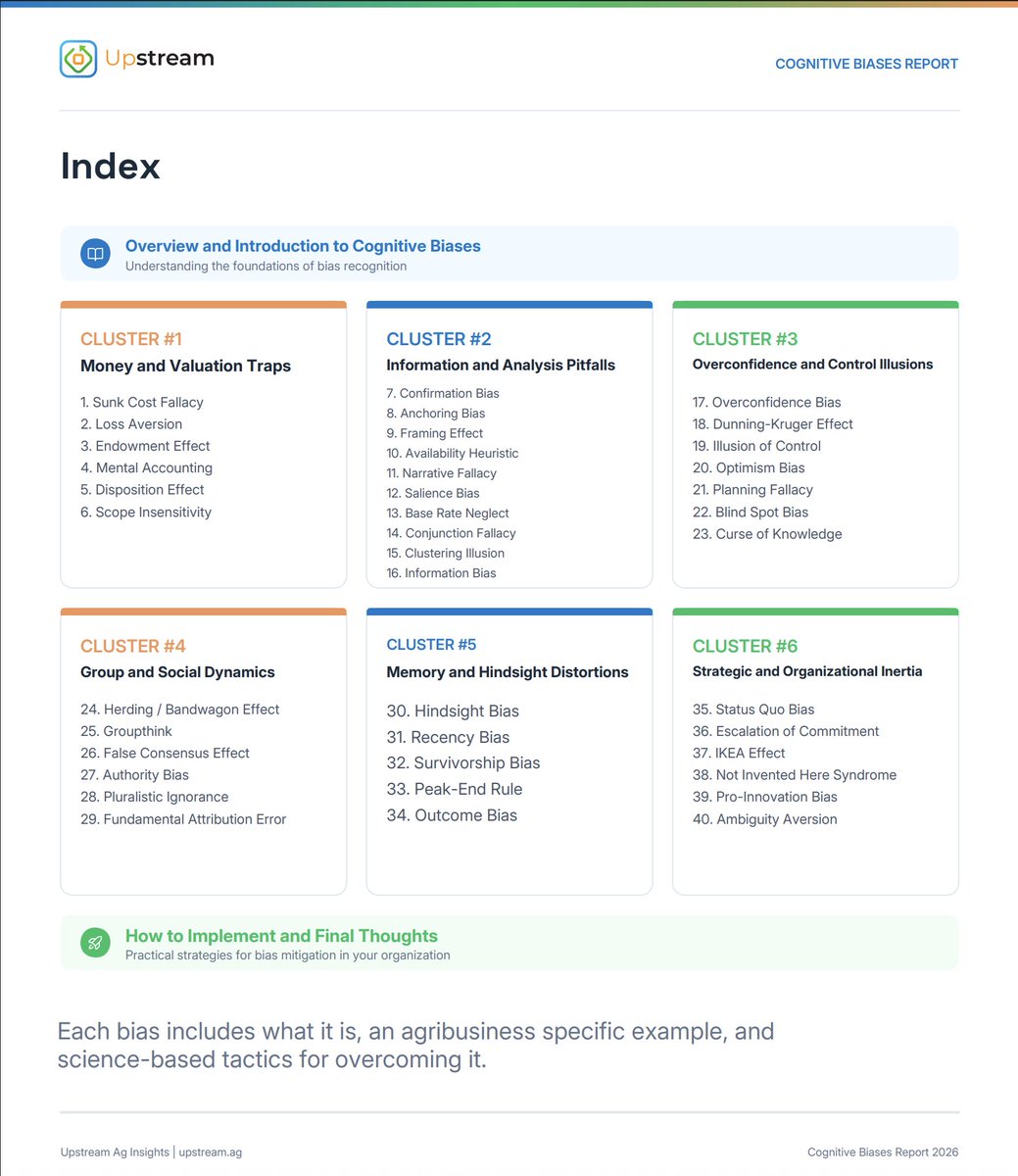

Cognitive Biases and Improved Decision Making for Agribusiness Leaders

◼︎◼︎◼︎

A cognitive bias is a systematic pattern of deviation from rational judgment. It's a predictable way our brains diverge from effective reasoning when processing information, evaluating risk, or making decisions.

I believe understanding them can vastly improve decisions making, along with influence.

So I put together a breakdown of 40 biases I find relevant, across 6 related clusters.

Every one is framed around actual agribusiness situations, including capital allocation, M&A, trading desks, R&D pipelines, selling, product launches, marketing, or board dynamics.

A few examples from inside:

- The ag retailer who sunk $4M into a proprietary digital platform because walking away felt like "wasting" the spend. The $7M budget was gone either way. The real cost was 18 months of delayed partnership revenue.

- The seed company that kept funding a declining $80M legacy platform because visible revenue felt more real than a next-gen pipeline. Clayton Christensen's disruption theory in action.

- The boardroom spending 90 minutes on an $80K break room and 30 minutes on a $12M acquisition.

Each bias includes what it is, the agribusiness example, and science-based tactics for overcoming it.

I also recorded a podcast on 7 of the biases, with an overview of one of my favorites, The IKEA Effect.

Researchers showed people value what they build themselves far more than identical items built by others — even when the self-built version is objectively inferior.

In agribusiness, this is the custom-built CRM defended against a superior commercial alternative, or even less tangible things like strategies or initiatives. I think it is worth paying attention to.

@UpstreamAg

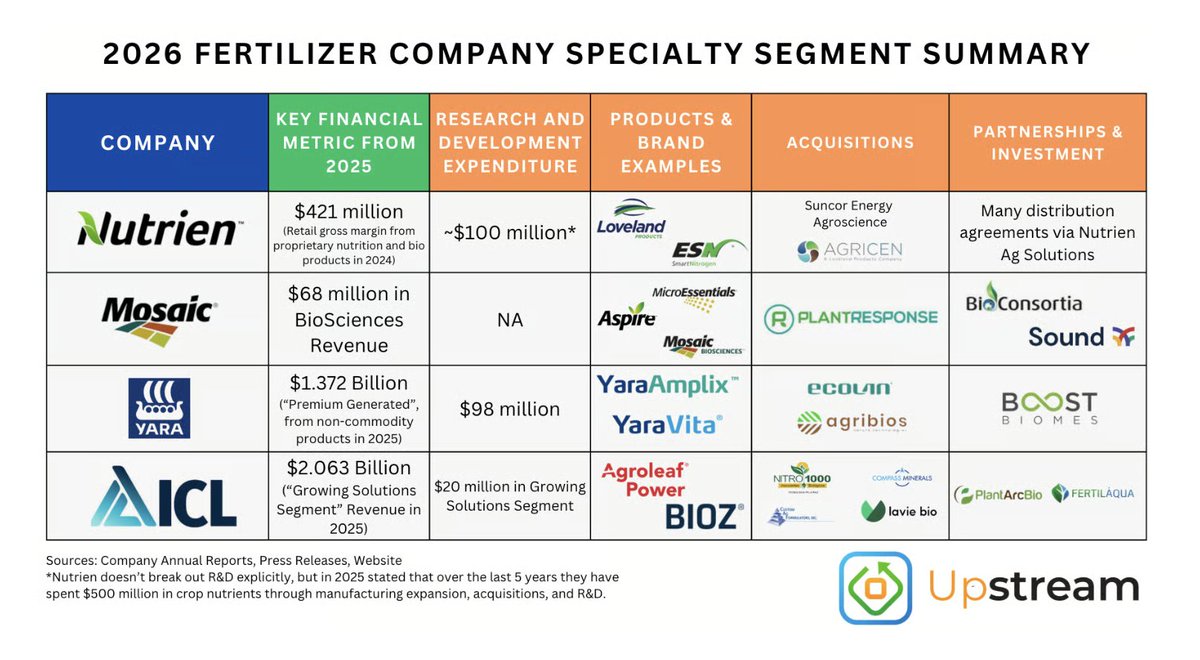

Every major crop input company now has a biologicals strategy. The question is how are they progressing and what specifically are they doing?

I just published an updated report that tracks the biologicals and specialty nutrition strategies, revenues, acquisitions, partnerships, pipelines, and commercial progress of 16 companies across crop protection, fertilizer, and the independent biologicals landscape.

Crop protection: Corteva, BASF, Bayer, Syngenta, FMC, and UPL.

Fertilizer: Yara, Mosaic, Nutrien, and ICL.

New to this edition are profiles on six scaled independent players that rarely get this level of coverage: Rovensa Next, BioFirst Group (formerly Biobest), Verdesian Life Sciences, Koppert, Acadian Plant Health, and DE SANGOSSE.

A few things you'll find inside:

Mosaic's Biosciences business doubled revenue to $68 million in 2025, hit EBITDA positive in 2025, and is targeting $200 million in EBITDA by 2030. How they're applying the MicroEssentials playbook to biologicals, and where their nitrogen fixation go-to-market approach may get challenged.

Corteva posted $519 million in biological revenue in 2025. What the planned Corteva split means for the biologicals portfolio, and why the NEXTA launch through Pioneer dealers is an important initiative.

BASF acquired AgBiTech in early 2026, their first meaningful bio acquisition since Becker Underwood in 2012. The report looks at why NPV-based bioinsecticides are a fit, and what the coming Ag Solutions IPO means for their biologicals investment appetite.

Nutrien's proprietary crop nutrition and biostimulant gross margins are approaching $500 million, with 70% of future proprietary product growth expected from biologicals and nutritionals.

The report also includes side-by-side comparison snapshots across segments, the largest bio-based and specialty acquisitions to date, an acquisition timeline since 2010, the key market drivers behind the growth of this segment and images illustrating acquisitions and partnerships, along with future considerations for the companies.

@UpstreamAg

DunhamTrimmer Biostimulant Report Highlights and Analysis

◼︎◼︎◼︎

The global biostimulant market hit $4.47B in 2024 and is projected to reach $7.88B by 2030.

But the headline number obscures what's actually happening structurally in the category.

Latin America and Asia-Pacific have overtaken Europe as the largest biostimulant-using regions. North America crossed $1B for the first time. Humic and fulvic acids dominate North American sales, driven by access to high-quality leonardite deposits, but amino acids and protein hydrolysates are gaining ground fast.

Meanwhile, commoditization is accelerating. Low barriers to entry, shared raw material suppliers, weak IP, and undifferentiated go-to-market strategies have put much of the industry on a path toward price-based competition. The companies that built this category now face the most pressure from it.

The most important forward-looking concept in the DunhamTrimmer report is Single Biostimulant Molecules. Rather than working with complex blends and differentiating purely through marketing, SBM players are identifying specific molecules with defined modes of action on plant metabolism and rhizosphere pathways. More specificity means more consistent efficacy, more replicable results, and a defensible value proposition, similar to how crop protection efforts have been executed.

I recorded a full video walkthrough of the DunhamTrimmer 2025 Global Biostimulant Report covering:

- Drivers of Interest

- Regional growth dynamics and where the market is headed

- Commoditization pressures and strategic responses

- The Single Biostimulant Molecule opportunity

- What this means for companies and investors in the space

Check out the full video below. @UpstreamAg

Cognitive Biases and Improved Decision Making

■■■

Every strategic decision in agribusiness passes through a human brain before it becomes action. That brain, regardless of the education or the decades of experience informing it, is running on cognitive software that evolved to avoid predators, and prioritize short term constraints, like food management or safety, not to optimize for being different, thinking long term or building systems that create success in business.

These sub-optimal approaches to thinking and decision making are known as cognitive biases.

They are patterns deviating from rational judgment and are not occasional mistakes or signs of low intelligence, however, they are predictable, measurable, and universal tendencies that affect how we process information, evaluate risk, remember outcomes, and interact with others.

They have long been central to my considerations when decision-making — though I remain far from perfect at managing them.

I think anyone operating in agriculture should be even aware of these biases – for those farming, and allocating capital and resources, or at a company and managing a team, or setting strategic priorities.

The higher the stakes and complexity of a role, the more cognitive biases can distort our judgment in ways that are hard to detect in the moment.

The full breakdown examines 40 cognitive biases through the lens of decision-making, for the likes of boardrooms, R&D labs, commercial teams, and executive suites where strategic decisions can influence billion dollar outcomes.

For each bias, there are four main areas covered:

1. what it is

2. why it matters

3. a specific agribusiness example of how it distorts decisions (occasionally, I will highlight how they can be used inversely, as well).

4. science-based strategies for overcoming it.

The full report is available for subscribers at upstream. ag.

@UpstreamAg

Upstream Ag Professional - The Big Three Stories of the Week

◼︎◼︎◼︎

A look at what agribusiness leaders will find in this weekend's edition of Upstream Ag Professional:

1. Cognitive Biases and Improved Decision Making for Agribusiness Professionals

Often we focus on making smarter decisions, but as good of an opportunity to improve our decison making and effectiveness is to remove predictably bad ones.

Over a decade of collecting cognitive biases led me to build a practical guide with 40 biases I reference often, organized into six clusters, each with agribusiness-specific examples and science-based strategies for overcoming them.

The aim is to have a reference piece for agribusiness professionals to imrpove their decision making, or enhance their influence.

2. Biostimulant Sales: Like selling seed? Or something else?

Check out a small clip from this week's @UpstreamAg Professional audio coverage highlighting the similarities to crop protection, but it goes further than that and I dive in in this weekend's edition.

3. Mental Models for Agribusiness Leaders with Shane Thomas on The Future of Agriculture

This week I joined @timhammerich on The Future of Agriculture podcast to discuss 7 useful mental models that are directly applicable to agribusiness professionals. Models include some popular, and some lesser known ones: Jevons Paradox, Influence Erosion, Strategy Tax, Friction Reduction, Contrarian Decisions, Jobs to be Done and One-Way Doors vs Two-Way Doors

Plus much more in this weekend's edition.

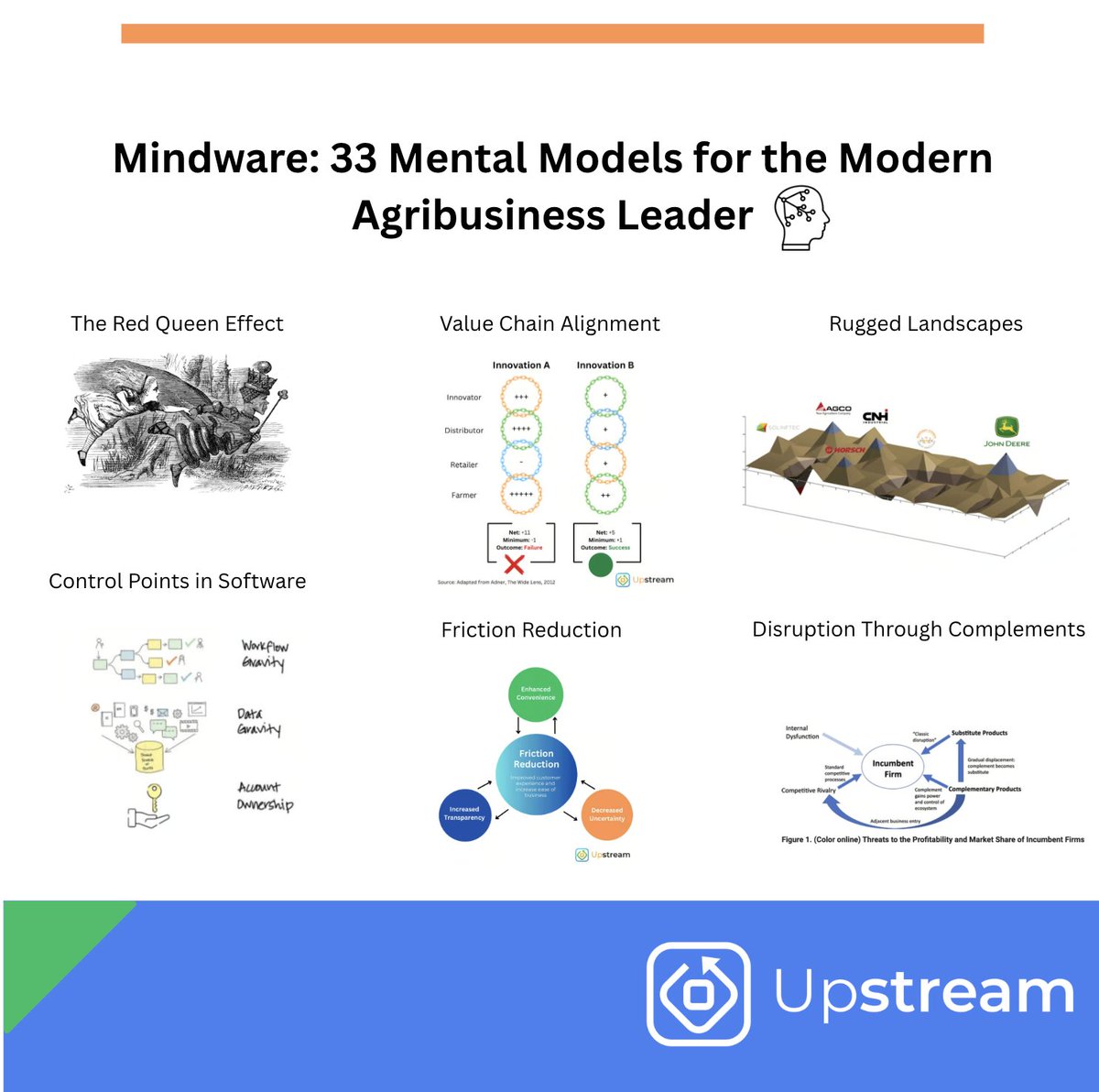

Mental Models for Agribusiness Leaders

◼︎◼︎◼︎

Recently, I talked with @timhammerich on The Future of Agriculture, one of my most listened to podcasts.

It was a ton of fun to join Tim and talk about some of the concepts that have been valuable to me over the course of my career.

In the conversation, we dive into half a dozen of the mental models I covered in the @UpstreamAg Insights e-book, Mindware: 33 Mental Models for The Modern Agribusiness Leader.

The basis of the concepts are that agribusiness professionals operate in a world full of volatility, complexity, and constant change. Commodity price swings, regulatory shifts, changing customer demands, and technological evolution create a landscape where uncertainty is the norm.

And ultimately, agribusiness professionals are knowledge workers and what separates the best in agribusiness from the rest is often how they think.

Thinking better, whether more strategically or quickly, requires mental tools.

Carpenters have a tool belt, golfers carry 14 clubs, a chef has more than just a spatula.

Every "tool" serves a specific purpose, depending on what is required.

Agribusiness professionals should operate the same way with mental tools.

These mental tools are what I refer to as Mindware - models and frameworks that help to gauge a scenario, find gaps in logic, or think long term, ultimately delivering improved judgement and better outcomes for careers and businesses.

Check out the full conversation where Tim and I discuss the concepts and apply them directly to agribusiness: futureofagriculture.com/episode/mental…

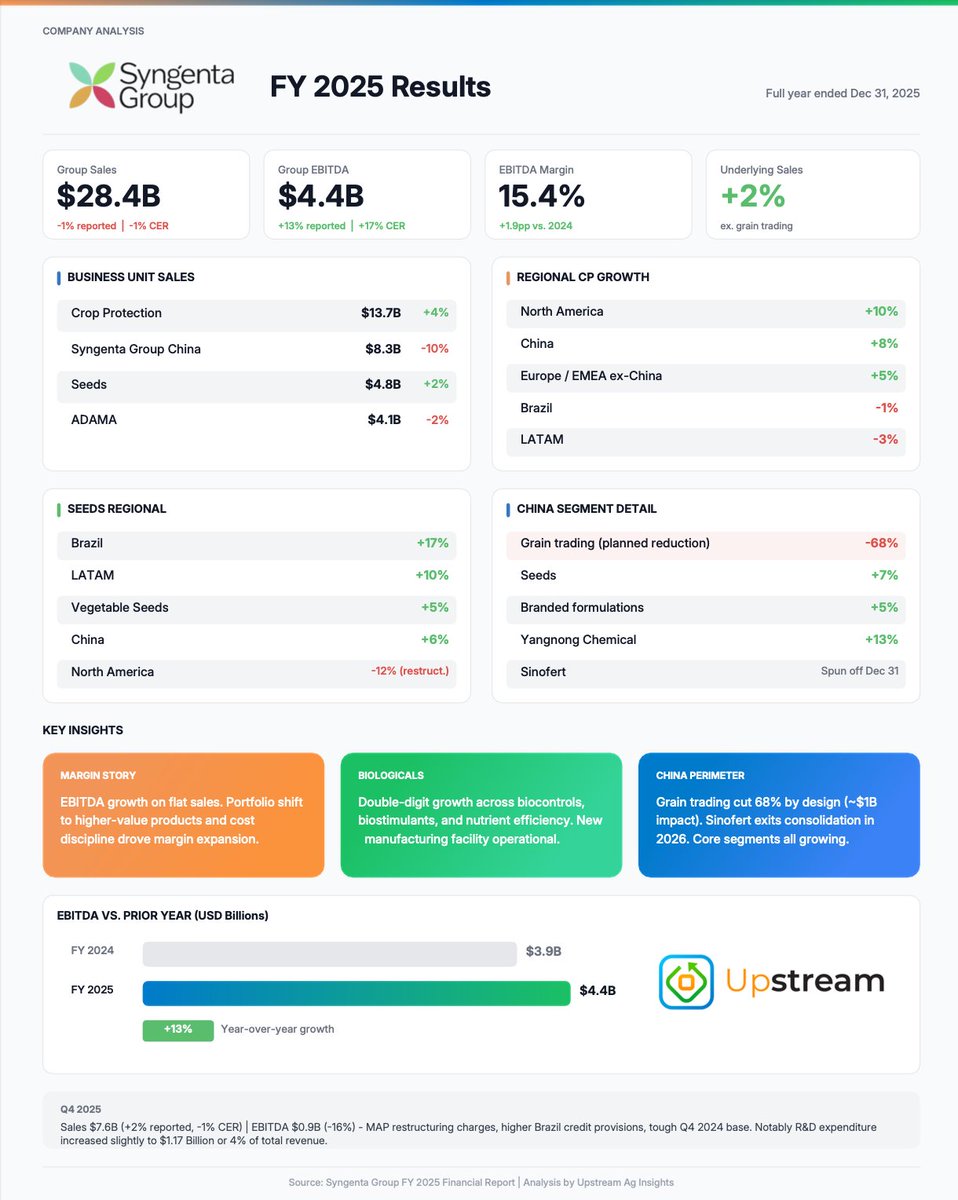

FY 2025 crop protection and seed results have all been reported, across @Bayer, @BASF, @corteva, FMC, @Syngenta, @UPLLtd, and @NufarmSeedsNA.

Several players were down, however, the crop protection market was viewed as more stable (before recent geopolitical events, anyways).

Channel inventories are normalized globally for the first time in a while, and for the first time in several years, the consensus view heading into 2026 is modest growth.

Volume is recovering, but generic competition has led to price challenges which have been more concentrated in Latin America and Asia Pacific, but seem likely to be a bigger concerns in North America in coming years.

A few other takeaways:

The major companies continue to emphasize biological capabilities on their earnings calls. Corteva hit $519M with 16% volume growth, but pricing hcallenged, particularly in LatAm, where 80+% of their bio rveneue occurs.

Syngenta delivered double-digit biologicals growth.

BASF acquired AgBiTech ahead of its planned IPO. FMC did not emphasize like they have historically, but shows how even though it is viewed as a growth priority, the core of their business is still chemistry and when challenges to the greater business arise, the focus remains on saving the core.

AI in discovery is continuing to be talked about, and I wil cover it more next week, but in the interim, Corteva described 1,000x faster active ingredient identification from molecular libraries. Regulatory submission preparation is also being compressed.

All companies flagged tighter farmer margins influencing purchasing behavior, even as underlying application demand stays consistent with historical levels.

For the full breakdown, check out the link below, or get quick hits for some companies in the @UpstreamAg images attached.

I recently spent time in Austin at the @AgVendHQ Partner Summit with over 250 industry leaders.

There was the usual talk of margin pressure and farmer profitability challenges, but what was most compelling to me was the sharing of the product roadmap.

I think the roadmap for a software company that penetrates 35% of the North American retail market provides an interesting signal into the future of ag retail:

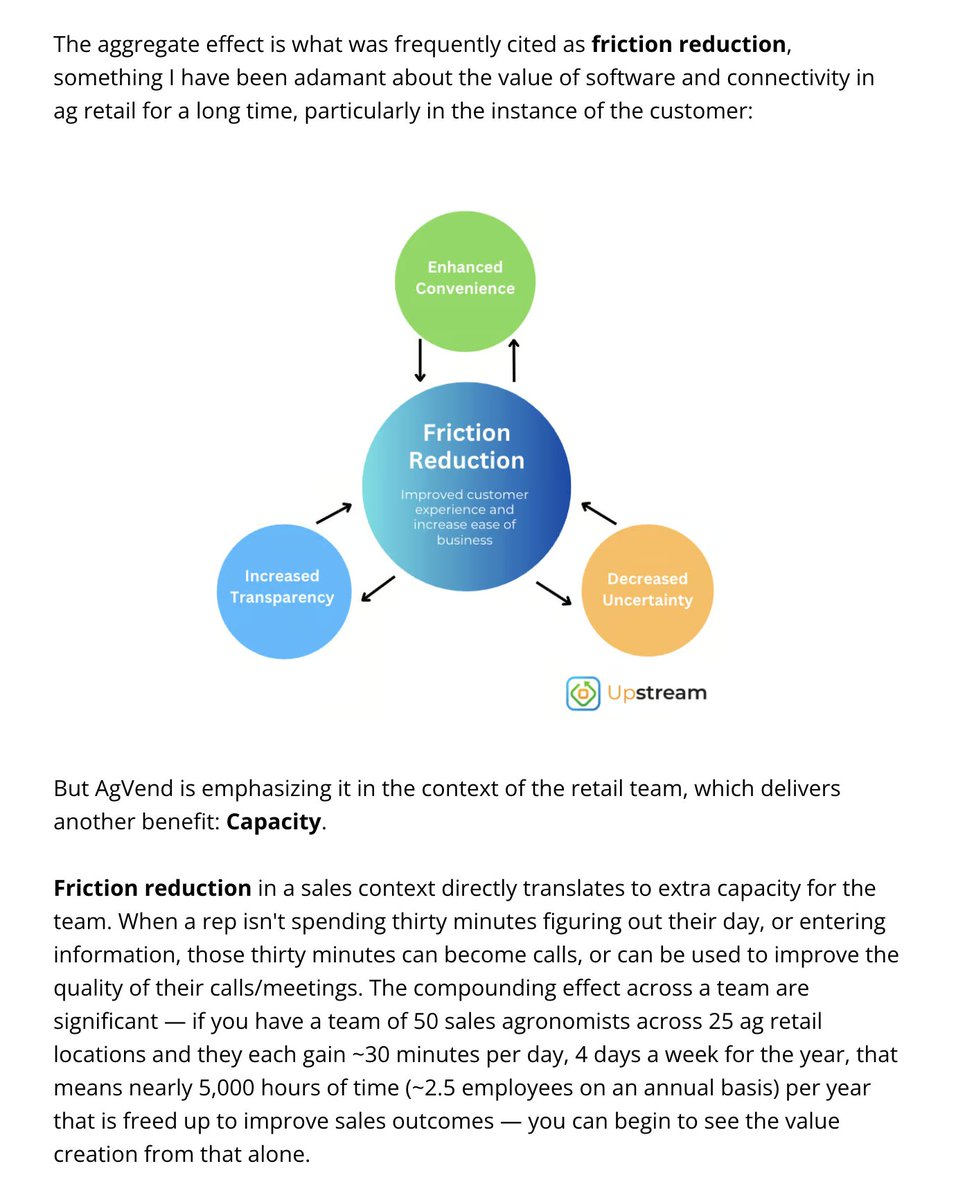

What problems it believes are worth solving, where it's placing its bets, and if you read between the lines what it thinks the next chapter of ag retail looks like, including heavy emphasis on one of my favorite subjects, friction reduction, and team efficiency that leads to better outcomes for retails, crop input manufacturers and ultimately better results and experiences for farmers, too.

A few product components that caught my eye:

1. CRM+ and the Death of "Dead Time"

CRM initiatives in ag retail usually fail because data entry is tedious and the "next step" after entering data is never clear. AgVend is attacking this with a Voice AI Agent. Now, sales reps can now have a conversation with an AI agent while driving. The AI structures the notes, logs them, and creates tasks based on the conversation with the farmer, that is relayed to the agent.

2. Loyalty & Programming

Historically, retailer-led loyalty programs have been an Excel nightmare. By leveraging real-time transactional data, retailers can now embed incentives directly into the purchase flow and give customers an up to date understand of where they stand and how they can unlock further rewards. Interestingly, pilot results showed 25% higher agronomy spend among participants.

3. The Power of the "Control Point"

This is one of my favorite strategic concepts and I came across it a few years ago when I was trying to better understand what software strategy in agribusiness should look like. By owning the "Control Point"—the mission-critical software driving daily workflow—AgVend earns the right to integrate complex layers like Program Management (tracking those notoriously opaque manufacturer rebates) along with other capabilities, like their Nexus product suite, to be able to touch all points of the value chain.

When these products get utilized in ag retail, AgVend becomes what I would call Digital Infrastructure, for not only the retailers and cooperatives, but the value chain.

By solving for inefficiencies, such as misaligned forecasting, lagging incentive data, and slow reconciliation they can become an irreplaceable node between the manufacturer, the retailer, and the farm gate.

I’ve shared a full analysis of the roadmap, in the @UpstreamAg article.