Sabitlenmiş Tweet

New post:

VIX ETPs – What Can Go Wrong?

vixandmore.blogspot.com/2022/04/vix-et…

$VXX $UVXY $VIXY $SVXY $UVIX $SVIX

English

Bill Luby

9.2K posts

@VIXandMore

Volatility, VIX products, options, ETPs and random musings about wine, music, travel, AI, etc. Bot slayer. Never investment advice. https://t.co/dO8lFhLFTa

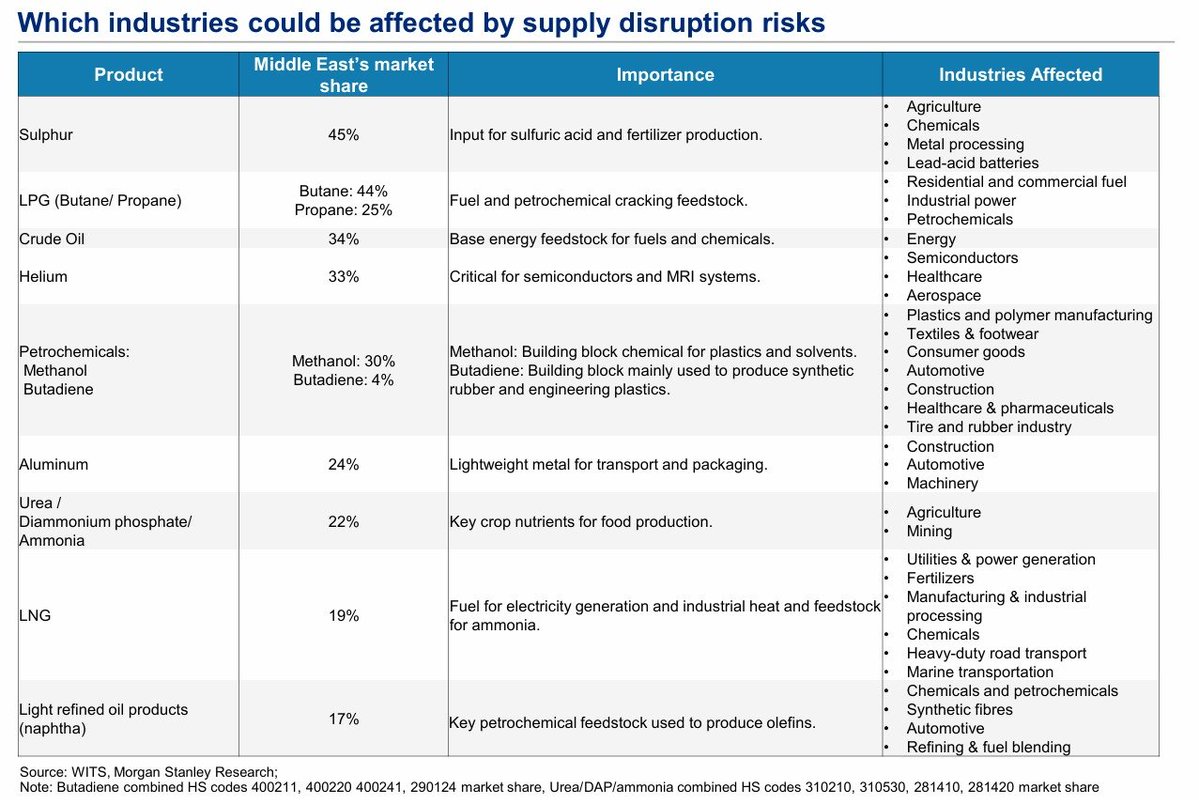

Seven clocks are running. None of them negotiable. All of them counting down to the same weeks. The planting clock. Mid-April is the biological deadline for corn and soybean planting across the US Midwest. Every day that passes without nitrogen becoming affordable and available narrows the window for corn. USDA projects corn falling to 94 million acres from 98.8 million. Soybeans rising to 85 million from 81.2 million. The seeds that go into the ground in the next three weeks determine America’s grain harvest in October. The decision is irreversible. The USDA clock. March 31. Prospective Plantings. The report that converts farmer intentions into official data. Every acreage number, every corn-soy ratio, every nitrogen-dependent calculation becomes a published fact that traders, governments, and food agencies will use to model global supply for the next twelve months. The number arrives in twelve days. The FAO clock. April 3. The Food Price Index. The first global reading that captures post-Hormuz commodity prices across cereals, vegetable oils, dairy, meat, and sugar. The 2022 peak was 159.7 in March 2022 after Ukraine. This reading will incorporate oil above $100, urea at $610, LNG halted, packaging repriced, and freight surcharges of $500 to $1,500 per container. The number that determines whether the UN declares a food emergency arrives in fifteen days. The pharmaceutical clock. India’s API inventory buffers are two to three months, measured from the war’s onset on February 28. Late May is the depletion window. Methanol at 87.7 percent Hormuz exposure feeds the solvent chain for paracetamol, ibuprofen, metformin, and antibiotics. Once buffers deplete, the shortage becomes a patient access crisis for the 47 percent of US generics that originate in India. The China crude clock. FGE NexantECA confirmed China is drawing commercial reserves at up to one million barrels per day. The draw sustains refinery operations for four to six weeks from March 19. Mid-April to late April is the exhaustion window. After that, China faces three options: accelerate Russian pipeline imports, reroute at massive premium, or crack open the strategic petroleum reserve. The third option reprices every commodity on the planet. The helium clock. SK Hynix and Samsung hold two to three months of helium inventory. Late May to early June is the depletion window. South Korea imports 64.7 percent of its helium from Qatar. Ras Laffan is offline. If helium buffers deplete before alternative supply arrives, semiconductor fabrication faces rationing. The AI hardware supply chain hits a physical wall measured in months, not quarters. The insurance clock. Solvency II requires 30 to 60 days of zero incidents before P&I clubs can reinstate war risk coverage. Even after a ceasefire, the insurance normalisation takes six to sixteen months based on the Red Sea precedent of 26 months and counting. The logistics system lags the financial relief rally by the longest duration of any clock in this crisis. Seven clocks. The shortest expires in twelve days. The longest runs for over a year. The planting window, the USDA report, the FAO index, the drug buffers, the Chinese crude draw, the helium inventory, and the insurance cycle are all counting down simultaneously. None of them pause for diplomacy. None of them respond to presidential directives. None of them read sealed packets. The calendar is the only actor in this war that has never lost a negotiation. open.substack.com/pub/shanakaans…