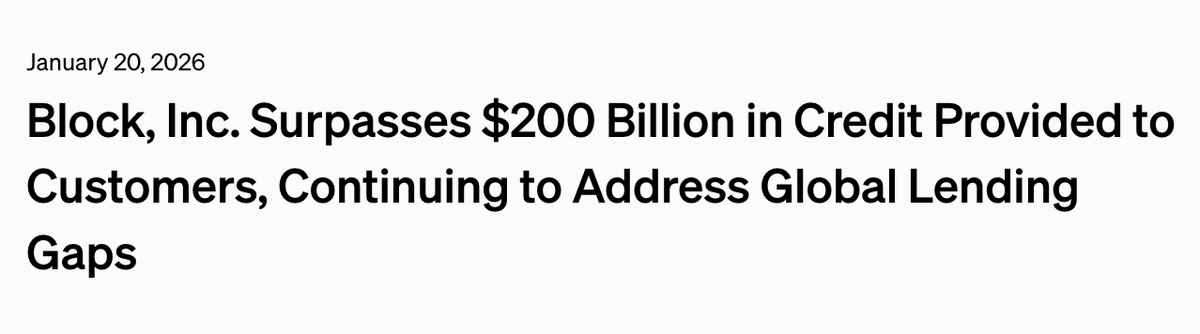

X is re-defining the future of money, while the Head of Product Design at Cash App is posting about coding and PR counts.

The gap in vision is starting to look wide. Feeling a bit bearish on $XYZ here

x.com/Teslaconomics/…

cam worboys@camworboys

In Aug 2025 we had 36 PRs from design. Last week we crossed 1,000 in production. Avg. PRs per week went from 21 in Dec to 54 in Jan to 124 in Feb. It’s wild. And it’s not just design → eng. PMs writing copy, data scientists shipping features. I’m more DRI than designer most days. The people thriving right now are malleable. Less attached to titles. Just want to build.

English