Today's peek into the ivory tower:

"luxury goods rely more heavily on services and have a lower environmental footprint"

lse.ac.uk/economics/Asse…

Really? I am ... skeptical.

We are looking for new colleagues!

Assistant Professor of Finance (Tenure-Track) at Frankfurt School of Finance & Management!

If you are creative, curious and passionate about research, apply by November 18 at apply.interfolio.com/158296

Let me know if you have any questions!

@frankoz95967943 Thanks! ..we provided only some suggestive evidence on the increasing volatility selling in recent periods.. certainly, it is only one of many forces driving volatility levels..

qmoms package for the Implied Moments from IV Surface!

Includes: log and simple variances, CVIX, TLM, Semi-vars, and tail measures.

On GitHub: github.com/vilkovgr/qmoms

..to be updated to include generalized lower bounds, implied betas, correlations++. Thanks for any feedback!

@ConcretumR@macro_synergy Good time of the day!

We also find that high 0DTE volume is associated with high volatility and underlying volume; in recent periods the flows in 0DTE and underlying markets are very correlated. However, we do not find that 0DTE flows cause higher volatility!

"The trading volume of zero days-to-expiration (0DTE) options has seen a significant increase in recent years... Increased trading in 0DTE options is associated with volatility and sudden price movements." papers.ssrn.com/sol3/papers.cf…

Tickets are now available for ØDTEs: Trading, Gamma Risk and Volatility Propagation at The Auditorium, Citigroup Centre, London on Thu 11 Apr 2024 at 6:00PM. Click the link for further information and to secure your tickets now! ticketsource.co.uk/whats-on/canar…

I just posted publicly about a bug in my code on GitHub. Gonna fix when I have the time. I wish other people did this. Does anyone else do this? github.com/chenandrewy/fl…

New analytical results on the impact of announcements and higher moments from 1DTE SPX option returns, building on 0DTE work by @VilkovGrigory and @BjornEraker with @NormanSeeger, Andreas Kaeck and Neel Shah. Macroeconomic announcements, not in 0DTE samples, drive 1DTE returns. papers.ssrn.com/sol3/papers.cf…

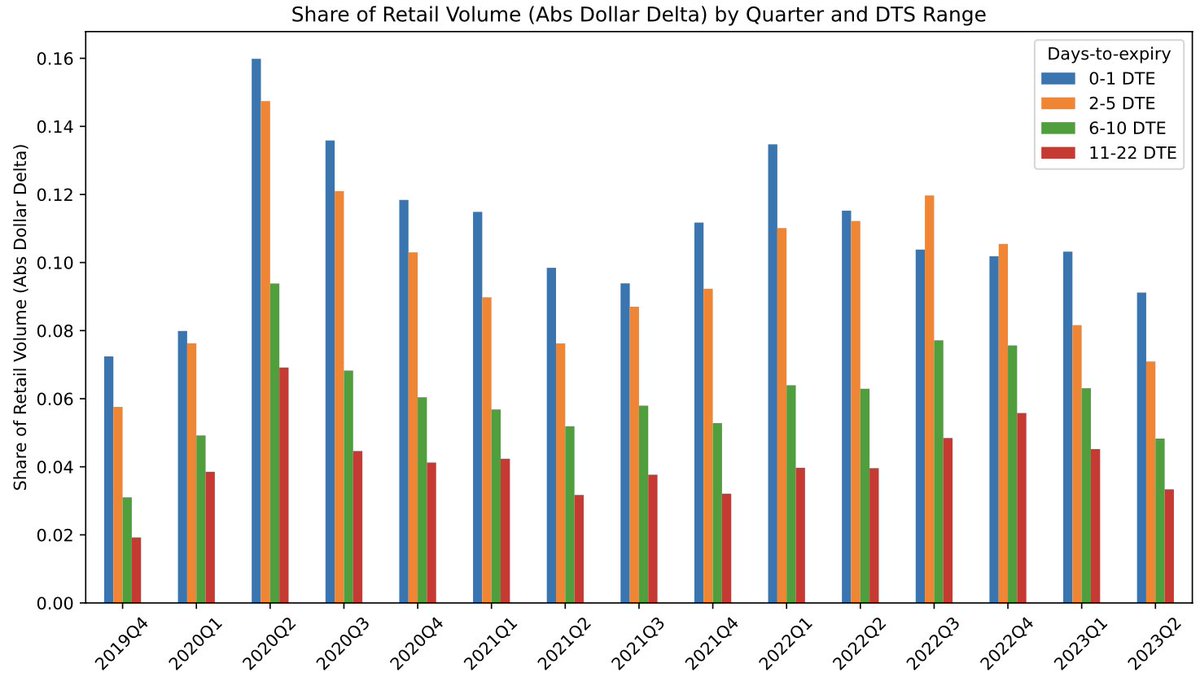

@paradoxinvestor Here is the share of the retail investors (identify by OPRA SLAN flag) for SPXW and SPY options by quarters and maturity buckets (in working days!)... rather going down than up! ..and it is pretty small overall!

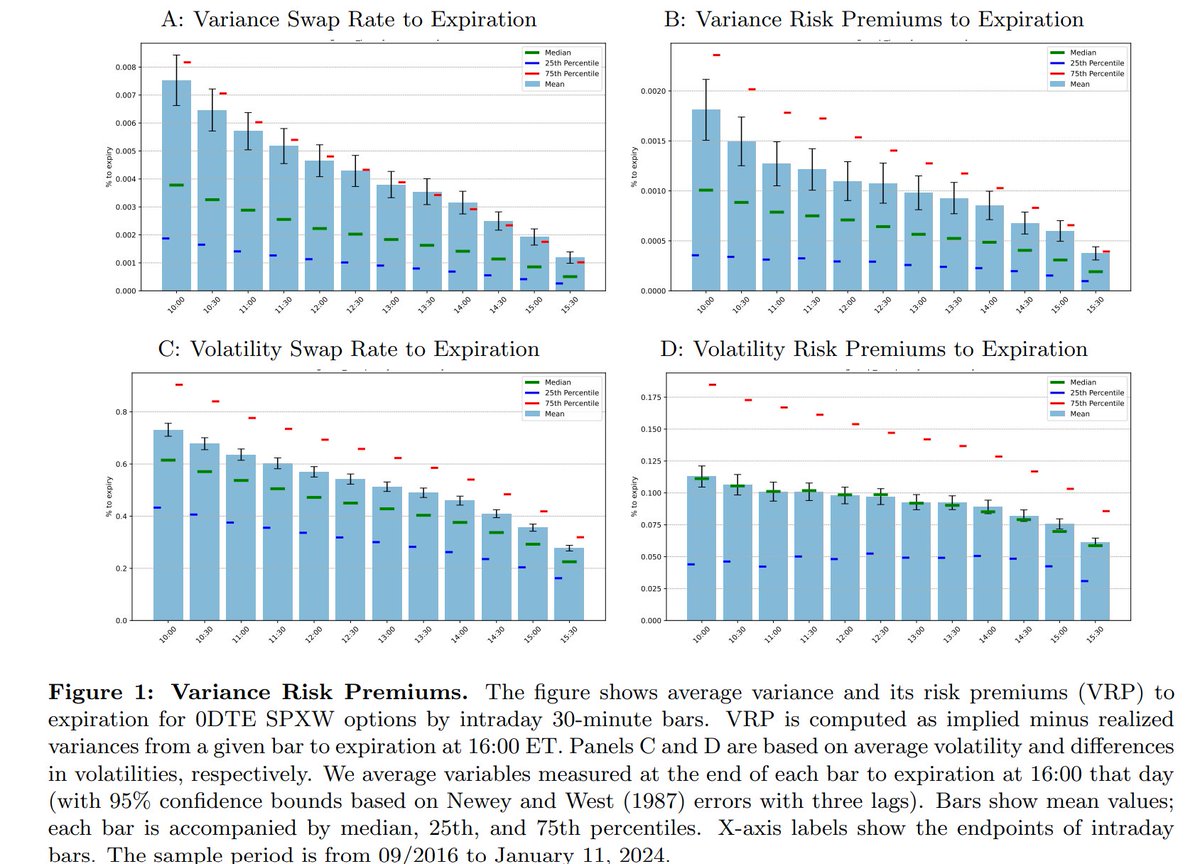

New options study. Zero-day options have become very popular recently. Buying them means losing money. Shorting them is hardly profitable: the variance risk premium is only 0.0011% (panel B). @VilkovGrigory up-to-date sample is from Sep2016- Jan2024. Link below shorturl.at/aruDQ

@prodigal_sun92@quantseeker selling calls is not profitable, and if some strikes show a positive median, the distribution is so wide that it is more a casino than trading.

@quantseeker@VilkovGrigory I'm gonna read into this more cause the idea that selling calls is profitable but risk reversals are too (which imply buying calls and adding more commissions) is contradictory unless the short put leg is carrying most of the PnL (which in that case just short the put).