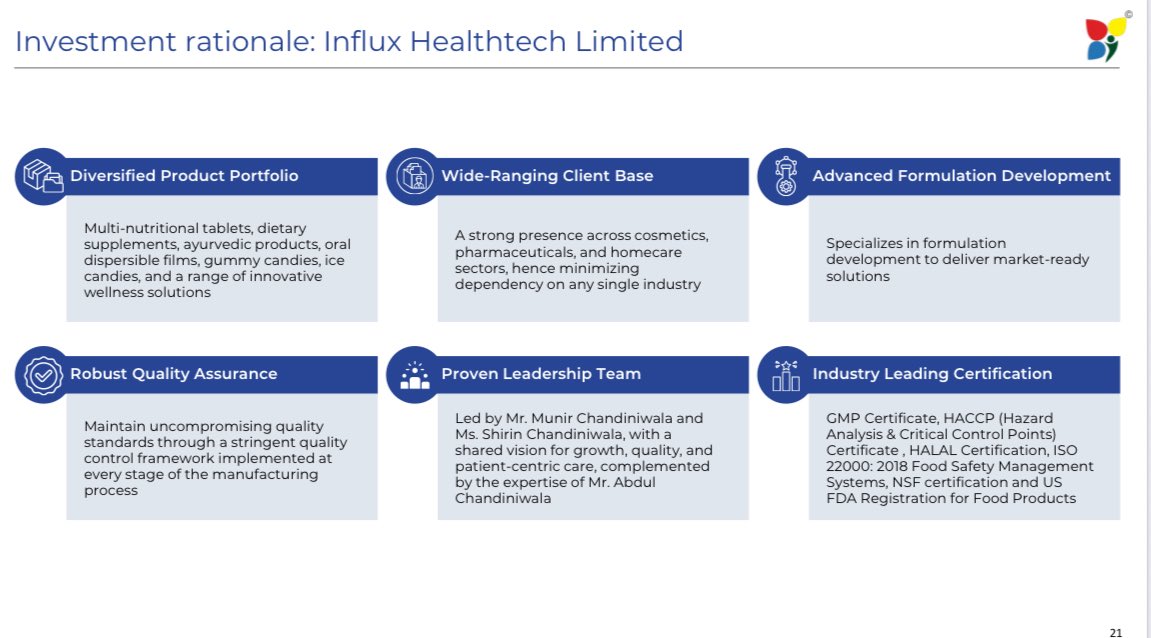

𝐈𝐧𝐟𝐥𝐮𝐱 𝐇𝐞𝐚𝐥𝐭𝐡𝐭𝐞𝐜𝐡 (Update) A 𝐑𝐚𝐫𝐞 𝐂𝐃𝐌𝐎 / 𝐍𝐮𝐭𝐫𝐚𝐜𝐞𝐮𝐭𝐢𝐜𝐚𝐥𝐬 𝐩𝐥𝐚𝐲𝐞𝐫 𝐥𝐢𝐬𝐭𝐞𝐝 𝐢𝐧 𝐒𝐌𝐄 𝐬𝐩𝐚𝐜𝐞 Main Board quality company on SME platform ✅Promoter quality + Manufacturing facility - Both are TOP Notch Detailed analysis👇🏻 ________________________________ Co is engaged in CDMO (end-to-end right from 𝐝𝐞𝐯𝐞𝐥𝐨𝐩𝐦𝐞𝐧𝐭 𝐨𝐟 𝐟𝐨𝐫𝐦𝐮𝐥𝐚) for Nutraceutical brands 🔹𝐒𝐞𝐫𝐯𝐢𝐧𝐠 𝐭𝐨𝐩 𝐧𝐮𝐭𝐫𝐢𝐭𝐢𝐨𝐧 𝐛𝐫𝐚𝐧𝐝𝐬 𝐢𝐧𝐜𝐥: 1. Carbamide Forte (products - superb ratings on Amazon) 2. Divine nutrition - one of a well known brand in supplement etc 3. In talks with ON nutrition (US based- considered one of the top of industry) 🔹𝐕𝐞𝐫𝐲 𝐬𝐭𝐫𝐨𝐧𝐠 𝐛𝐮𝐬𝐢𝐧𝐞𝐬𝐬 𝐦𝐨𝐝𝐞𝐥: - Net debt free - Historical consistent Operating Cash Flows (OCF) to EBITDA of 50-60% - Continuous capex over last 3-4 yrs funded out of internal accruals 🔹𝐄𝐦𝐞𝐫𝐠𝐢𝐧𝐠 𝐬𝐞𝐠𝐦𝐞𝐧𝐭𝐬 - 𝐂𝐨𝐬𝐦𝐞𝐭𝐢𝐜𝐬 (𝐡𝐢𝐠𝐡𝐞𝐫 𝐦𝐚𝐫𝐠𝐢𝐧) & 𝐕𝐞𝐭𝐞𝐫𝐢𝐧𝐚𝐫𝐲 - Setting up separate lines for these out of IPO funds - Focus is on increasing this contribution from 5% currently to 15-20% in next 3 yrs 🔹Capex from IPO funds : 𝟐.𝟓𝐱 𝐜𝐚𝐩𝐚𝐜𝐢𝐭𝐲 𝐛𝐲 𝐀𝐩𝐫’𝟐𝟔 (9 months from now) - 𝐑𝐞𝐯𝐞𝐧𝐮𝐞 𝐩𝐨𝐭𝐞𝐧𝐭𝐢𝐚𝐥 𝐨𝐟 𝟓𝟎𝟎-𝟓𝟓𝟎𝐂𝐫 ✅ 𝐩𝐨𝐬𝐭 𝐜𝐚𝐩𝐞𝐱 🔹Financials/Projections (conservative): FY25: Rev 105Cr ; PAT 13.4Cr FY26E: Rev 175Cr ; PAT 23-24Cr✅ 𝐅𝐘𝟐𝟕𝐄: 𝐑𝐞𝐯 𝟐𝟔𝟓𝐂𝐫 ; 𝐏𝐀𝐓 𝟑𝟖-𝟒𝟎𝐂𝐫 ✅ Margin profile in line with peers like Zeon Lifesciences (unlisted) gives additional comfort 🔹Peer comparison (can check tagged tweet) - 𝐭𝐫𝐚𝐝𝐢𝐧𝐠 𝐚𝐭 𝟔𝟎% 𝐝𝐢𝐬𝐜𝐨𝐮𝐧𝐭 𝐭𝐨 𝐨𝐭𝐡𝐞𝐫 𝐂𝐃𝐌𝐎 / 𝐜𝐨𝐧𝐬𝐮𝐦𝐞𝐫 𝐜𝐨𝐧𝐭𝐫𝐚𝐜𝐭 𝐦𝐟𝐫𝐬 - No direct competitors, covered proxies (CDMO pharma, Nutraceutical brand owners, Consumer contract mfr) _________________________________ Disc: Not a buy / sell reco | DYODD