Drew retweetledi

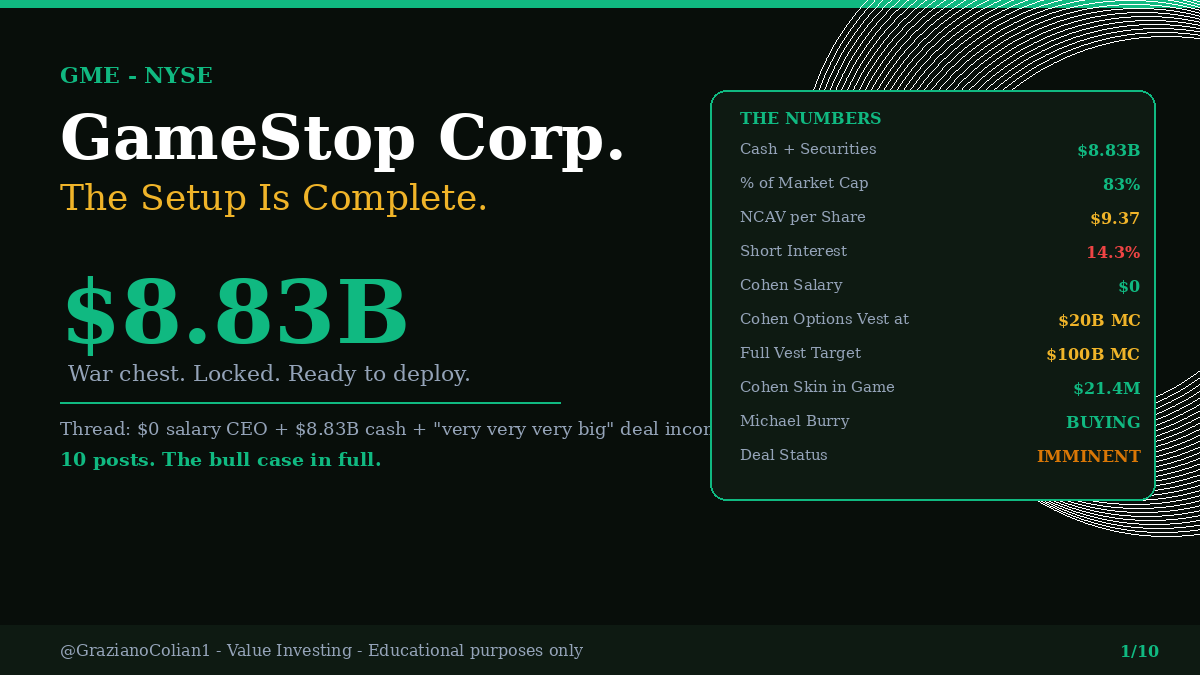

1/10

Everyone is sleeping on $GME.

$8.83 billion in cash. 83% of the entire market cap.

A CEO with $0 salary who only gets paid if the stock 10x's. A deal described as "very very very big" — and IMMINENT.

The setup is complete. 🧵

English