StandTrue

298 posts

StandTrue

@WisdomOfJustice

Warrior for truth & ⚖.

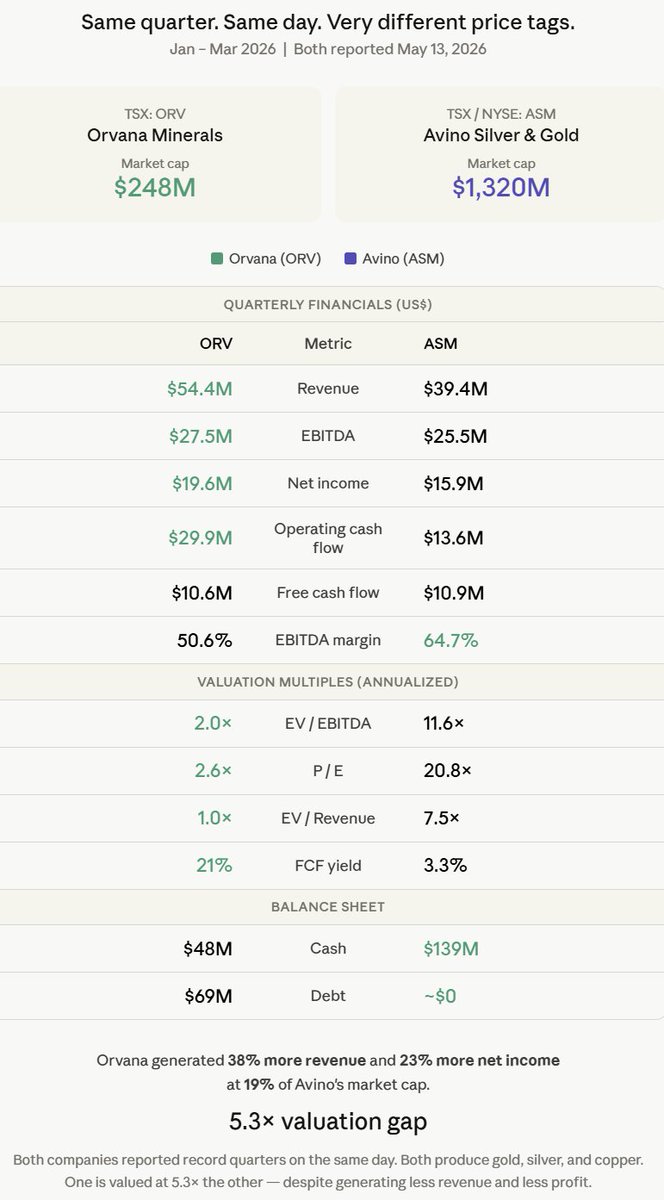

$ORV.TO - ORVANA vs $ASM.TO - AVINO Two mining companies reported record quarters on the same day. One generated 38% more revenue and 23% more net income, while also being undervalued having a 5.3× smaller market cap. Same metals. Same cycle. Very different price tags. ORV: $54.4M rev, $27.5M EBITDA, $19.6M net income, 50.6% EBITDA margin, market cap: $248M ASM: $39.4M rev, $25.5M EBITDA, $15.9M net income, 64.7% EBITDA margin, market cap: $1,320M Valuation gap: X5.3.

$ORV.TO $ORVMF - ORVANA MINERALS I have taken a massive position in ORV start of this week in anticipation of the ORV results for 2026 Q2. And indeed, the ORV results are extremely good. See the updated PF below. ORV is now 40.8% of the PF. I'll do some tweets on ORV today to explain the Q2 results. I'll also publish a full write-up on ORV today or tomorrow.

I heard all arguments on low LOM, bad assets, bad Management etc. But FCF rules together with right assets and technical teams. As an anecdote $vle.to CEO had very bad reputation before the Thai acquisitions and many Investors missed out despite seeing good Cash flows, assets etc

Silver jumps to highest price in more than 2 months 📈📈

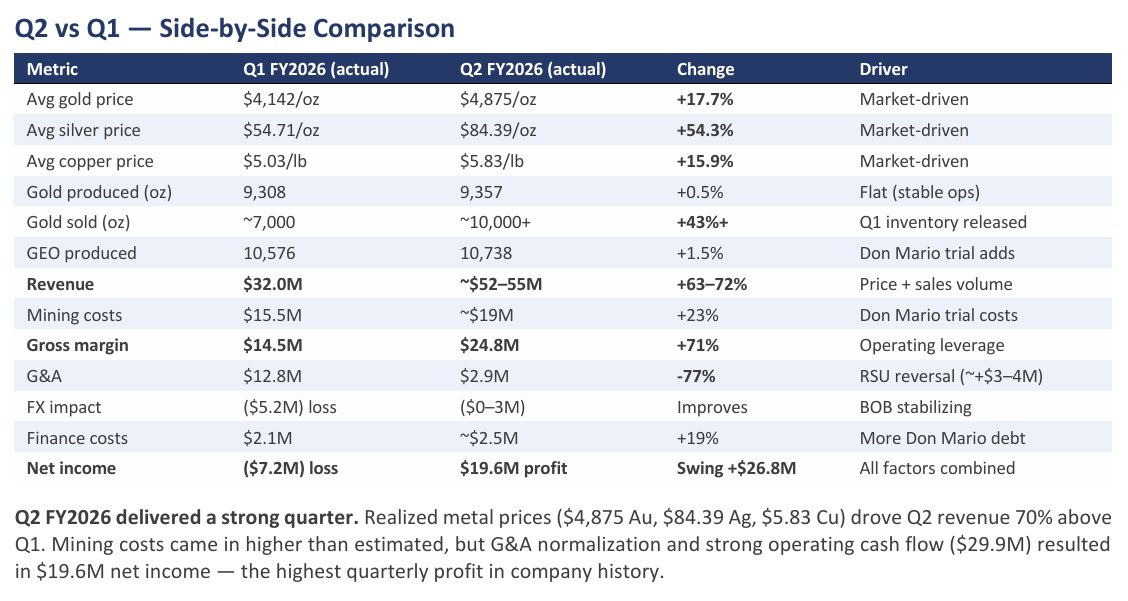

$ORV.TO $ORVMF - ORVANA MINERALS OCF of $29.9M on a $180M market cap, from one single mine (Spain only, Don Mario barely contributing), in one single quarter. That's a 66% annualized OCF yield from Orovalle alone — before Don Mario oxide processing even starts. Don Mario produced only 959 oz Au from trial processing. Oxide stockpile feeding hasn't even started yet. When it does (weeks away), Q3/Q4 should step-change again. Cash build: $48M cash on $68.7M total debt = net debt shrinking fast. At this OCF run rate, the entire debt stack gets wiped within 2–3 quarters of dual-mine production. The CEO's language on Taguas is careful but the geological confirmation is real — "vertically zoned hydrothermal system transitioning into a deeper porphyry setting." Assay results from the critical deep zone coming May–June. This is the binary catalyst. This resembles ATEX, a $1 billion company. Q2 Results: + Revenue +70% QoQ — $54.4M, a record quarter + OCF: -$0.8M → +$29.9M — $30.7M improvement + Net income: -$7.2M → +$19.6M — from loss to massive profit + Cash jumped to $48M — up from $32M, building a war chest during construction of Don Mario + AISC beating guidance — YTD $2,306/oz vs guidance $2,700–3,000 (costs running 20% below guidance midpoint) + Don Mario oxide feeding imminent — "expected to commence in the coming weeks" + FCF positive at $10.6M — while still spending $14.9M on CAPEX (mostly Don Mario construction) + Taguas porphyry transition confirmed — "vertically zoned hydrothermal system transitioning from high-sulfidation epithermal into a deeper porphyry setting." Assays coming May–June. Q2 Annualized Run-Rate Metrics (× 4):

⚡ ORVANA ANNOUNCES Q2 FY2026 RESULTS; PROVIDES UPDATE ON OXIDES STOCKPILE PROJECT AND TAGUAS DRILLING $ORV.TO Read more in CEOCA News: @newswire/orvana-announces-q2-fy2026-results-provides-update" target="_blank" rel="nofollow noopener">ceo.ca/@newswire/orva…

$ORV.TO - Orvana Minerals breaking out

#Copper is the only metal with strong fundamental arguments of undervaluation.

At current spot prices, Orvana Minerals’ Don Mario is achieving the "Holy Grail" of mining: Negative AISC. This means by-products cover 100% of costs—and then some. Here is the math on why the gold is effectively free. 🧵 $ORV.TO $ORVMF 1/5