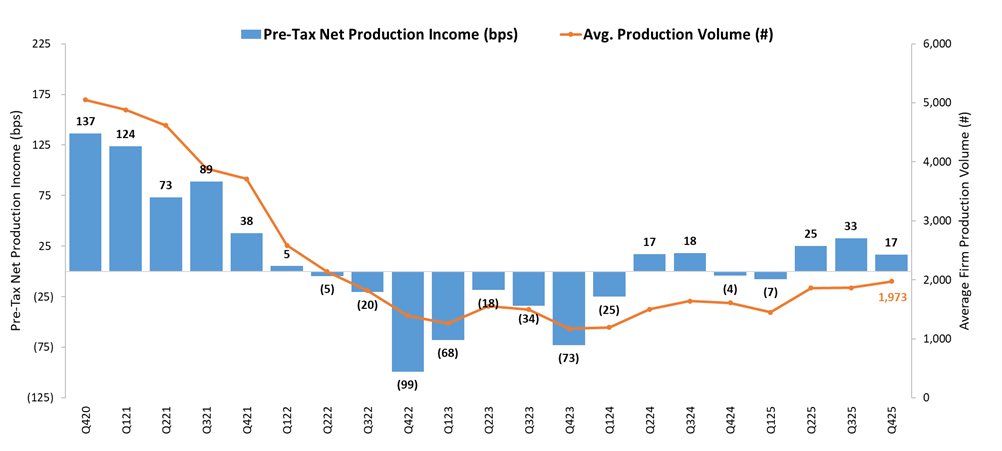

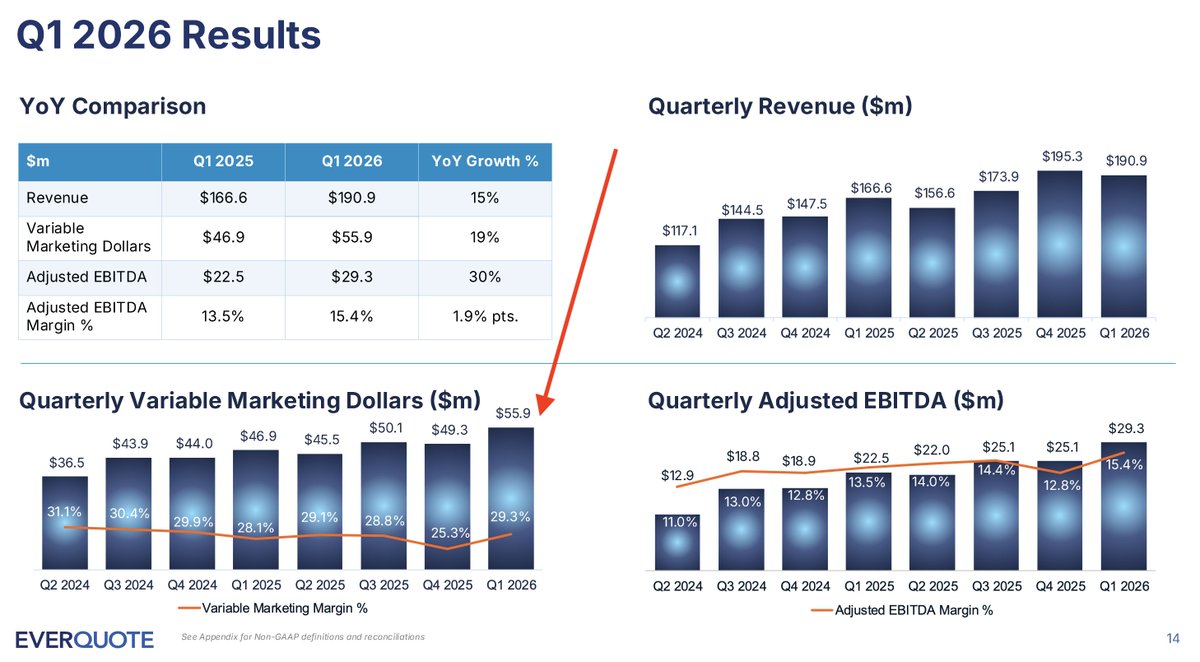

Big numbers out for $EVER and a solid pop. P&C insurance is just so strong right now. Amazing for a 356 person team to be trending over $600k+ per employee in VMD. Interested to hear what they have to say but more proof $GOOG $GOOGL is just fine for the paid players.

English