Higher oil isn’t the macro headwind it used to be.

In 2005 we imported 12.5 mmb/d net. today we export 2.8.

$100 crude pulls money out of US pockets, but it also flows back into US shale, gulf coast refining, and energy capex.

The net hit to GDP is a fraction of what it was.

And then you tie it to my prior chart, which showed that we’re still well below peak oil levels when adjusted for inflation.

The WTI year to date avg of $83 sits just above the 46-year average of $73, while the 1980 and 2008 peaks tower at ~$140-150.

102, the spot price is also 30-40% below  historical peak levels were adjusted for inflation.

If I fast forward 10 years, it’s hard to see the leading AI labs staying purely horizontal. I tend to think most of them will have to verticalize in some form, not just around models, but across compute, data, and distribution. The have to try owning more of the stack and tightening the loop between training, deployment, and user behavior. Hyperscalers are verticalizing the other way.

That doesn’t mean they all become the same kind of business, but it does suggest that being “just a model provider” likely won’t be enough.

I’d say, the ones that win probably control the full system, from infrastructure to application layer, where they can capture data, improve performance, and drive outcomes in a continuous cycle.

There’s a chance leading labs we know today don’t exist in 10 years. They are 1-2 model flops away from APIs re-routing…

Who wins? Who loses? :: $AMZN

“Amazon's custom AI chips are expected to save tens of billions in capital expenditures annually and provide several hundred basis points of operating margin advantage versus relying on third-party chips.”

Atlassian just gave one of the clearest signals I’ve seen that AI is not a headwind… it’s a real growth driver for certain software vendors.

They have an SBC issue for us but anyways. The data points are pretty hard to ignore:

• Customers using AI (Rovo) are growing ARR at ~2x the rate of non-AI users

• AI credit usage is growing 20%+ month-over-month

• Teamwork Collection users:

2x more AI credits per user

2x more agents deployed

AI users are seeing real productivity gains:

• 13% faster issue resolution

• 20% more issues resolved

Service Collection (AI-heavy offering):

• $1B+ ARR

• Growing 30%+ Y/Y

AI-driven workflows are delivering:

• 70%+ AI resolution rates (100K+ conversations)

• 6x faster post-incident reviews

• ~70% alert compression

Customers are:

• Signing bigger, longer deals

• Expanding seats

• Adopting more AI-driven products

I could keep going, but I’ll stop there with all the key data points.

$TEAM

Nearby payments.

Rolling out a pilot this week.

No QR codes. Just Bluetooth.

Great for getting paid by strangers. Or sorting a round at the bar.

Well done @DamjanStankovic and team on this beauty.

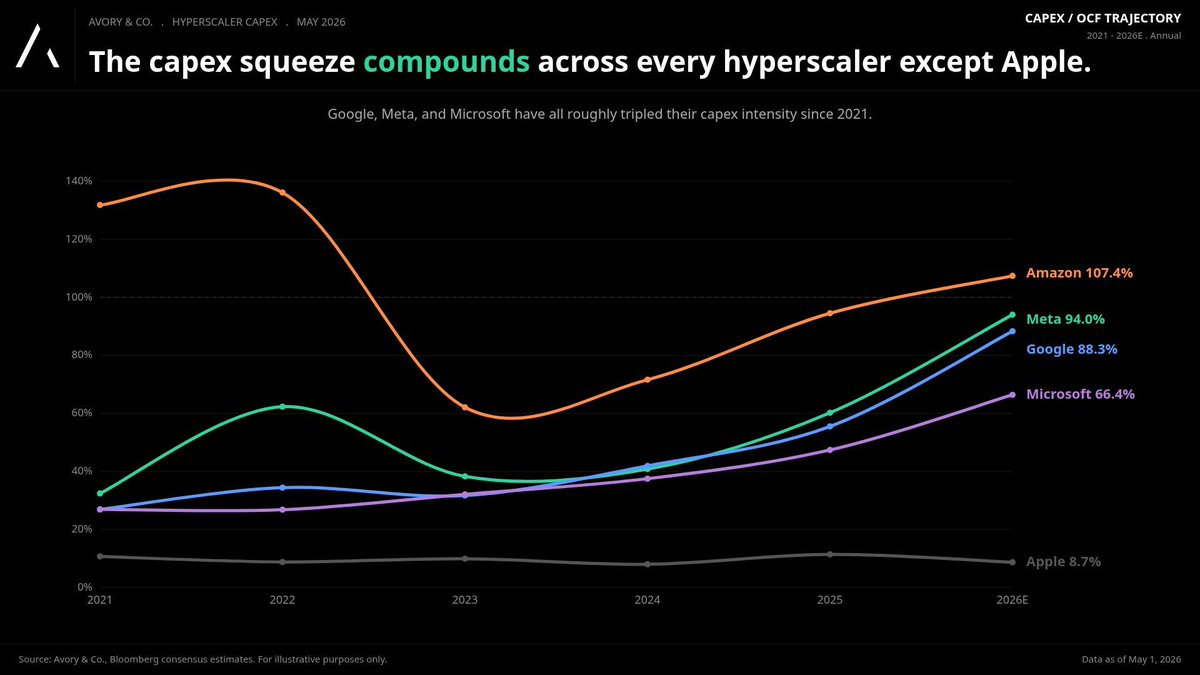

It’s pretty remarkable to watch how resilient hyper scaler margins have been.

Through post-COVID normalization, constant geopolitical noise, and now a massive AI-driven capex cycle, margins have largely held up.

They may look different as depreciation flows through, but what’s playing out right now feels like a real-time case study in operating leverage and reinvestment at scale. Crazy actually.

$AMZN $MSFT $META $AAPL

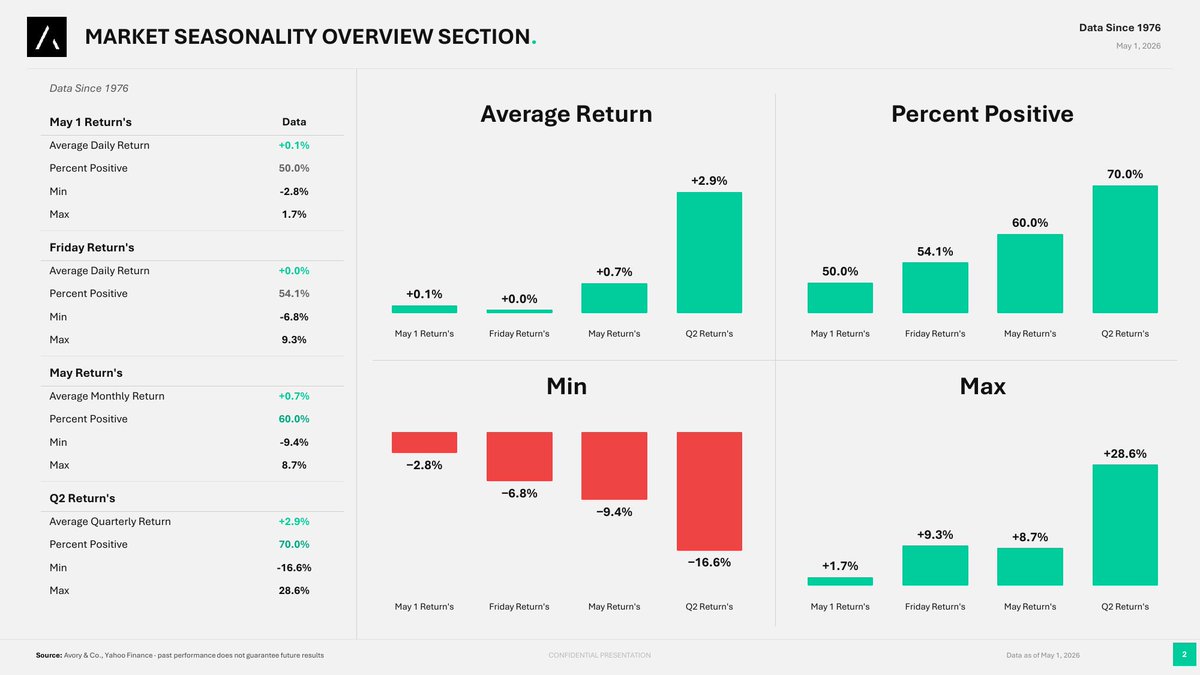

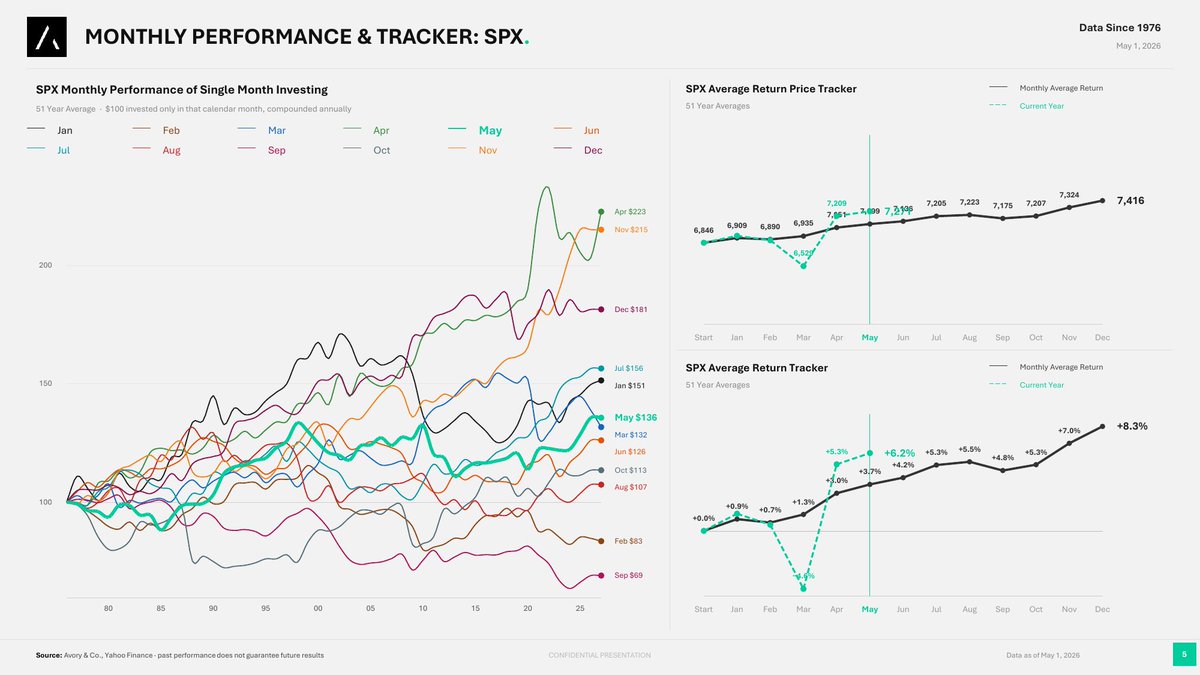

Sell in May" is one of the most repeated lines in markets. The data says it's wrong.

May is positive 60% of the time since 1976. June, July, August all positive too.

The actual ugly month? September.

Weekly data like this @ investingwithdata.substack.com

Ironically, looking at this chart, most investors would probably say the best businesses start on the left and move to the right.

Higher margins. Cleaner earnings. More obvious operating leverage.

But if we’re thinking about the ability to replicate these businesses, which I think is incredibly difficult for all of them, the takeaway may be different.

It is probably harder to replicate from right to left than left to right.

Amazon’s physical infrastructure, fulfillment network, cloud backbone, customer relationship, and commerce scale took decades to build.

Meta’s social graph, attention network, ad infrastructure, and AI distribution are also incredibly hard to recreate also.

So while the margin profile looks cleaner on the left, you could argue the more difficult businesses to replicate sit further to the right.

Lower margins is the enemy of competition.

$AMZN $MSFT $META $GOOGL $AAPL

What’s interesting is that Amazon has been here before from a capex standpoint as a percentage of operating cash flow.

The difference is that last time, the spend was focused on building out its distribution, warehouse, and physical footprint for the commerce business.

Today, the spend is focused on AI infrastructure.

But of all the companies building aggressively right now, Amazon and Meta (to some extent) are two of the few that have already lived through this kind of investment cycle before.

$META $AMZN $MSFT