Sabitlenmiş Tweet

ya3kov

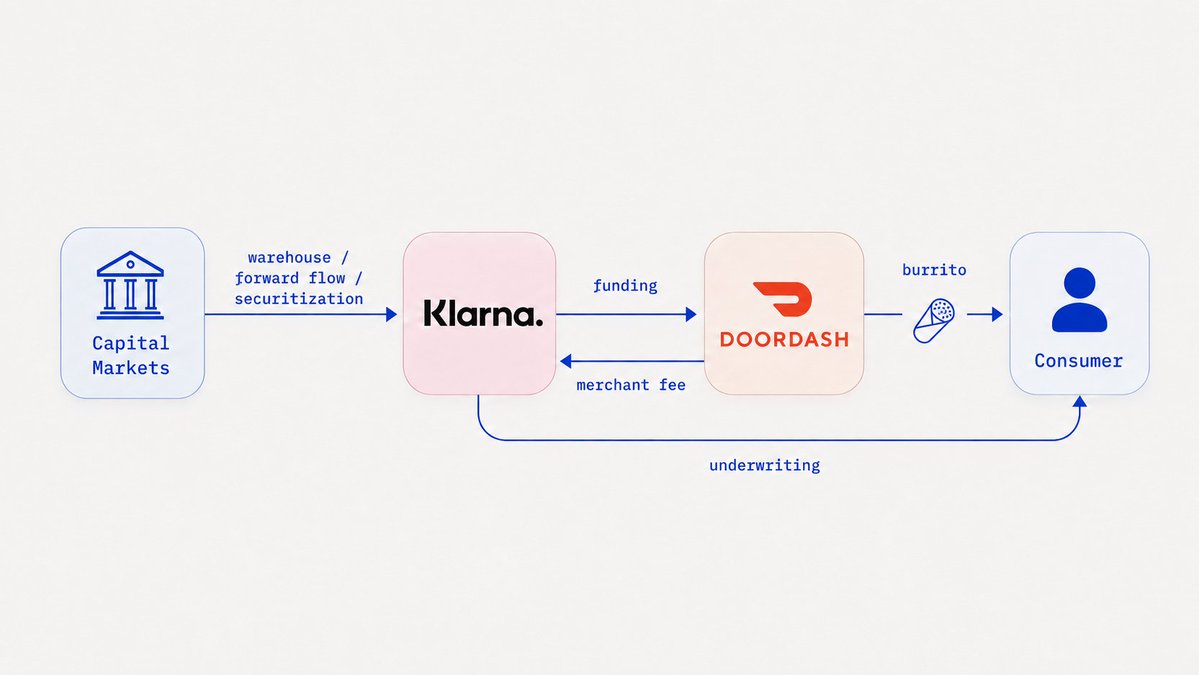

1.4K posts

ya3kov

@_yakovsky

founder @3janexyz. leverage is a God-given right

Katılım Ocak 2021

798 Takip Edilen4.8K Takipçiler

Native asset issuance has been postponed by 2 years until further notice.

Crypto Carl@CarlKVogel

English

Structured credit changed your life more than Michael Jordan, the iPod, & Youtube put together by shaving 200bps off your mortgage.

ABS, CDOs, synthetics are complex forms of financial engineering, and we believe they are the most fertile breeding ground for the next era of DeFi innovation.

Learn about the risks below.

3Jane@3janexyz

Structured financing for fintech lenders (ABF) is a $100B+ asset class with virtually no history of being exported into crypto markets, despite consistently generating 10%+ returns. Releasing a deeper analysis ahead of public launch: ➝ ELI5 warehouse loans & forward-flows ➝ Where the yield comes from ➝ Structured credit risk profile & loss distribution Full post below.

English

The quality of The Economist’s analysis - the supposed last bastion of ruthless empiricism - has dropped off a cliff over the past year. A once-sharp knife, devastatingly blunted . End of an era, @TheEconomist.

English

12/ The credit fund might offer to buy $10 worth of future burrito purchases for $9.85. Private credit fund gets their double-digit IRR and Klarna scales their loan book without tying up equity, keeps an origination/servicing fee, and recycles capital. Extremely capital-efficient

English

11/ Forward-Flow // 2

Klarna has purchased $4 of loans, proved their performance, & wants to scale to $10 of burrito purchases without raising equity to fund the warehouse first-loss slice. Klarna gets approached by a credit fund for a forward flow whole-loan purchase.

English

1/ DoorDash just reported 933M orders and $31.6B GOV in Q1.

In 2025 they added Klarna BNPL at checkout to drive growth. Most consumers still don't know who fronts the cash.

The capital markets rabbithole on how your burrito gets financed at 0% APR

Fiscal.ai@fiscal_ai

DoorDash reported 933 million orders in Q1, up 27% YoY. $DASH: +12.8% after hours

English

9/ Instead, Klarna approaches the bank and borrows $3 with interest, funds the $4 burrito order, & pledges the receivables as collateral with the bank at a 75% advance rate, keeping a first loss slice. Bank gets their yield and Klarna scales their loan book w/o giving up equity.

English

3/ Pay-in-4 BNPL is a unique credit product in that there is no interest typically associated with loans. Instead, Klarna/Affirm earn the "APR" off something called a "merchant fee" paid out by DoorDash. That fee varies and isn't publicly disclosed, but it can vary. Let's assume its 4%

English

2/ When you make an order, you have the option to pay interest-free in 4 installments. Klarna assesses your credit risk, looking at your credit data / other signals & then funds the order on your behalf. You get a burrito, DoorDash keeps a fee. So how does Klarna get paid?

English