A₹jun retweetledi

A₹jun

2.9K posts

A₹jun

@abhi3cr

Kumaoni (Uttarakhand) ,Tweets are personal opinion , Tweet on politics,sports and finance

Katılım Şubat 2021

425 Takip Edilen114 Takipçiler

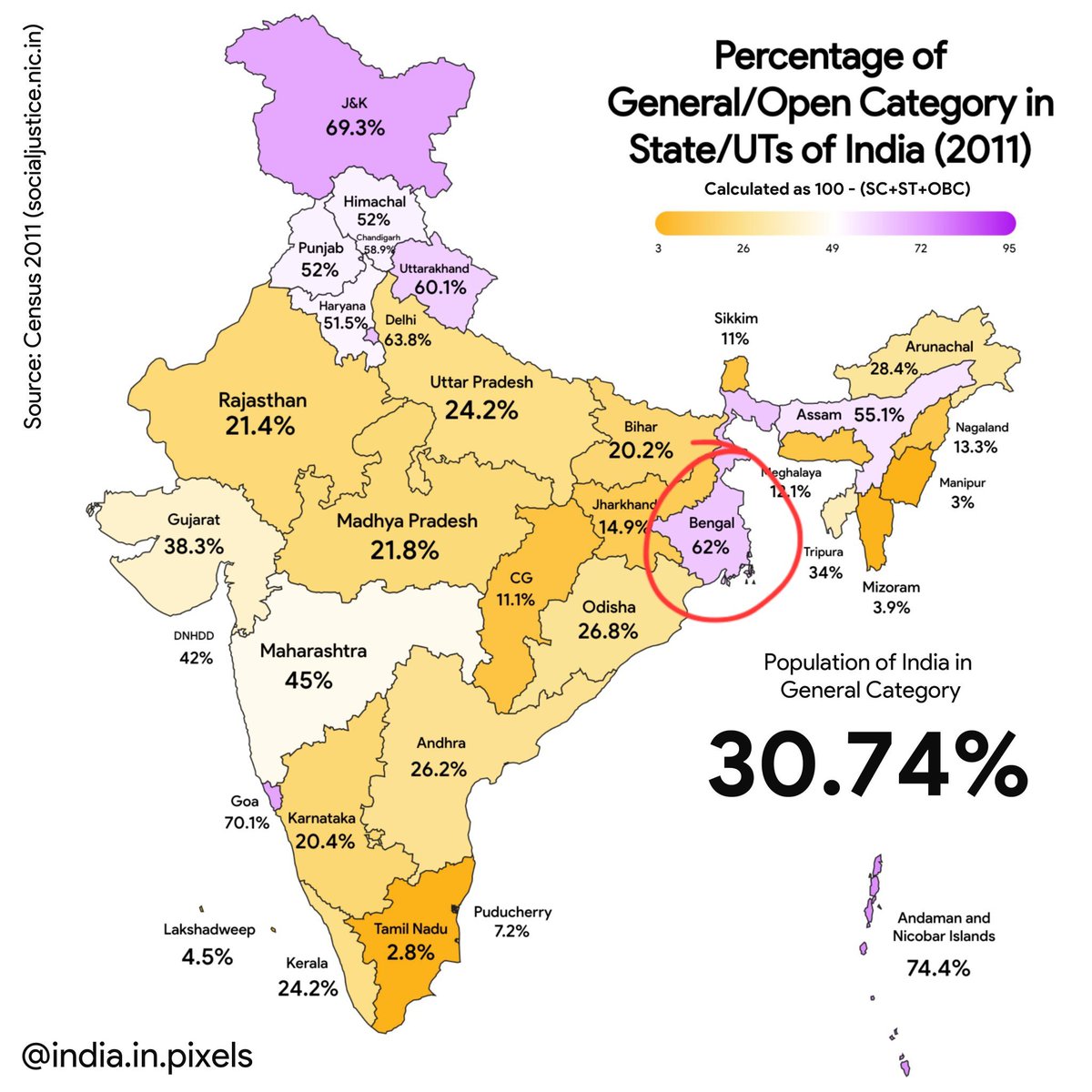

@neha_laldas Two points

1 General caste in uttarakhand is more than 70

2 Bengal People voted as hindu for their survival

Himachal,UP and Uttarakhand election will explain UGC impact

English

🤡

West bengal has high GC population-62%.

Take your caste BS elsewhere!!

Kushan Mitra@kushanmitra

Please remember that in Bengal, the @BJPBengal won because of the subaltern Hindu. The Dalit and Tribal Hindus. Not because of the Brahmin, Vaidya or Kayasth vote.

English

A₹jun retweetledi

Sterlite Tech still at 8x EV/EBITDA and 17x PE on FY28 numbers as per Nuvama's eestimates.

Feels too cheap for a turnaround story with order book momentum. What exit multiple are you penciling in?

#STLTech

English

A₹jun retweetledi

Indian Hume Pipe Co has got big orders with its JV Co!!

Rajeev Desai@rajuidesai

Indian Hume Pipe Company Ltd : CMP :Rs 274 1. Excellent Mar qr results. 2. Np up from 16 Cr to 44Cr. 3. Eps up from 3.30 to 8.30 4. Promo increasing stake. 5. OPM highest of many yrs at 18% in Mar qr. 6. Excellent BV of 157 7. Mcap of only 1443 Cr against sales of 1390 Cr. So quoting at 1:1 ratio. Cheap? Yes it is. 8. FV 2 but Mcap is very Low. 9. In Water management and Thermal Power plants. 10. Manf Prestressed Concrete for Railway sleepers! Do your DD. Take ur Call.

English

A₹jun retweetledi

Stocks i will be tracking next week.

Some EPs & High RS stocks in priority list.

#StocksInFocus #StockMarketIndia

English

A₹jun retweetledi

🚨 TOP 20 STOCKS THAT ABSOLUTELY CRUSHED Q4 FY26 🚨

A thread you CANNOT afford to miss if you're serious about markets 🧵👇

1/ 🟢 BHAGYANGR

46.3% revenue growth (guided 35-40%) + 258% PAT surge + ₹59 Cr CFO

Copper demerger on June 9th = massive catalyst incoming 🔥

2/ 🟢 NAVINFLUOR

992 bps margin expansion (crushed 28-30% guidance)

Debt/Equity now just 0.31x — this company is on a DELEVERAGING beast mode 💪

3/ 🟢 ETERNAL

Revenue nearly TRIPLED 📈 (+196.4%)

Quick Commerce: ₹265 Cr PROFIT vs ₹82 Cr LOSS last year

625.7% YoY growth. Read that again. 🤯

4/ 🟢 TIPSMUSIC

92.9% PAT growth 🎵

Beat 20% guidance by 10 FULL POINTS

Content costs at 10.2% vs 18% guided limit — insane capital discipline

5/ 🟢 ACUTAAS

33% revenue growth + 35.87% EBITDA margin (guided 28-30%)

CWIP surged 155% — capacity explosion is coming 🏭

6/ 🟢 CGCL

PAT of ₹9,491 Mn — beat guidance by 11.7%

ROE hit 16.49%... FY28 TARGET achieved in FY26 ⏰

2 years AHEAD of schedule. Wow.

7/ 🟢 SMARTWORKS

First FULL YEAR of profitability ✅

440 bps margin expansion

Crossed 10 MILLION sq ft operational portfolio 🏢

8/ 🟢 PHOENIXLTD

EBITDA margins at 60.8% vs 56-57% guidance 🏆

Residential segment surged 122.3% YoY

Mall + housing = unstoppable combo 🔥

9/ 🟢 EQUITASBNK

PAT grew 405% YoY 🚀🚀🚀

Provisions DROPPED 52%

GNPA: 2.60% | NNPA: 0.72%

All universal bank license criteria: ✅ MET

10/ 🟢 STLTECH

Enterprise/Data Center mix hit 36% (target was 30%) 📡

Turned PAT positive at ₹59 Cr

The strategic pivot is WORKING

11/ 🟢 TMB

Advances grew 20.78% vs 16% guidance

GNPA at multi-year LOW of 0.73% 📉

Quiet, consistent, and completely underrated 🤫

12/ 🟢 AURUM

₹505.4 Cr annualized ARR — target achieved ✅

91% DEBT REDUCTION — effectively debt-free 💰

1740 bps EBITDA margin expansion. Monster quarter.

13/ 🟢 VEDL

FY26 EBITDA beat guidance by 12% 🏅

Aluminum margins +1600 bps

Power segment EBITDA surged 365% ⚡

14/ 🟢 CHENNPETRO

PAT grew 1349% 🤯🤯🤯

GRM more than doubled to $9.28/bbl

Throughput at 111.5% CAPACITY UTILIZATION

Refining is back, baby 🛢️

15/ 🟢 CHOICEIN

PAT +39.1% (guided 25-30%) ✅

EBITDA margins beat guidance by 620 bps

Broking segment grew 110% 📊

16/ 🟢 ATUL

Life Science Chemicals margins expanded 921 bps 🧪

Free cash flow: ₹847.90 Cr

Virtually DEBT-FREE balance sheet

Turnaround of the year candidate 🏆

17/ 🟢 INFOBEAN

30.1% revenue growth vs mid-teen guidance 💻

PAT MORE THAN DOUBLED

Cash conversion ratio: 1.22x — quality earnings 💎

18/ 🟢 CEATLTD

PAT +47.7% — crushed double-digit guidance 🚗

D/E conservative at 0.60x

Dividend INCREASED by 350% 🎉

Tyre sector quietly printing money

19/ 🟢 FEDFINA

AUM growth 22.9% vs 12-15% guidance 🏦

Credit costs: 0.89% (well-controlled)

PAT grew 52.6% YoY

20/ 🟢 SEJALLTD

Glasstech hit EBITDA break-even 🪟

D/E collapsed from 4.16x to 0.99x via ₹94 Cr equity raise

Turnaround CONFIRMED ✅

🏁 SUMMARY THREAD:

✅ Guidance beats across revenue, margins & PAT

✅ Deleveraging stories picking up pace

✅ Turnarounds confirming in multiple sectors

✅ FY27 looks STRONG for these names

If this thread added value: Like, RT and comment your thoughts on the same.🔁

Follow for more data-driven market insights 📊

⚠️ NOT INVESTMENT ADVICE. Do your own research. Past performance ≠ future returns.

#StockMarket #NSE #BSE #IndianStocks #Investing #Q4Results #FY26Results #EarningsSeason #FundamentalAnalysis #StockScreener #Multibagger #ValueInvesting #GrowthStocks #EquityResearch #MarketAlpha #StockPicks #FinTwitter #dalalstreet #NIFTY #SENSEX #SmallCap #MidCap #LargeCap #TradingCommunity #WealthCreation #PortfolioManagement #EarningsCall #QuarterlyResults #MarketOutperformers #BeatTheStreet

English

Saurabh said to Mohit don't play with akansha and stick with ashmita

And after the show ,he completely flipped as per clout

Seriously if you are loved by people ,people change their identity and their opinion

#Splitsvilla16 #SplitsvillaX6

English

What Tayne and Sadhaf are doing in show

Literally no screentime no individual play ,even deeptanshu have lots of potential but he becomes 2nd Gauresh

#SplitsvillaX6 #Splitsvilla16

English

A₹jun retweetledi

To Dumb Gauresh is the sweetest revenge anushka can take from that bully gang

Why will anushka care about other emotions if no one cares for her

#SplitsvillaX6 #Splitsvilla16

English

Vishu was ready to be paired up with Preet

And now he is an ideal match with Suzzane

How can every one play with an exact partner this season ,how they guessed it so right

Completely Scripted

#Splitsvilla16

#SplitsvillaX6

English

@1no_aalsi_ You have no ground knowledge

In 30 lakh you will not get land in the ideal tier 3 in Uttarakhand

English

In small cities 30–35 lakh is enough including land.

narsa.🪺@rathor7_

How much would it cost to build a house like this?

English

A₹jun retweetledi

What a result from Mitsu Chem Plast!!

Np up from 3.54 Cr to 7.72 Cr🎯

Eps up from 2.61 to 5.69..🎯

OPM are Up!!

Whole year Eps is up 11.50 highest since 2017!!

Available below 10 P/E!!

Introducing new products, new capacities!!..

Rajeev Desai@rajuidesai

Mitsu Chem Plast Ltd: cmp: 182. 1. Excellent Dec Qr results. 2. Mcap is 220 Cr and sales is 300 Cr. 3. High promo stake of 73%. 4. FV 10 5. Sales going up every year. 6. In manf of Hospital furniture / beds. Do ur DD. Take ur call.

English

A₹jun retweetledi

One such critical mineral is in huge demand

"Tungsten" a hunt for haunt begins ❓⁉️

Interesting article on Tungsten to understand the reason for increase in surge globally

theoregongroup.substack.com/p/why-tungsten…

Also study the below for understanding the growth and demand of Tungsten with statistics

grandviewresearch.com/industry-analy…

English

A₹jun retweetledi

What Whales are buying? 🚨

Suba Hotels - Ashish Kacholia

True Colors - Mukul Agrawal

Tracxn Tech - Mukul Agrawal

OSEL Devices - Mukul Agrawal

TechD Cyber - Vijay Kedia

M & B Eng - Sunil Singhania

Yatharth Hospita - Vijay Kedia

Zelio E-Mob - Mukul Agrawal

Exato Tech - Vijay Kedia

English

A₹jun retweetledi

A₹jun retweetledi

Q4 concall notes of few companies that posted blockbuster results-

Acutaas chemicals

Sterlite Tech

RR kabel

HFCL

Acutaas chemicals:

- margin expanded to 42.4% driven by product mix

- revenue grew 33% yoy, pat grew 114%

- growth guidance of 30% & margins to be maintained (though i feel there's more upside from here)

- Phase 1 of electrolyte capex at Jagadia is completed and Phase 2 will be completed by Q1 27

- Battery chemicals capacity of 2000 tons for VC and FEC backed by long term contracts

- indichem JV to go live in 2H

- CDMO pipeline: 4 new products validated, expecting revenues of 50-100cr each

- 1000cr CDMO target by FY28

- semicon business should contribute meaningfully from next year

(can do 500cr pat by fy28 ~ 2000cr revenue)

Sterlite Tech:

- revenue grew 37% yoy, margin at 15.1%

- order book at 7309cr up 67% yoy, order inflows more than doubled to 7687cr

- opm margin target of 20% by EOY

- data center segment to scale up to 30% this fy

- market share gains in NA, 500cr capex planned

- Launched Hollow Core Fiber cable reducing latency by 35 to 40%

- G.654.E secured first commercial order

(i see 630cr PAT by FY28 ~ assuming 19% margins)

RR kabel:

- highest ever quarterly and annual revenue

- Target of 16-18% volume growth for w&c in FY27

- FMEG segment contributed 10% in sales, targets to achieve breakeven in FY27

- Expanding cable capacity every 6 months with capabilities increasing from 66 KV to 220 KV by FY28

- Targeting new growth opportunities in segments including data centers, wind, solar and infra.

- 1200cr capex between FY26 to 28

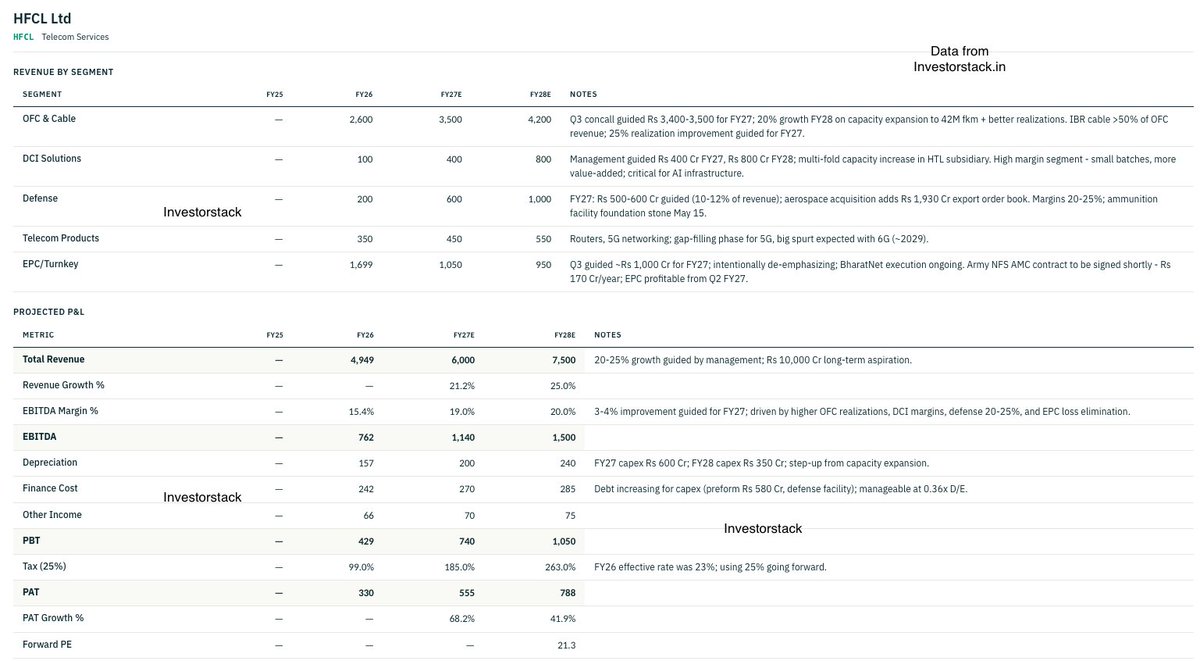

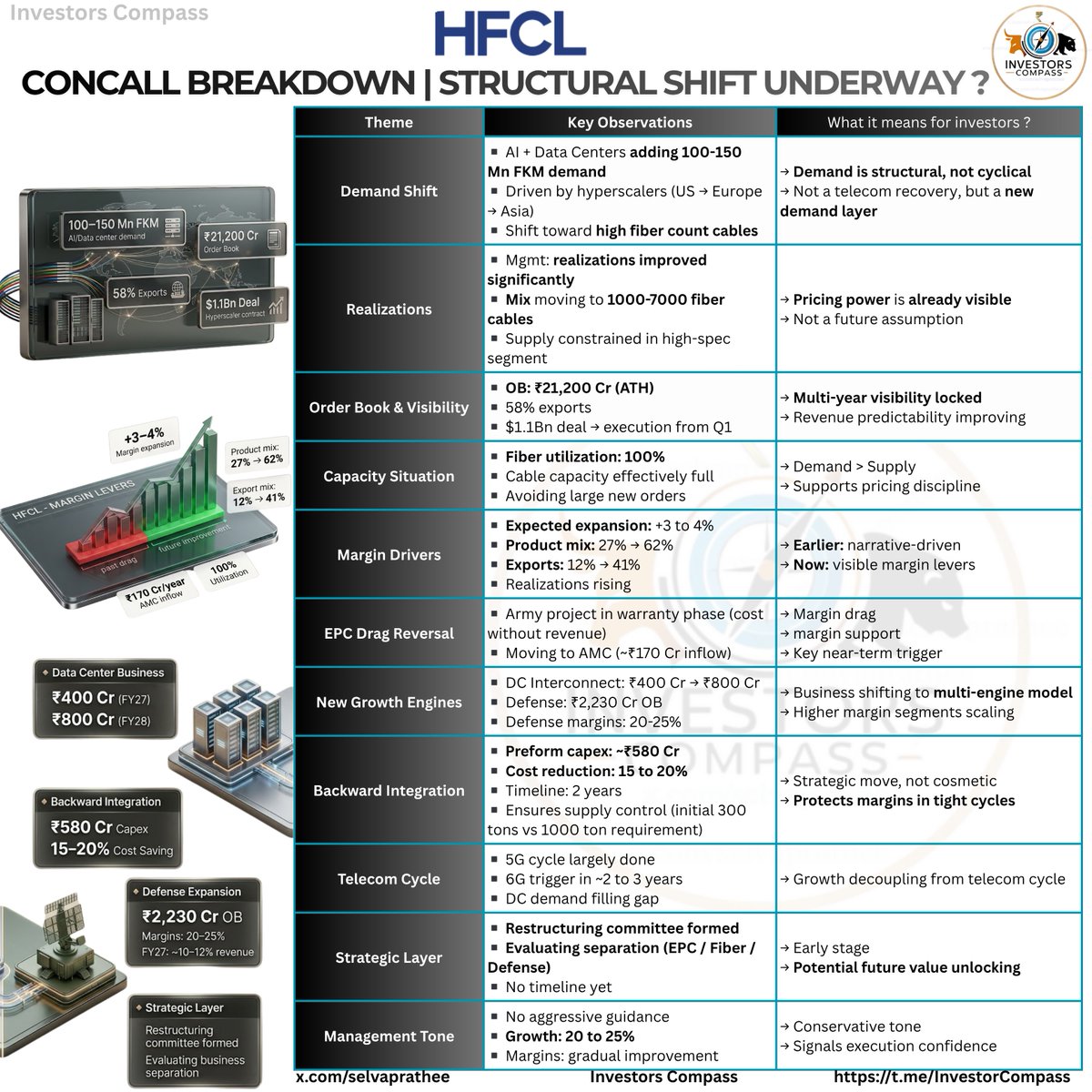

HFCL:

very interesting call & would suggest listening it instead of just reading summary.

- Order book at all time high of 21200cr, exports contributing 58%

- Setting up preform manufacturing facility with 580cr capex to lower costs by 15-20%

- Data center interconnect solutions to add 400 cr in FY27 and 800 cr in FY28

- 1.1 billion dollar global optical fiber cable supply contract starting end of Q

- Total defense order book expanded to 2230 cr

- Setting up ammunition facility in AP for hand grenades and artillery shells

- 20-25% growth for next year with margin expansion

- capex for FY27 at 600cr and FY28 at 350cr

English

@bhogleharsha Mumbai batting is not suited to score 220 above for continuous matches and in today's time batting improved a lot from 2020

There bowlers got criticism but there are no batsmen who can score with 200+ strike rates

They have lots of anchors

English

I must confess I didn't see a team, as studded with stars as #MumbaiIndians is, come apart like this. The only possible indicator could have been that, Bumrah apart, the others hadn't had an outstanding T20WC. But nobody could have predicted this. I had thought aloud about a hypothesis on my YT channel that reputation is becoming a burden in modern T20 cricket as a possible reason. I don't know if all the forces within were aligned but that could be another. And the experiment with Hardik Pandya as captain is now 3 years old and it has delivered a play-off only once so maybe something isn't working there. But I bet nobody saw #MI not making the play-offs.

English

A₹jun retweetledi

HFCL - Structural Shift Underway | Concall Breakdown

The most important shift here is not growth, it’s quality of growth.

- HFCL concall, points to a shift in growth quality, led by AI/data center demand (100 to 150 Mn FKM) driving higher realizations and shift to high fiber cables.

- Visibility is strong with a ₹21,200 Cr order book (58% exports) and a $1.1Bn deal (Q1 execution).

- With ~100% capacity utilization, management is prioritizing execution and selectively taking orders (read: demand strong, capacity catching up), while expansion is underway.

- Pricing is supportive but closer to peak levels.

- Margins have clearer levers with +3 to 4% expansion expected, driven by product mix (27%→62%), exports (12%→41%), and EPC drag reversal (~₹170 Cr AMC).

- Data center interconnect (₹400→₹800 Cr) and defense (~₹2,230 Cr OB, 20 to 25% margins, ~10 to 12% FY27 mix) are scaling as new engines, while preform capex ₹580 Cr (15 to 20% cost benefit, ~2 year timeline, initial 300 tons vs 1,000 tons requirement, aimed at supply control over availability) adds supply control.

- Telecom demand is stable post-5G (next major cycle 6G in ~2 to 3 years), with DC demand offsetting the gap.

- A strategic restructuring committee is evaluating business separation (no timeline), indicating potential future value unlocking.

- Management tone remains conservative (20 to 25% growth) despite strong tailwinds. Overall, transition toward a more diversified, margin-accretive model is visible, execution remains the key monitorable.

No Buy/Sell Recommendation

#StocksInFocus #StocksToWatch #HFCL #DC #OFC

English

A₹jun retweetledi