@cryptoCT7 @aleabitoreddit @_king142 Been hammered for a few days now 🤦♂️ may have bought at the wrong time

English

aiden convey

11 posts

@aleabitoreddit Taiwanese don't know how to promote themselves in the financial sector. Also, dumb local capital rules.

This announcement is the most bullish catalyst for $HIMS revenue re-acceleration to date. This is amid: - 30%+ of the float sold short - new $NVO partnership/lawsuit dropped - new global acquisitions - recovering macro climate. The share price is still $25, down from $70 last year. Short sellers are likely in trouble: $HIMS can capture market share at the ~70%-80% gross margins typical of their compounded products for the holy grail of the "Grey Market" TAM for peptides. - EG. Healing: BPC-157 and Thymosin beta-4 - Hair & Skin: GHK-Cu - Weight Loss & Muscle: MOTS-c and Ibutamoren And now they're probably the world's largest independent DTC distribution network to date from their new acquisitions... So just running a peptide protocol subscription between $150 to $300, for 200k subscribers is $360M+ in high-margin ARR. As just one example, but now they have a worldwide net of customers. They burned through capex last year to acquire peptide manufacturing facilities too... so now that's turned into a massive cash-cow business. I said $HIMS would need fundamental changes in order to force shorts to cover, and this is probably that signal as seen with market data. And $HIMS is turning into a fundamentally sound company after regulatory de-risking.

@aleabitoreddit They only went up those percentages because of your and other X accounts attention to those stocks combined with them being undervalued

@aleabitoreddit Was it you that mentioned Riber SA as well? $Alrib? It’s been flying as well.

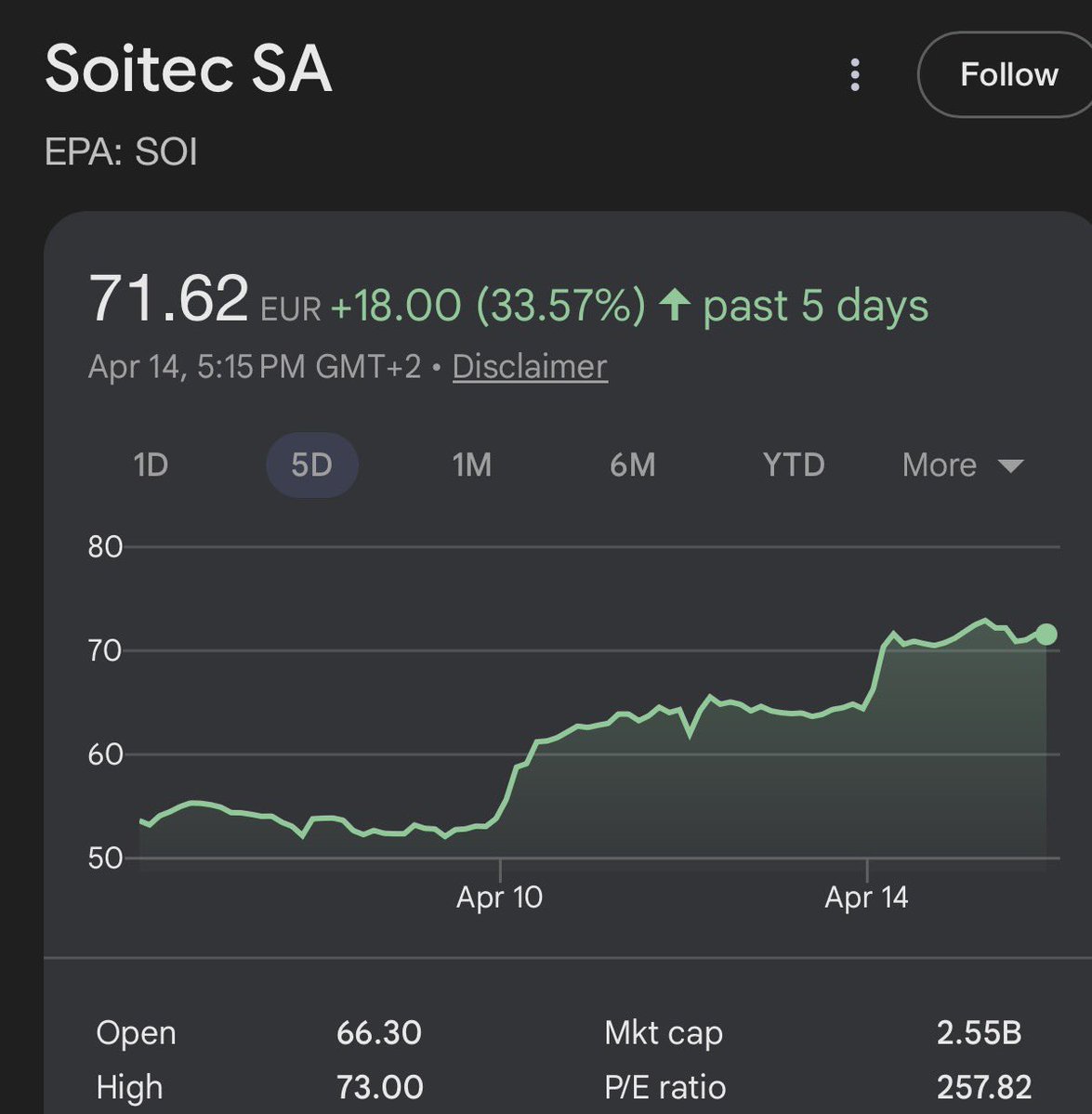

Changed my mind about Soitec ( $SLOIF ) and took a sizable position ~43 for CPO exposure. $NVDA GTC next week biggest catalyst pushing photonics and this architecture. ~1.5B euros MC. Trading at 1x book value and ~2x P/S (very depressed valuations) Genuine monopoly over substrates side for CPO (typically very premium valuations for photonics + even extra premium for monopoly status) Algos and analysts might get confused over market share but it’s an actual monopoly over SOI substrates since they give licenses to other players like Shin Etsu for diversification sake eg. $TSM doesn’t like just 1. I don’t think institutions will wait until next year to frontrun these names like Soitec or $TSEM (and most probably haven’t even heard of these names like $AXTI yet) This timing would be buying the likely bottom of the depressed smartphone cycle, while getting full upside of CPO mid-late 2027 + $NVDA GTC catalyst next week. I personally think it’s a 3x from here so I went long.