Sabitlenmiş Tweet

When have you ever had a scenario where a huge portion of a G7 country’s future space/sovereign defence budget can flow to one public company.

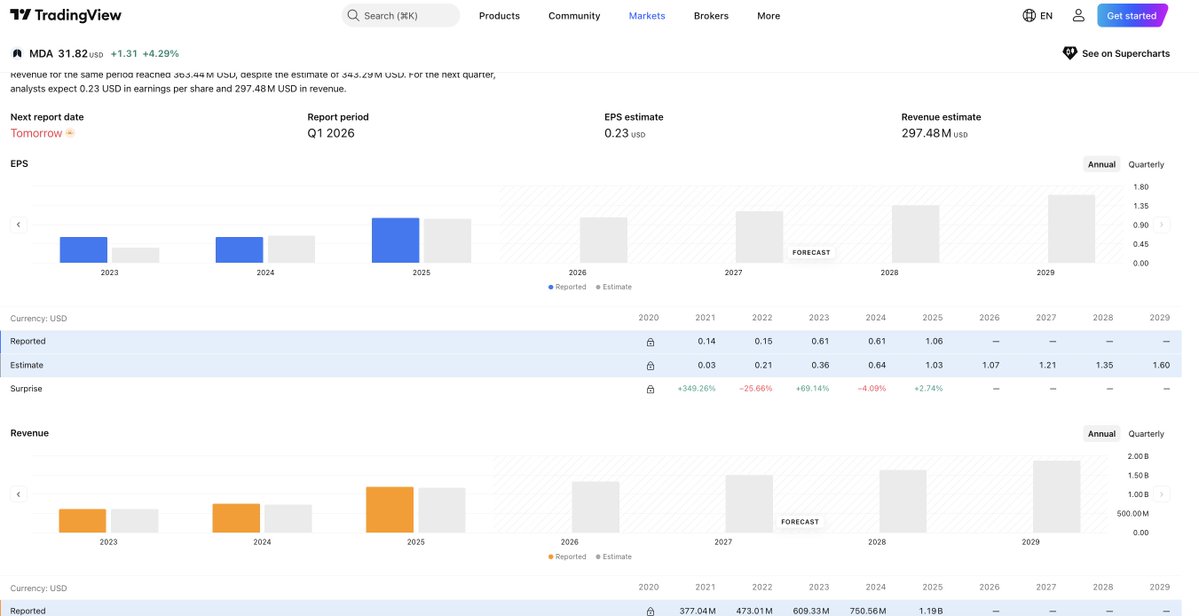

$MDA / $ MDA.TO / $ MDALF

• This is the five eyes and allies sovereignty thesis. $MDA is one of the only scaled non-US space primes that NATO and allied governments can lean on when they want sovereign space capability, but don’t want to be dependent on SpaceX and the US (industry still feeling effects of Musk/Ukraine).

• Canada moving hard towards its own space capabilities. Europe moving away from US (also US moving away from EU/NATO). Militaries need LEO comms, surveillance, Arctic coverage, maritime domain awareness, more satellites, etc. Sovereignty is the new trend and $MDA is a huge beneficiary. Laying out a bunch of catalysts below.

• Obviously $MDA is well known in the industry. Works or partnered with Airbus, TSAT GSAT LHX RKLB Hanwha ($000880.KS) VOYG/Starlab DND CSA ESA etc. All 5 US primes for SDA use components from $MDA

• Compared to US peers, valuation gap is crazy. $MDA is profitable, growing, already has insane ISS heritage, and since IPO on TSX (2021) the business has compounded revenue at ~32% CAGR but analysts are modeling future revenue growth till 2029 at 12% (!). Crazy that at a time where Canada is full steam ahead on defence /space/Arctic etc. that $MDA's growth significantly decelerates, whereas they were growing at 32% for the past 5 years when the industry was mainly US/foreign primes. Also, Canada does not have a bunch of primes competing for the same contracts, they are the ONLY Canadian scaled, trusted, space partner with decades of experience.

• Last earnings, $MDA showed a backlog of ~$4b CAD with a pipeline of ~$40b CAD. The pipeline DOUBLED year over year with $ 10b of that downselected to them. A lot of the below contract are still in the beginning /design phases. $MDA is about go on a huge run of contract award announcements (contract award list attached in thread)

• One of the biggest catalysts coming up is the ESCP-P (Polar mission). Yesterday during TSAT's earnings call, the CEO mentioned they are in advanced stages with the Canadian gov and it should be awarded over the coming months. This is a >$5b program none of which is not even recognized in the backlog yet (huge part of the 40b pipeline though). $MDA TSAT and CDN Gov already signed the strategic partnership on Dec 9.

• Another huge potential catalyst that no analyst is modelling is Defence Enhanced Surveillance from Space - Project (DESSP) which $MDA is a natural contender for. Although early and start definition is 2028/2029, this is another greater than $5 b CAD program that $MDA should get a huge chunk of since the contract is an upgrade to RADARSAT and $MDA already has a done of a ton of work there (even implementing RADARSAT heritage and experience in their new MDA Chorus product)

• The above is completely different than Lightspeed (which the TSAT constellation that got awarded to $MDA). Lightspeed is progressing well, on time, and ready for first launch end of 2026. TSAT mentioned lots of demand coming to them, also last quarter they updated their sats to add Ka-band/military payload. They mentioned this due to increasing demand and it shows how $MDA's Aurora platform is dual use and easily configurable. Current TSAT contract is for 198 satellites with option to add 100 more. With increased demand, TSAT could be looking sooner than later to extend (need to get past their lawsuit first)

• Another catalyst is the Surveillance of Space 2 Program. So far, $MDA has only awarded $32 million out of the $250 million to $499 million program. Expect some follow on awards there.

• $MDA is also part of the River Class Destroyer. They got $60 m for the first 3 ships for sensors. Canada is building 15 ships total, so you could get ~300 million over contract.

• They also spun off an internal subsidiary called 49North to focus on opportunities in Canadian defence tech. They've already done tons of work for Canada with River destroyer, UAVs, ISTAR, command/control, surveillance, Arctic, etc. So 49North is not starting from zero but having their own president presents more opportunities and focus.

• You also have the Amazon/GSAT thesis. This is purely a call option on $MDA. Obviously AMZN acquired GSAT and has plans to bring production in-house. But AMZN is likely to face some regulatory hurdles with their slower than expected roll out. $MDA is still contracted to finish building GSAT's C-3 (17 sats + the next 50). However, you got GSAT announcing in September Globalstar HIBLEO-XL-1 where it filed for up to 3,080 LEO satellites. $MDA is already the prime on Globalstar C-3 so more work potentially ahead if AMZN can't keep up?

• Hanwha 000880.KS signed MOU with MDA, but if you listen to Mike Greenley on podcasts and interviews, it seems like a collab on a military constellation for South Korea in exchange for Canada awarding the submarine deal to Hanwha (vs. TKMS). Submarine deal (whether it goes to Hanwha or TKMS) is expected to be awarded in June. Hanwha beefed up their offer big time, even sent the KSS III subm to Victoria which is being accompanied by 2 RCNs. Part of me thinks this lines up with a Canada/South Korea media PR campaign during award (could be wrong).

• $MDA also recently launched (and yesterday signed multiple contracts and LOIs) for MDA CHORUS. The reason CHORUS is different than other EO sats is because of RADARSAT heritage. Everyone might think its just another EO constellation but this is differentiated because of RADARSAT heritage which makes it more geared for military ops (specifically in Arctic) than a PL or BKSY. Recurring rev starting and re-pricing from space components to space data provider.

• Another underrated aspect of $MDA is Aurora D2D NTN (which was already a proven concept with Echostar SATS). Hiring is picking up in APAC and UK. During satcom, Mike Greenly ($MDA CEO) pitched building a neutral satellite network layer for MNOs and operators so they can offer terrestrial and NTN coverage without handing their customer/data relationship to a third party. Military angle is even more obvious too. Governments don’t want sovereign comms/data flowing to third party networks and will avoid doing that. I like the ASTS thesis, but if D2D ARPUs are real, sat costs keep falling, why wouldn’t MNOs or tower operators fund a consortium and keep the revs to themselves.

• You also got Starlab ($VOYG). Not a lot of investors know but $MDA owns a small equity stake (around 1%), and basically has a deal for SKYMAKER (their robotics Canadaarm). Yesterday VOYG seemed optimistic about the prospects of Starlab.

• Can't forget the increased Canada and EU space partnerships. They signed a classified info sharing agreement (which is pretty big). Canadian firms can also now bid on ESA programs: Moonlight, FutureNAV, ACCESS, and ERS-EO.

• Also, MDA is a prime for SkyPhi which is European and UK Space agencies to enable regenerative 5G D2D. Right now is still early days, but if it works (which I think it will), what's stopping them from building it out into a full constellation (similar to what SATS was trying to do).

• One of their more wellknown accomplishments in Space is the Canadaarm. Hard to find anyone else who has the advantage of over 25 years of robotics heritage on the ISS. Currently working on Canadaarm3 which is funded by the Canadian Space Agency and will be used for future lunar work as well (also on Starlab via Skymaker as mentioned above).

• They've got a solid balance sheet. Raised $300 million USD in NYSE listing in March. Mike literally said they have a shortlist of acquisitions in US and Europe (vid below). Could speculate all day here on who they acquire, maybe European supply chain, SpaceFlux type asset in UK, maybe AccelerComm if they want to enhance D2D NTN, maybe something in domestic launch/sovereign infrastructure, but don’t know and will keep looking.

• Recently listed on NYSE. No options yet, so adding that could be a nice boost. You also see institutions now can adding. Probably gets added to some US space/ aerospace ETFs over time. Dont know Russell rules well enough because Canadian HQ/foreign issuer issue, but I would imagine index / ETF ownership should improve from here.

• Can’t forget the Montreal facility. They went from being able to manufacture ~1 satellite per week to (with fill capacity expected in second half of 2026) to 2 Aurora digital sats per day. Very underrated and $MDA calling it world’s largest high-volume manufacturing facility in its satellite class. Management said they expect to sign 1-2 constellations in the next year. Perfect timing with the facility.

• Another catalyst is first orders for $MDA Midnight (guard sats). Japan, India, EU, etc. all exploring guard sats. With companies and governments putting high value assets in orbit (military comms) and all the talk about orbital data centers, you're going to need some protection. Canadaarm playing a huge role here.

• Can't not talk about the Golden Dome. $MDA was awarded SHIELD IDIQ followed by TSAT a month after. TSAT already adding lots of Ka-band and hinting to more military revenues. Canada also removed all restrictions on air and missile defence of Canada, which is them lining up to join. If/when Canada officially announces it's joining Golden Dome, these can pop. US needs Canada for this and they are basically shoeins for the contracts.

• In orbit refuelling and space debris is another theme that could get going soon. $MDA is already advanced there via MDA Midnight.

Now obviously space is heating up and lots of new entrants and everyone competing, but $MDA does not get enough credit (especially on fintwit). Canada literally named space and aerospace as sovereign capabilities under the new Defence Industrial Strategy. Canada hit 2% NATO and is targeting 5% by 2035. Arctic sovereignty is becoming actual policy. ESA agreement with Canada opens more doors to Europan programs. You can clearly see how MDA Space becomes Canada’s national defence and space champion + trusted supplier to allies globally (all for ~$4 billion USD marketcap all for the lowest forward EV/Sales in the industry - aside from value trap RDW).

Analysts still pricing $MDA like a space subcontractors while backlog is $4 billion, pipeline $40 billion, record revenue, profitable, new NYSE listing, national champion status, Canada defence budget inflecting, moving to recurring revenue, and MDA Space is one of the only prime beneficiaries in Canada. Carney literally said Canada will raise the share of defence acquisitions awarded to Canadian firms to 70%.

Earnings tomorrow morning.

Feels like the market still hasn’t fully priced what happens when a G7 country decides space is no longer optional, but core to national sovereignty, and there is basically only one scaled public Canadian space prime standing in the middle of it.

English