Amit GK

4.3K posts

Amit GK

@amitkal

Indian, Cricket Fanatic, Foodie, W̶a̶n̶n̶a̶b̶e̶ Entrepreneur, and your go-to Man for everything to do with Money and Marketing; not necessarily in that order

Mumbai Katılım Mayıs 2009

557 Takip Edilen286 Takipçiler

Main arterial junction of Worli Naka was blocked for hours

What others did does not justify what happened here

I also got stuck due to this, had to take a detour and was late by 30 minutes reaching my destination

What takes 15 mins took 45 minutes

Not justified by any argument.

Mr Sinha@Mrsinha

-Shahin Baug was blocked by Muslims for 100+ days : No issue -Singhu Border was blocked by "farmers" for 378+ days : No issue -A road in Mumbai was blocked for 10 min : Nonstop outrage We all know the reason...

English

@hermes_ooo India has three fun variations for the exact same addictive snack! 🇮🇳

Pani Puri in Mumbai

Gol Gappe in Delhi

Puchka in West Bengal

Same same but different 📷

That’s the beautiful unity in diversity of our country!

So glad you’re loving it too @hermes_ooo♥️

English

Amit GK@amitkal

BUILD AN EMERGENCY FUND A medical emergency, a layoff, and a family crisis all look the same to your bank account. An emergency fund is the single boring decision that prevents the most disasters. Yet most salaried Indians skip it. Either because it “doesn’t grow” or because they’ve convinced themselves their credit card is their emergency fund. It isn’t. It’s a 36% interest trap waiting to happen. The rules: 1. HOW MUCH: 6 months of household expenses. Not income. Expenses. Calculate what you actually need to survive: rent/EMI, groceries, utilities, school fees, insurance premiums, transport, essential medicines. Multiply by 6 if you are salaried. 12 if you are self employed. 2. WHERE: liquid fund or sweep-in FD. Not equity (too volatile). Not gold (too illiquid for an actual emergency). Not a regular savings account (too accessible, earns 2.5%). Liquid funds earn 6-7%, are safe, and take 1 working day to redeem. 3. Don’t touch it. Not for a vacation, not for “a great investment opportunity,” and definitely not for your cousin’s wedding. It’s there for one purpose: real emergencies. Medical, job loss, family crisis. How much, realistically: • Single, stable job: 3 months minimum, 6 target. • Married, single income: 6 months minimum. • Variable income (freelancer, business): 12 months. • Sole breadwinner with dependents: 9-12 months. Build it in phases. Don’t try to accumulate 6 months of expenses before doing anything else: • Phase 1 (Month 1-4): ₹50,000 or 1 month of expenses in a liquid fund. The “starter” emergency fund. Gets you past most small shocks. • Phase 2 (Month 5-12): Ramp to 3 months of expenses. You can slow down SIPs slightly to accelerate this. • Phase 3 (Year 2): Reach 6 months. Maintain it indefinitely. A client of ours, a senior analyst, no emergency fund, ₹40,000/month SIPs across three funds, had no cash cushion. In July 2023, his firm had sudden layoffs. He wasn’t laid off, but for him the penny had suddenly dropped. He realised he was one HR meeting away from a disaster. He saved ruthlessly, paused SIPs for 4 months, and built up ₹4.8 lakh in a liquid fund. Only then did he resume the SIPs. Two years later, his wife had a medical emergency which cost ₹3.2 lakh uncovered by insurance. He didn’t panic. He didn’t touch his investments. He wrote a single cheque from the liquid fund. Replenished it over the next 6 months. THIS money’s job is not to grow. It’s to be there at 2 am on a Tuesday when everything falls apart. Build yours. Start this month. — This is Week 18 of my book Less Talk, More Do 52 ideas. One week at a time. Dropping June 2026. #EmergencyFund #LiquidFund #FinancialSafety #RainyDayFund #FinancialResilience

QME

🇺🇸 Nearly 40% of Americans have less than $500 in savings.

14% have nothing at all, and about 45% couldn’t cover more than one month of expenses if their income stopped.

Two-thirds have already dipped into savings just to pay for essentials like food.

At the same time, the dollar has been weakening, hitting its lowest level since the Iran conflict began.

For millions, the financial cushion is already gone.

Source: The Street

Mario Nawfal@MarioNawfal

🇺🇸 Small businesses in the U.S. are acting like a crisis is already here. Only 16% plan to invest in the next 6 months, the lowest since 2009, down 12 points in just a few months. Before 2008 and during 2020, this figure was around 30-35%. High energy costs, policy uncertainty, taxes, labor issues, and inflation are all hitting at once. Main Street is pulling back hard. Source: @KobeissiLetter

English

@sachin_rt @dhruvjurel21 Sachin, I am sure you would remember this one by @JockMore too …

Those were the days when you guys inspired everyone to take up cricket 🏏

youtu.be/xQJfzjQn42U?si…

YouTube

English

Only one stump in sight, on the move, and done in the blink of an eye! Simply magnificent Dhruv Jurel!

English

@KP24 Reminded of a similar stumping done by one of the greatest Indian keepers @JockMore in the 1992 WC league games to get Martin Crowe out

Commentators were confused if it was a stumping or a run out 😀

Here goes: youtube.com/watch?v=xQJfzj…

YouTube

English

The greatest stumping ever in cricket

ESPNcricinfo@ESPNcricinfo

That's an unbelievable stumping from Dhruv Jurel 🤯

English

Interesting number crunching! Breaks a lot of myths around how they may have generated alpha.

Though, I have to disagree on the motive of "saleability" you mentioned here. If that alone drove their decisions, their product strategy would look entirely different.

Instead of maintaining just 3-4 core schemes, they would be pushing 30-40 different thematic funds to gather AUM, like much of the competition does.

They are one of the rare fund houses that actually practices strict value investing rather than just using it as a marketing slogan.

The cash is a byproduct of that discipline. It's a great lesson in behavioural finance.

Credit where it's due.

English

@May02nkG They hold cash to smooth volatility. A volatile fund doesn't sell in the fund management industry. This is something that all professionals in the industry know.

English

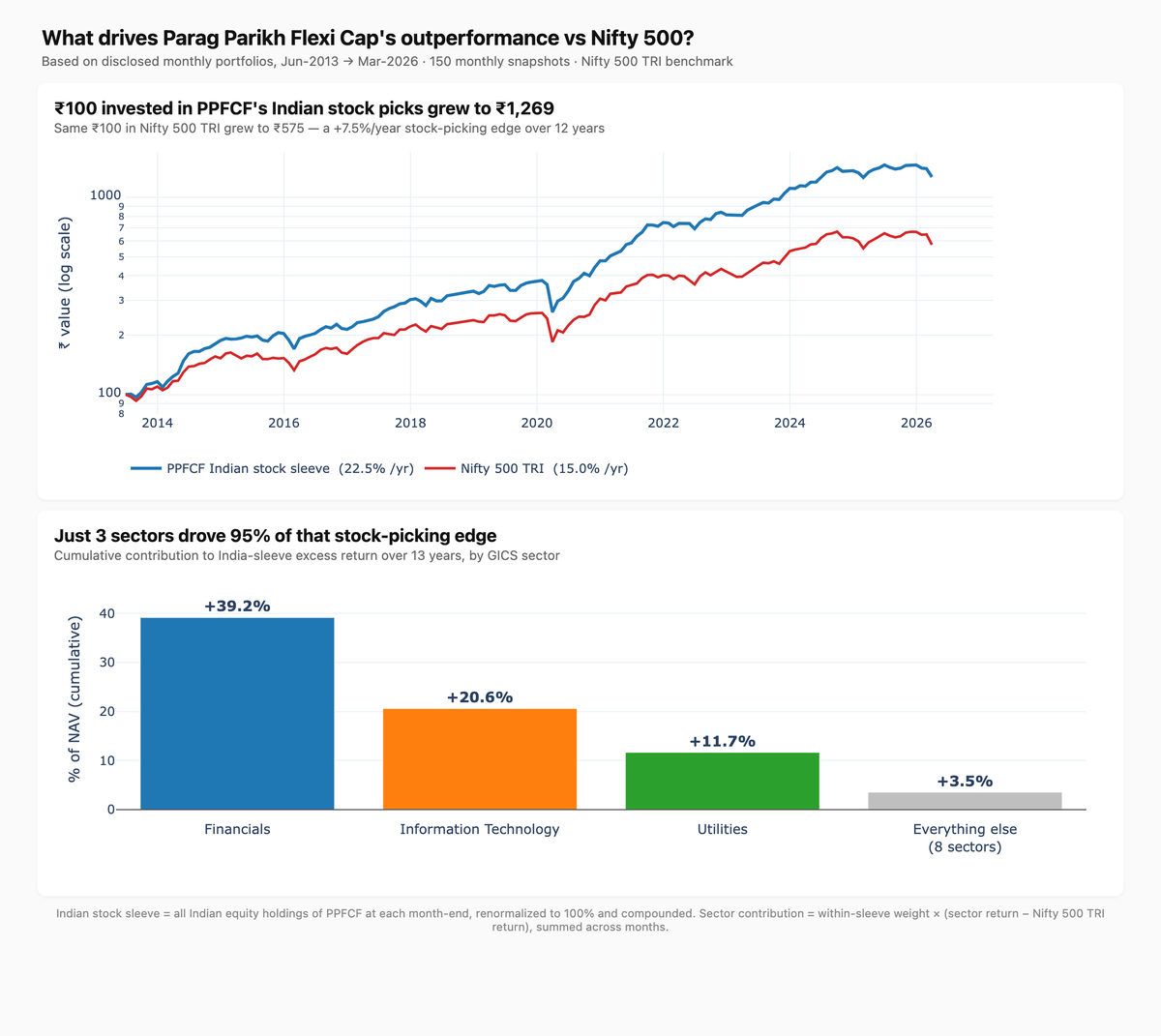

This is the real secret sauce behind Parag Parikh Flexi Cap’s success—and it’s not what you think.

Everyone attributes Parag Parikh Flexi Cap's success to its foreign stocks and cash discipline. I reconstructed 13 years of the fund from 160+ disclosed monthly portfolios. That story falls apart.

The fund has compounded at 17.9%/yr since June 2013. Nifty 500 TRI did 14.3%/yr over the same window. A clean 3.5-percentage-point edge.

Now decompose where that edge came from.

📊 Brinson attribution splits the excess into three pieces based on where the fund kept its money and how each bucket performed versus the Nifty 500. Over 13 years, cumulative:

→ Indian stock selection: +46.0%

→ Foreign equity tilt: +3.9%

→ Cash + arbitrage tilt: −20.6%

Read that last line again. Cash — the famous "dry powder" that PPFCF fans love to talk about — has cumulatively dragged the fund by 20 percentage points versus the benchmark.

Foreign added 3.9%. Meaningful, but not the engine.

The engine is one line. Indian stock selection.

🔬 Strip away foreign and cash. Look only at the Indian sleeve, renormalized to 100%. It compounded at 22.5%/yr. Nifty 500 TRI: 15.0%/yr. A 7.5%/year pure stock-picking edge. It beat the index in 12 of 14 calendar years.

🧪 Now the other common story: "PPFCF is really a value fund." Tested it. Tried to explain the India sleeve's excess return using the four classic style tilts — Value, Quality, Low Vol, and Momentum. They don't explain it. A mild quality lean, yes. A value tilt? Basically zero.

So, where does 7.5%/yr of selection alpha come from?

3 sectors:

→ Financials — 47% avg weight vs Nifty 500's 27% — contributed +39.2%

→ Information Technology — 12% vs 7% — +20.6%

→ Utilities — 8% vs 5% — +11.7%

3 sectors, ~95% of the total India-sleeve excess. The other 8 sectors were a wash.

And here's the tell. Financials and IT have both been through a rough patch recently. What is Parag Parikh doing? Adding. Not trimming. Not rotating. Same move they've made through every pullback of the last 13 years.

If you own Parag Parikh Flexi Cap because of Google and Microsoft, or because "they hold cash in bear markets" — that's not what you own.

You own a concentrated Indian stock-picker, structurally overweight Financials and IT, with demonstrable selection skill inside both.

Foreign is a side show. Cash has been a cost.

English

@darshitpatel84 Reminds of the epic dialogue from the original Border movie.

It's an ocean and investors of all shapes, sizes and life situations. Enough scope for everyone to live long and prosper.

English

Some people

Appearing daily on Zee Business to give buy/sell calls with a strike rate below 50%…

And then Tweeting negative about mutual funds…

Every day process…

English

BUILD AN EMERGENCY FUND

A medical emergency, a layoff, and a family crisis all look the same to your bank account.

An emergency fund is the single boring decision that prevents the most disasters. Yet most salaried Indians skip it. Either because it “doesn’t grow” or because they’ve convinced themselves their credit card is their emergency fund.

It isn’t. It’s a 36% interest trap waiting to happen.

The rules:

1. HOW MUCH: 6 months of household expenses. Not income. Expenses. Calculate what you actually need to survive: rent/EMI, groceries, utilities, school fees, insurance premiums, transport, essential medicines. Multiply by 6 if you are salaried. 12 if you are self employed.

2. WHERE: liquid fund or sweep-in FD. Not equity (too volatile). Not gold (too illiquid for an actual emergency). Not a regular savings account (too accessible, earns 2.5%). Liquid funds earn 6-7%, are safe, and take 1 working day to redeem.

3. Don’t touch it. Not for a vacation, not for “a great investment opportunity,” and definitely not for your cousin’s wedding. It’s there for one purpose: real emergencies. Medical, job loss, family crisis.

How much, realistically:

• Single, stable job: 3 months minimum, 6 target.

• Married, single income: 6 months minimum.

• Variable income (freelancer, business): 12 months.

• Sole breadwinner with dependents: 9-12 months.

Build it in phases. Don’t try to accumulate 6 months of expenses before doing anything else:

• Phase 1 (Month 1-4): ₹50,000 or 1 month of expenses in a liquid fund. The “starter” emergency fund. Gets you past most small shocks.

• Phase 2 (Month 5-12): Ramp to 3 months of expenses. You can slow down SIPs slightly to accelerate this.

• Phase 3 (Year 2): Reach 6 months. Maintain it indefinitely.

A client of ours, a senior analyst, no emergency fund, ₹40,000/month SIPs across three funds, had no cash cushion.

In July 2023, his firm had sudden layoffs. He wasn’t laid off, but for him the penny had suddenly dropped.

He realised he was one HR meeting away from a disaster. He saved ruthlessly, paused SIPs for 4 months, and built up ₹4.8 lakh in a liquid fund. Only then did he resume the SIPs.

Two years later, his wife had a medical emergency which cost ₹3.2 lakh uncovered by insurance. He didn’t panic. He didn’t touch his investments. He wrote a single cheque from the liquid fund. Replenished it over the next 6 months.

THIS money’s job is not to grow.

It’s to be there at 2 am on a Tuesday when everything falls apart.

Build yours.

Start this month.

—

This is Week 18 of my book

Less Talk, More Do

52 ideas. One week at a time.

Dropping June 2026.

#EmergencyFund #LiquidFund #FinancialSafety #RainyDayFund #FinancialResilience

English

PAY OFF YOUR DEBT FASTER

❄️ Snowball vs. Avalanche 🏔️

The “mathematically optimal” debt strategy is completely worthless if you abandon it in month 3.

Two schools of thought dominate debt payoff:

📉 Avalanche Method:

Pay minimums on everything, throw every extra rupee at the highest-interest debt first.

• Mathematically optimal

• Saves the most total interest

• Takes the longest to feel progress

⛄ Snowball Method:

Pay minimums on everything, throw every extra rupee at the smallest balance first.

• Suboptimal on paper (saves less interest)

• Closes debts fast! Each closed debt is a visible win

• Momentum compounds

The spreadsheet prefers Avalanche. 📊

The human brain prefers Snowball. 🧠

Which is better for you? Honestly ask yourself one question: Have I ever stuck with a 24-month disciplined plan before?

✅ If YES (you’ve run marathons, completed degrees part-time, built things over years):

Use Avalanche. You can delay gratification. Take the math win.

❌ If NO (you’ve started and stopped gym memberships, diets, side projects):

Use Snowball. You need the dopamine hits. Closing a ₹40,000 credit card balance in month 2 will keep you going. Closing an ₹8 lakh personal loan in month 30 will feel impossibly far away.

👥 A Real Example:

Two clients, similar debt profiles: around ₹7 lakh across 5 debts.

• Client A chose Avalanche. 3 months in, the highest-interest debt was barely moving. He gave up, went back to minimums, spiraled. Took 38 months with a restart.

• Client B chose Snowball. By month 3, he had closed 2 debts entirely. By month 12, half his debts were gone. Debt-free by month 24.

Avalanche is mathematically better. Snowball is behaviorally better.

BEHAVIOUR WINS EVERY TIME: because any plan you abandon saves you 0%. 💯

💡 The Hybrid Option:

Smallest by interest rate. If your debts are roughly similar in size, sort by rate. The psychology of Snowball + the logic of Avalanche.

Whichever you pick, follow these rules:

1️⃣ Pay minimums on everything. Late fees destroy the plan.

2️⃣ Throw every bonus, tax refund, and gift toward the target debt.

3️⃣ When one debt closes, roll its minimum into the next target debt. This is the “snowball” getting bigger.

4️⃣ Don’t take on new debt. Ever. This is a rule, not a preference. 🚫💳

Pick your method this week. Commit for 24 months. Stop overthinking it. ⏳

—

📖 More on this in Week 13 of:

LESS TALK, MORE DO

52 weeks, 52 actions, one book.

Coming June 2026.

#DebtSnowball #Avalanche #DebtStrategy #DebtPayoff #FinancialDiscipline

English

The bad thing about how the catch ended was his ex-captain and current captain were within handshake distance in the dugout.

Instead of getting up and giving him a pat on the back for a catch well taken they just chose to sit in their places.

IPL rivalries are coming in the way of national camaraderie. That too in a big way.

English

What made Shreyas Iyer’s catch so special was not just the athleticism, but the awareness behind it.

He had to judge the speed of the ball, the height, where the boundary rope was, how close he was to stepping on it, and get his jump absolutely perfect.

Then, while still in the air, he caught the ball and released it to a teammate before landing, all the while knowing exactly where that fielder was positioned.

To process all of that in a split second takes unbelievable awareness, timing, fitness, and composure.

@ShreyasIyer15 got everything spot on. One of the best catches I’ve ever seen live! x.com/IPL/status/204…

English

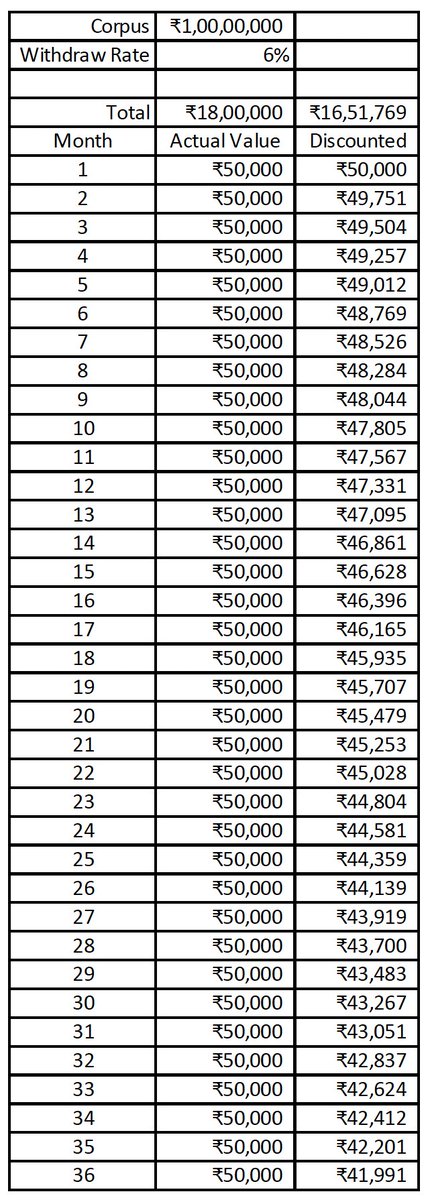

Yes. Lots of nuances other than the ones you mentioned too.

For someone looking at an SWP withdrawal rate of say 6%, the best case is to stash the first 16.5% (36 months discounted cashflow) in a pure liquid fund, and let the rest 83.5% stay in a well diversified equity portfolio.

That way even if there's a market fall, the equity portfolio has some runway and breathing space to recoup some of the losses.

You keep filling up the liquid pot opportunistically based on market gains, or according to a pre defined system. But never let it cross the 16.5% - 3 year threshold as then that will be come at an opportunity cost.

English

3 Big Risks of Using SWP for Regular Income from Mutual Funds

Many retired people or those needing monthly income use Systematic Withdrawal Plan (SWP) from mutual funds. It lets you take out a fixed amount regularly.

But if not planned well, SWP can slowly reduce your savings and create money problems. Here are 3 important risks explained simply:

1. Sequence of Returns Risk

If the market falls in the first few years when you start withdrawing, you have to sell more units at lower prices. This reduces your total savings faster, and even if the market recovers later, your money may not grow back fully.

2. Taking Out Too Much Money

Withdrawing a high percentage (like 8-10% per year) can finish your corpus quickly. A safer limit is usually around 5-6% or less, and you should increase it slowly with inflation.

3. Choosing the Wrong Funds

Putting all money in high-risk equity funds for SWP is dangerous. During market drops, regular withdrawals can hurt your capital badly. Better to use a mix of debt, hybrid, or balanced funds.

I feel one should Keep 2-3 years of expenses in safe funds first. Review your plan every year and consult a financial advisor before starting SWP.

Plan carefully to make your retirement money last longer.

#MutualFunds #RetirementPlanning #SWP #InvestingTips

English

@KP24 @Rajiv1841 I’ve watched that replay 10 times and I still don’t know how he stayed in the air that long. ✈️ Shreyas Iyer is playing on a different level of awareness this season. The hang-time, the flick back to Bartlett, the landing... pure machine behavior! 🦾

English

SHREYAS IS AN ABSOLUTE MACHINE

Mufaddal Vohra@mufaddal_vohra

SHREYAS IYER….. YOU ABSOLUTELY FREAK. 🤯 - The reaction of Rohit and Surya and an ice cold Celebration by Sarpanch Saab. 🥶

English

Fascinating perspective, Alok.

But there could be another hidden trend contributing to this volume:

using gold loans as pseudo bank lockers.

I know families taking loans at just 10-15% LTV. So taking a 1L loan by pledging 10L in jewellery.

Why?

The interest paid acts as a fee to get their gold securely stored, documented, and 100% insured. Traditional bank lockers don't offer that!

One of my clients was the product manager who thought of this idea for a south India based gold loan company who are now offering this for as little as a 10K loan.

The good thing for the company is that they can show more gold on their balance sheets leading to cheaper primary borrowings.

This may be the hidden jugaad or as you may put it, Dhan-de ki baat.

English

Why are Indians borrowing so much against gold?

I came across this Mint article—and it genuinely stunned me. (Article Link in comments)

There is a “frightening” surge in gold loans in India.

What the data says:

- Gold loan outstanding: ₹16.8 lakh crore (~4.7 crore borrowers)

- Now larger than personal loans (₹15.4 lakh crore; ~6.8 crore borrowers)

- Average ticket size: ~₹0.9 lakh → ~₹2 lakh

- Per borrower exposure: ₹1.9 lakh → ₹3.1 lakh

- Rising multiple, concurrent loans per borrower

- Early stress signals: delinquencies, wallet concentration, unsecured exposure

I don’t read this as growth. The velocity of gold loan growth? Incomes don’t scale like this

This feels eerily similar to the credit build-up cycles we’ve seen elsewhere. (USA credit cards)

People are borrowing more than they earn.

Why is this happening?

- Indian households hold massive idle gold reserves

-Gold prices have surged, making borrowing against it easy and tempting

What’s the risk?

Gold is becoming a liquidity crutch, not just a store of value :(

It’s the fallback when Cash flows don’t match life

Leverage is quietly building up across households

And a tougher question:

Are gold loans now funding lifestyle gaps?

Because for some borrowers, this may no longer be optional liquidity… but a last resort.

Is this the uncomfortable reality?

For decades, gold meant safety.

Today, it may be quietly funding consumption gaps.

A widening aspiration vs income gap

The real danger

Lack of awareness.

Do borrowers truly understand what it means to borrow against assets?

If gold prices correct, the loan liability stays the same, but what about the value of the pledged gold? What happens when there is a negative mismatch?

#dhandhekibaat: Spend only half of what you earn.

Your honest view?

Have you ever borrowed against family gold?

English

@joybhattacharj But the irony of it all is that the catch wont go on his name :|

English

Drop everything and see this catch. Outstanding!

lightningspeed@lightningspeedk

@joybhattacharj Here you go!

English

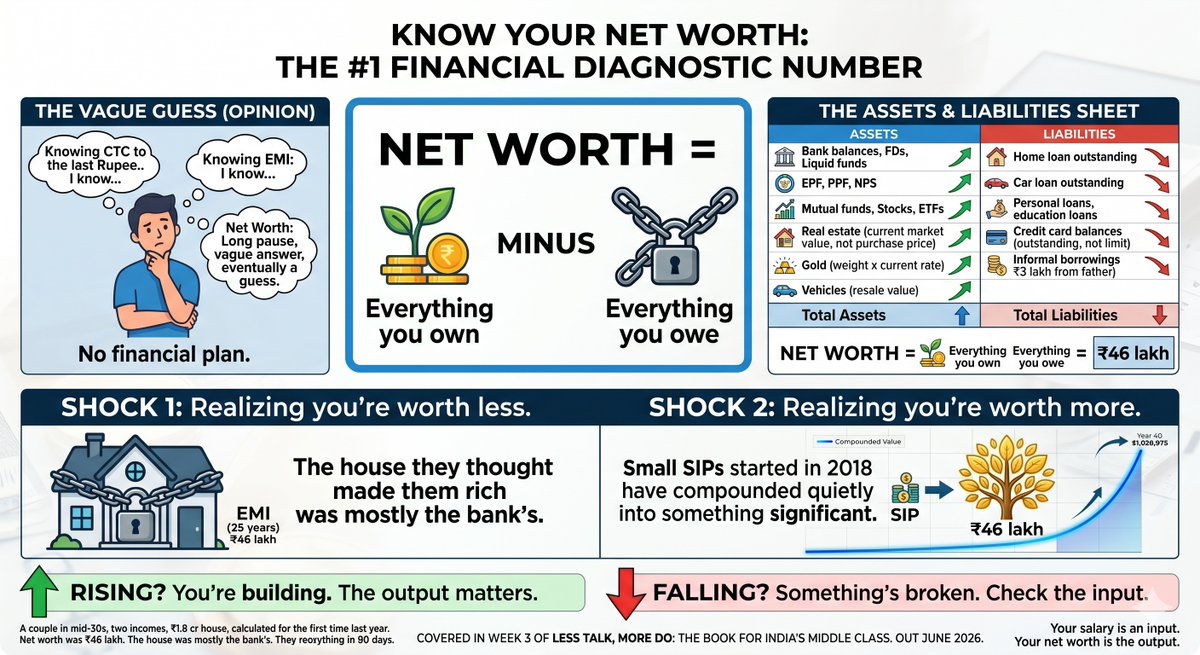

KNOW YOUR NET WORTH

If you don’t know your net worth, you don’t have a financial plan. You have opinions.

Ask a salaried person their CTC. They’ll quote it with pride to the last rupee. Their EMI. They know. Their net worth. Long pause, vague answer, eventually a guess.

This is the single most diagnostic number in your financial life, and most of you have never calculated it once.

NET WORTH =

Everything you own

Minus

Everything you owe

Not hard. Not optional. One number. One page.

Open a Google Sheet right now. Two columns:

Assets: - Bank balances, FDs, liquid funds - EPF, PPF, NPS - Mutual funds, stocks, ETFs - Real estate (current market value, not purchase price) - Gold (weight × current rate) - Vehicles (at resale value, not what you paid)

Liabilities: - Home loan outstanding - Car loan outstanding - Personal loans, education loans - Credit card balances (outstanding, not limit) - Any informal borrowings (yes, even the ₹3 lakh from your father)

Subtract liabilities from assets. That’s your number.

Most people are shocked in one of two directions.

Either they realise they’re worth less than they felt. Because they were counting the house but forgetting the 25 years of outstanding EMI.

Or they realise they’re worth more. Because small SIPs started in 2018 have quietly compounded into something quite significant.

Either way, you now have a baseline.

Redo this calculation every 3 months. Same format. Same sheet. The arrow matters more than the absolute number.

- Rising? You’re building.

- Flat? You’re leaking.

- Falling? Something’s broken.

A couple we advise, mid-30s, two incomes, ₹1.8 crore house, calculated it for the first time last year. Net worth was ₹46 lakh. The house they thought made them rich was mostly the bank’s. They restructured everything in 90 days.

Your salary is an input. Your net worth is the output. Track the output.

—

Covered in Week 3 of LESS TALK, MORE DO: the book I wrote for India’s middle class. Out June 2026.

#NetWorth #FinancialIndependence #IndianInvestor #WealthTracking #FinancialHealth

English

The Rule of 72

Your FD at 6% doubles your money in 12 years.

Equity at 12% doubles your money in 6 years.

The difference may seem linear but is not "double." It's exponential. And this one piece of mental arithmetic, that takes 10 seconds to learn, is the reason wealth in India is unequally distributed.

Here's the formula:

72 ÷ your annual return rate = years to double

That's it. No spreadsheet. No SIP calculator. A single division you can do at a traffic light.

Apply it to your life:

- Savings account at 3% → doubles in 24 years. By then, inflation has already halved its value. You lost.

- FD at 6% → doubles in 12 years. You tied.

- PPF at 7.1% → doubles in 10 years. You edged ahead.

- Well diversified mutual fund portfolio at 12% → doubles in 6 years. You compounded.

Now zoom out to 30 years — a full career:

- ₹10 lakh in an FD doubles roughly 2.5 times → becomes ~₹57 lakh.

- ₹10 lakh in equity doubles 5 times → becomes ~₹3.2 crore.

Same starting money. Same 30 years. The gap is not 2×. It's 5.6×

This is the part nobody in your joint family told you. Your uncle's advice to "keep it safe in FD" isn't conservative. It's expensive. Inflation is the enemy quietly halving your savings while you sleep. The FD just makes you feel like you're doing something.

@iRadhikaGupta tells a story I love.

She visited a Scottish whisky distillery. A 12-year bottle cost £50. An 18-year bottle (50% more age) cost £200. A 25-year bottle (only 10% more age than the 23-year one) cost £2,000.

youtube.com/shorts/IHa39gX…

Her punch line: "The same thing happens in equity."

Time does not add value in a straight line. It bends sharply upward near the end. The later years carry almost all the gain. Which is precisely why most investors — the ones who exit early, switch funds, panic during a crash — never actually meet those years.

The Rule of 72 is not just math. It's a decision filter.

Before every "safe" money move, run it through the rule. Then ask one question: am I tying, or am I compounding?

————————————————

This is one of 52 weekly actions in my upcoming book Less Talk, More Do — a 52-week action plan for India's middle class.

Launching June 2026.

Follow for one idea every week, from net worth to nominations to your FI number.

————————————————

#RuleOf72 #Compounding #EquityInvesting #PersonalFinanceIndia #SIP

YouTube

English

** AGING YOUR MONEY **

Most people think the hardest math they’ll ever do is Calculus in 12th grade.

But the real life "Advanced Mathematics" starts when you’re an adult trying to fit:

30 days of life into 20 days of salary. 🧮📉

We’ve turned the "Month-End Stretch" into a national sport.

We’re high-fliers on the 1st,

"budget-conscious" on the 15th, and

by the 25th, we’re checking if we have enough reward points on our credit card to buy basic groceries.

The problem is simple:

Our expenses have Vande Bharat speed, but our salary has Local Train stamina.

This is paycheck-to-paycheck living. And it is epidemic, even among people with decent salaries.

It is not an income problem. It is a structure problem.

I’ve been deep-diving into the "Age Your Money" philosophy, and it’s the ultimate cure for that "22nd-of-the-month" sinking feeling.

-------

The "Puraana Paisa" (Old Money) Logic

-------

In India, we respect "Old Money" families.

Now you can build your own version through some cash flow mechanics. The goal is to stop spending money you earned yesterday and start spending money you earned say 30+ days ago. ⏳💰

Jesse Mecham, creator of YNAB (You Need A Budget), calls this 'aging your money.' The concept is simple: instead of living on this month's salary, you build a buffer so that you are living on last month's salary.

THIS CHANGES EVERYTHING.

The salary that arrives on the 1st does not immediately get spent. Instead, it goes into a buffer to cover next month's expenses. By doing this, you break the month-to-month cycle. You are no longer a slave to the calendar.

When you’re spending last month’s salary to pay this month’s bills, the calendar stops being your enemy. If your geyser leaks or your maid asks for a double advance, you don't panic. Why? Because that expense is being covered by the "You" from 45 days ago.

Building this buffer takes time, usually 1-3 months of discipline. But once it exists, the psychological shift is enormous. Suddenly you have breathing room. An unexpected expense does not become a crisis. It just comes out of your buffer, which you then replenish over the next month.

The "Cashback Trap" vs. Systemic Timing

We love to obsess over the small stuff. We’ll spend 20 minutes hunting for a ₹50 cashback code or haggling with the vegetable vendor for free dhaniya, yet we quietly ignore the thousands leaking out of our accounts because our timing is broken. 💸

Wealth isn't built on tiny, exhausting sacrifices; it’s built on Systemic Timing. If you’re earning a great salary but spending it on the 1st to pay for things you bought last month (the Credit Card Float), you’re still broke. You’re just a high-earning person in a debt-trap. You're playing a T20 match when you should be playing a Test Match. 🏏

--------------------

Less Talk, More Do 👊

I’m tired of finance books that feel like they were written for someone living in a vacuum. Our financial lives are messy. We have joint family pressures, sudden shaadi seasons, and an inflation rate that eats FDs for breakfast.

That’s why I’m finishing up my book: “Less Talk, More Do.” It’s not a book of "ideas" or motivational quotes. It’s a tactical manual. No fluff. Just the exact, slightly ruthless systems I use to:

Reading doesn't pay the bills. Execution does.

If you’re done with the monthly "30 vs 20" math and want to be the first to know when the “Less Talk, More Do” pre-order drops, just reply with a "YES" below. 👇

Let’s stop surviving the month and start owning it. 💰🔥📈

--------------------

English

Most Indians are masters at "Saving" but absolute rookies at Wealth Building. ❌

We’ll haggle for 10 mins over the price of tamatar, then quietly let inflation rob 7% of our purchasing power every year.

I just finished 'Profit Plus' by Mike Michalowicz and it’s a masterclass in breaking this cycle.

amzn.to/4cIP6JB

The book was written for entrepreneurs. But the principle underneath it is not a business principle. It is a human behaviour principle. And it applies to your household with the same force it applies to a company.

The core idea was deceptively simple.

Take your profit first, then run the business on what remains. Michalowicz built the system around multiple bank accounts, each with a designated purpose.

Every rupee that enters the system is immediately assigned a job before it can be spent on impulse.

It flips the script from the tired 'Surplus' mindset (save what is left) to a 'Profit First' mindset.

The Game-Changer? The Five-Bank-Account-System. 🏦

Stop the "one-account chaos" where your salary vanishes into a black hole of bills and shaadi gifts. Instead, treat your household income like a business.

Every rupee that hits your Income Account gets split immediately:

1️⃣ PROFIT: Your wealth builder. Taken FIRST. (Routed to SIPs/Assets)

2️⃣ OWNER’S PAY: Your guilt-free lifestyle money.

3️⃣ TAX: No more "March 31st panic" for Income Tax

4️⃣ OPEX: The daily kharcha, bills, and groceries.

5️⃣ INCOME: The hub where all inflows land.

Why this works in India: 🇮🇳

This system forces you to be your own fund manager. By fixing your percentages and automating the transfers, you kill "lifestyle creep" before it kills your future.

Western gurus tell you to skip the $5 latte.

Bro, skipping a ₹20 cutting chai isn't making you a Crorepati. 😂

The math only changes when you change the SYSTEM.

Profit Plus is modern-day Chanakya Neeti for your bank account—ruthless, strategic, and light-years ahead of the "boring savings" trap.

--------------------------------

Let’s be real: Reading 50 books changes nothing.

Action changes everything. 👊

I’m currently distilling these strategies into a 100% Desi execution plan in my upcoming book:

“Less Talk, More Do.”

No fluff. Just the exact "How-To" for families and businesses to implement systems like this and actually see the bank balance grow. 📈

Time to move from Gyaan to real Growth.

If you want to be the first to know when the “Less Talk, More Do” pre-orders drop, and want a sample chapter, follow and reply with a "YES" below. 👇

Who’s ready to play offense? 💰🔥

--------------------------------

English

@theliverdoc @bossafzal5 Keep at it doc. You never know, enough resistance will give them pause. After all, how many can they silence?

English

I am sorry everyone, we all know who is coming after me. Maybe goodbyes are in order.

English