Ashton Invests@Ashton_1nvests

I think some of the best opportunities in the market right now are not the most hyped stocks.

They are the companies where the fundamentals are clearly improving, but the stock price has not fully caught up yet.

Revenue is growing.

Margins are improving.

Free cash flow is expanding.

Guidance is moving higher.

But the market is still stuck on an old narrative.

That is where I think the opportunity is.

Here are a few stocks I believe fit that setup perfectly:

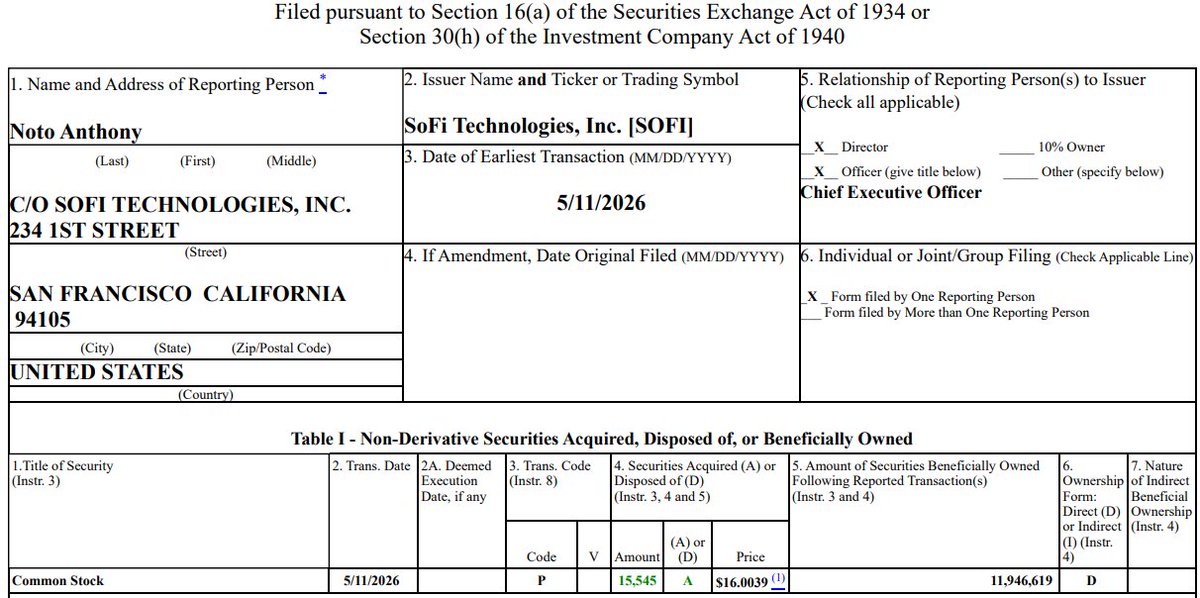

1/ $SOFI

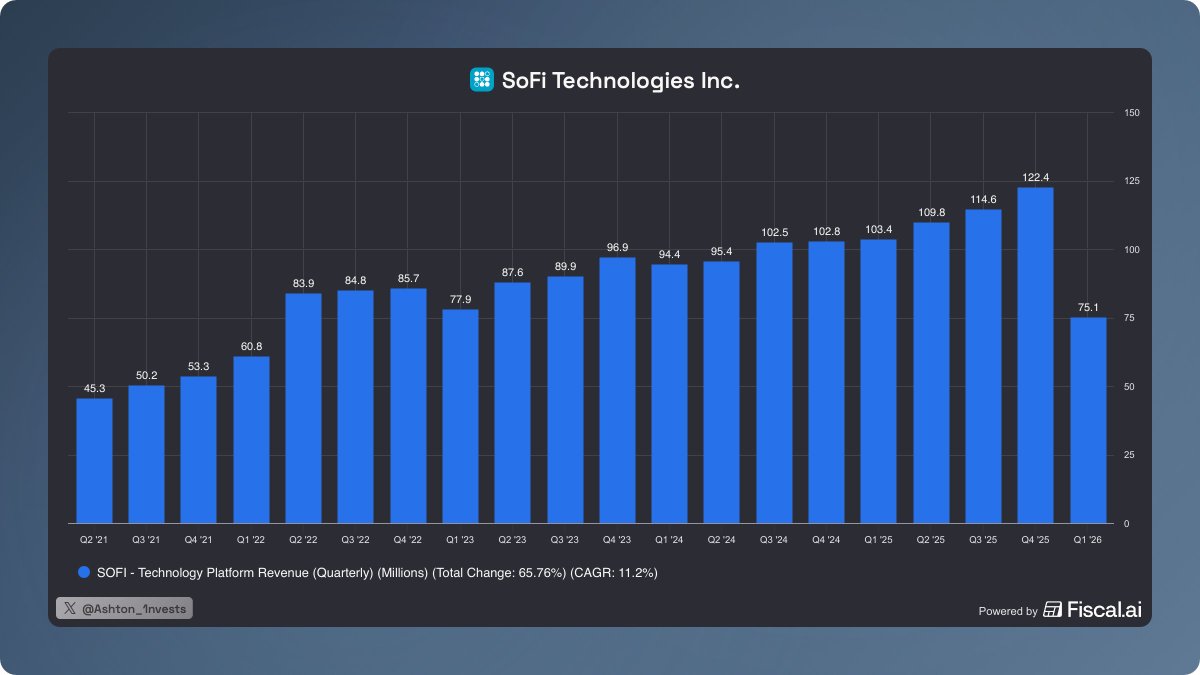

$SOFI is still one of the clearest examples of a company where the business is improving faster than the stock is being rewarded.

The market still treats SoFi like a risky lending business, but the company continues to become more diversified every quarter.

Members are growing rapidly, products continue to expand, deposits are scaling, financial services revenue keeps becoming a bigger part of the story, and profitability is finally starting to show up in a real way.

That matters because the bear case for years was simple:

“Cool growth story, but where are the profits?”

Now the company is answering that.

SoFi is no longer just proving that it can grow. It is proving that it can grow while becoming profitable, while lowering its dependence on one part of the business, and while building an ecosystem that becomes more valuable with every new member.

The stock might still trade like the market does not believe the story yet, but the fundamentals are moving in the right direction.

That disconnect is exactly why I still think $SOFI is one of the most interesting long-term opportunities in the market.