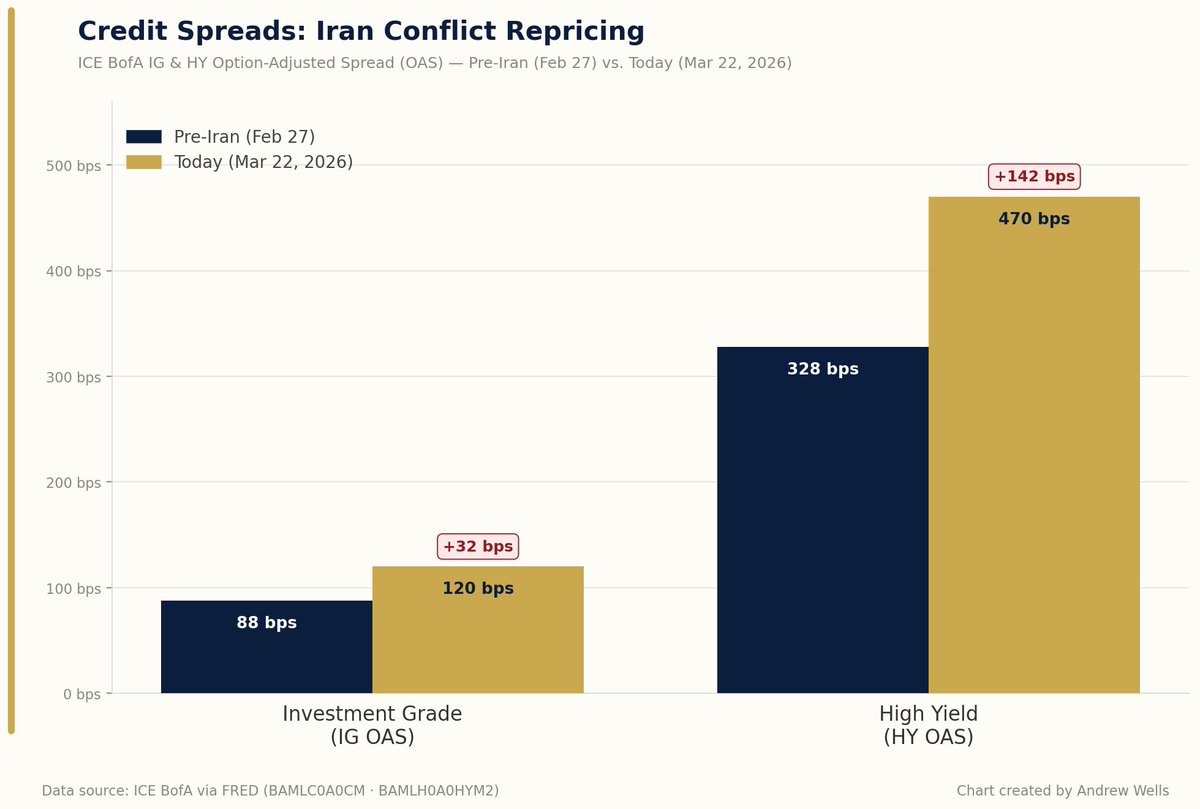

𝗖𝗥𝗘𝗗𝗜𝗧 𝗦𝗣𝗥𝗘𝗔𝗗𝗦: 𝗜𝗿𝗮𝗻 𝗖𝗼𝗻𝗳𝗹𝗶𝗰𝗧 𝗥𝗲𝗽𝗿𝗶𝗰𝗶𝗻𝗴

📊 Credit markets are finally starting to price what the geopolitical calendar has been screaming for three weeks.

Investment-grade spreads (OAS) have widened from 88 bps to 120 bps since the Iran conflict broke out February 28, a 36% move in less than four weeks.

High yield has been hit harder; HY OAS has surged from roughly 328 bps to 470 bps, a 142 bp move that reflects genuine risk-off repositioning, not a blip.

Here is the structural problem. Credit spreads typically widen during geopolitical stress, then recover when the shock fades and the Fed provides cover.

That second part is not available this time. The Fed cannot ease into an energy-driven inflation spike. There is no policy backstop for spread widening when the same conflict generating fear is also generating CPI pressure. The spread-compression trade that worked in every prior geopolitical episode since 2001 relies on a rate cut that is not coming.

Add a refinancing wall, where billions in corporate debt locked in at 3 to 4% is now rolling over at 6 to 7%, and the fundamental case for tight spreads starts to erode. IG at 120 bps is wider than January but still historically tight. It is not pricing a hard landing. HY at 470 bps is getting there.

The question is not whether spreads widen further. It is whether the pace matters before the Fed blinks.

#FixedIncome #CreditMarkets #MacroViews #BondMarket #CreditSpreads

English