I’m calling it now: 2026 is going to be the year of operating leverage.

It’s why I believe operator-heavy funds will outperform investor-only funds over the next cycle.

For years, returns could be driven by:

- Cheap leverage

- Multiple expansion

- Aggressive underwriting

That environment masked a lot of operational gaps. But today, those crutches are gone.

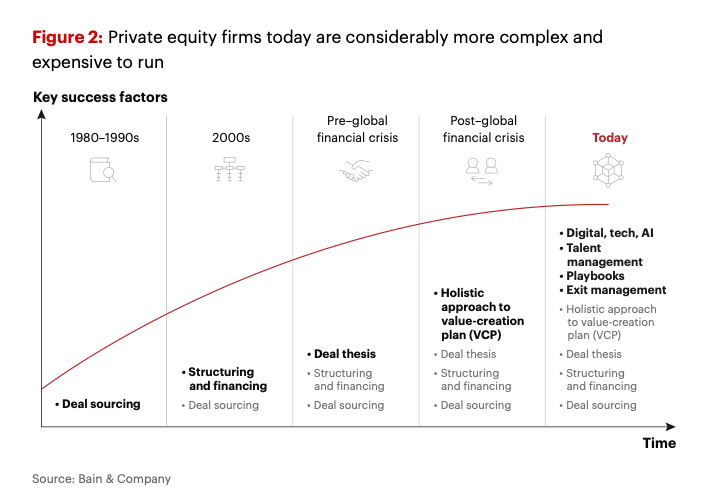

What’s become increasingly obvious, especially across mid-market and upper middle market portfolios, is how uneven operating benches actually are.

Smaller funds often can’t afford deep operator teams. That’s understandable. But what’s more surprising is how much variation exists even at the mega-fund level.

Some firms have Executives-in-Residence, functional experts in finance, procurement, HR, and GTM, and repeatable playbooks across portfolios. But others still rely on ad hoc help and expect management teams to “figure it out.”

That difference shows up after the close. As hold periods extend and exit windows narrow, value creation itself is the job. And PE funds that internalize operating expertise compound advantages across every new acquisition.

In 2026, the edge will come from knowing what to do once you close the deal.

English