@realroseceline I share the latest investment strategy plan on WhatsApp. Free to join ✅

Copy and paste the link and enter it. Reply "777" to WhatsApp: 13074541169

Latest link: wa.me/13074541169/?t…

Thoughts on $ZETA

Lots of you asked me about $ZETA, so I took a quick look at the financials and wanted to share a few early thoughts.

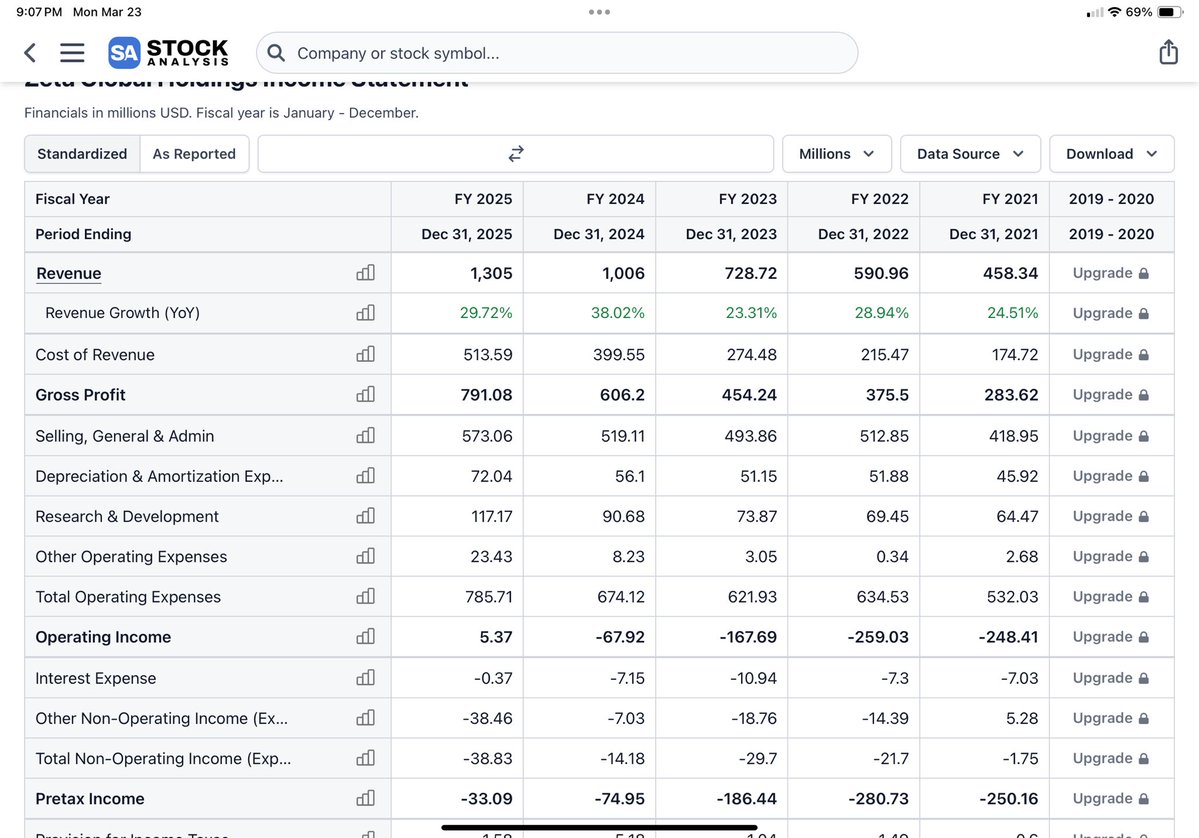

This is actually an interesting one because it looks messy on the surface, but there’s something happening underneath. Sales are strong, revenue grew from $458m in 2021 to $1.3b in 2025, and it has been fairly consistent along the way.

Gross profit was ~$790m on $1.3b of revenue, so roughly 60% margins, which means the core product is not the issue. The problem has been everything below that line on the income statement. SG&A is extremely high at ~$575m or about 45% of revenue, and it has not scaled well, which is why operating leverage has been nonexistent. R&D at ~$120m is fine on its own, but combined with SG&A it overwhelms the business.

The key is that operating income just turned roughly break even in 2025 at ~$5m after years of losses. Operating expenses grew only about ~$100m while revenue jumped by ~$300m, which is the first sign that incremental dollars are starting to fall through. This is not a broken business, it’s a high growth company that historically lacked discipline and is now starting to mature, although non operating losses and still negative pretax income show it is not fully there yet.

The balance sheet is not weak, but it is not strong either. Liquidity is fine with ~$320m in cash and ~$685m in current assets against ~$430m in current liabilities, and debt at ~$200m is manageable so there is no survival risk.

What stands out is how much of the asset base is goodwill and intangibles, roughly ~$776m combined, which is more than half of total assets. That tells you growth has been acquisition driven to some extent, and if those deals do not deliver, you risk impairments and poor capital allocation. Retained earnings are deeply negative at around -$1.06b, meaning shareholders have funded the business historically, but equity is now growing quickly, which aligns with the move toward profitability and improving efficiency.

Current liabilities jumped from ~$200m to ~$430m is something to watch. Some of it may be normal for growth or deferred revenue, but it can also mean working capital pressure.

Then you get to the cash flow statement, which is where things look better than I expected after reviewing the income statement and balance sheet. Operating cash flow is ~$200m on $1.3b of revenue, about 15%, and it has grown consistently from ~$78m to ~$200m over a few years.

But a big part of that comes from stock based compensation ~$178m, which means a large part of the cash flow is dilution. Even so, free cash flow at ~$185m with low capex shows this is an asset light model with strong economics.

What is interesting is the capital allocation. After issuing a large amount of stock in 2024, $ZETA bought back around ~$121m in 2025. That suggests a transition from relying on shareholders to starting to return capital, which is a meaningful change if it continues.

There are still risks. Receivables are a drag on cash, down ~$77m, which means they are waiting longer to get paid. Acquisitions are still ongoing, around ~$90m, which comes back to the goodwill and raises the question of how much growth is truly organic.

So when you put it all together, the income statement says barely profitable, while the cash flow statement says this is already a decent but loosely managed business. The truth is probably somewhere in the middle. This is a company with strong underlying economics that converts revenue into cash, but still masks part of its costs through SBC and depends on acquisitions.

If they keep growing operating cash flow, bring SBC down as a percentage of revenue, and grow organically, $ZETA can become a quality cash generator. If not, it will continue to look good on the surface while largely redistributing value through dilution and acquisitions.

🌹

@KawzInvests I share real-time trading alerts (entry and exit points) on WhatsApp. Joining is free! ✅

➡️ Copy the search link and send the word "TRADE" to WhatsApp: +19737038621

Link: api.whatsapp.com/send?phone=197…

🎥 - Daily live trading

📖 - Trading summaries

☢️ - Personalized strategies

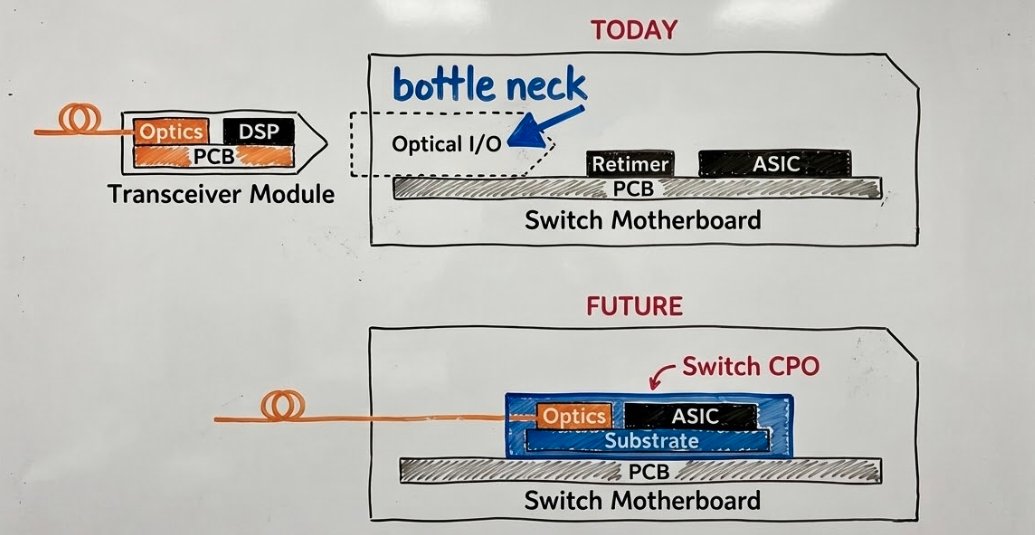

Everyone is arguing over who wins the CPO arms race. $AVGO with Davisson. $NVDA with Spectrum-X. $MRVL with their own play. Meanwhile nobody is talking about the company that supplies the foundries building all of it.

Here's the actual setup.

Today's data centers run on pluggable transceivers. Optics sit outside the chip, signals crawl through copper traces, DSPs burn 30W per interface just compensating for signal loss. At 100K AI servers, optics alone consume 10-20x the power of a traditional data center. The math stops working.

CPO fixes this by integrating optics directly onto the switch ASIC substrate. Signal loss drops from 20dB to 1-2dB. Power consumption falls 3.5x. Reliability jumps Meta ran 15 million device hours on AVGO's Bailly without a single unserviceable failure. This isn't experimental anymore.

But the cycle matters. Pluggables still own 95%+ of the market through 2027. CPO doesn't meaningfully inflect until 2028. You don't abandon transceivers you hold both and rotate.

The real winner-agnostic play? Silicon photonics is the engine of every CPO solution on the market. Silicon photonics runs on SOI wafers. One company supplies those wafers to virtually every major foundry on earth TSMC, Samsung, GlobalFoundries.

Soitec. NVDA wins → Soitec wins. AVGO wins → Soitec wins. Some dark horse startup takes share → Soitec wins.

$24B CPO switch TAM by 2030.

$15B optics TAM on top of that.

$SOITEC

Spent the weekend sorting books for a local school library—helped organize 200+ volumes, and the kids’ excited “thank yous” made every minute worth it! #VolunteerJoy#CommunityLove

"Today’s win: 10 mins of hide-and-seek with my little one—she laughed so hard she snort-laughed, and I got to see the world from her tiny hiding spot. Parenting magic isn’t in big plans—it’s in these messy, giggly seconds. #TinyMomentsBigJoy#ParentChildBond"

"Thrilled to share my recent talk at [Event Name]! Spoke on [Topic]—from core frameworks to real-world wins. Grateful for the engaged crowd u0026 insightful Qu0026A. Thanks to the organizers for the platform! #Training#SkillBuilding#CareerGrowth"

Turn an old glass jar into a chic herb planter! Clean it, add pebbles + potting mix, pop in mint/basil. Perfect for small spaces—no green thumb needed!