cason cantrell

254 posts

I've noticed most business owners have no idea how much their loans really cost.

That gap in understanding can be expensive.

So I built the Loan Amortization Calculator.

If you want it, just like this post + reply “Loan”.

And I’ll DM it to you.

English

If you read one thing today, make it this valuation guide

The 104-paged PDF teaches you everything you should know

Do you want to receive it?

1. Like this post

2. Comment "send" below

3. Get immediate access

English

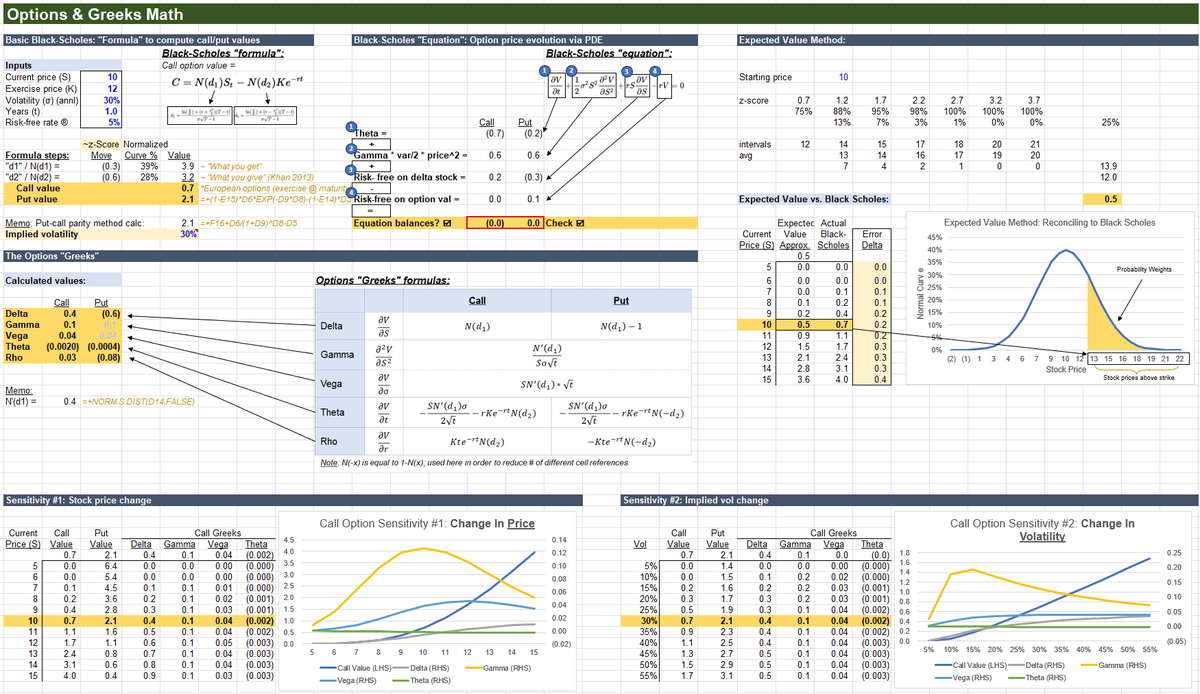

If you don't understand options & greeks, you don't understand markets

Comment if you'd like the excel

5 points:

1) Basics

An option is the right to buy or sell a stock at a pre-specified price.

So if a stock is trading at $10, and you own a call option with an exercise price of $12 and 1 year to expiration -

That clearly is worth something.

But how much?

2) Black-Scholes Equation

The primary answer to that is Black-Scholes.

It describes two competing forces in an option's value:

The negative force is the decay of the option's value over time (its "Theta")

The positive force is the growth in option value as the stock moves (its "convexity" - #2 attached multiplying Gamma by vol & price).

Leaving aside risk free return, the core insight of the Black-Scholes math is this:

The negative impact of time decay at every moment must exactly offset the positive impact of price convexity.

You can watch that change function (PDE) balance precisely in cell N21.

3) Black-Scholes Formula

But the most practical form is the solution to this PDE calculating the exact value of call/put options.

Simplifying a bit, that formula says the following:

What is the probability that this option ends up profitable -

And then multiplies that probability by the difference between the expected value of the stock in that scenario and the exercise price.

This math reconciles exact Black-Scholes to the expected value approximation in cell V29.

4) Greeks

The Greeks show how options move with changes in their inputs:

Delta = option value move per change in the stock price

Gamma = how much delta itself moves with the stock

Vega = option value move per 1% change in volatility

Theta = option value move per day that passes

The other less frequently used Greeks generally capture rates of change of those above (higher order derivatives).

Math & sensitivities attached.

5) Strategies, Extensions, & Limitations

There are as usual two camps of investors:

Those expressing directional views on fundamentals or events; and then those matching, servicing, & trading against the first group.

The second includes market makers, vol surface traders, carry & dispersion traders, and others.

But options also serve as a metaphor for almost any payout structure in finance:

Credit investors and merger arbs sell puts

VC and biotech buy calls

Distressed varies by cap table position

Options describe a wide range of outcomes in ways other vehicles can't.

And in equities, despite other methods like binomial trees, and Black-Scholes assumptions that are often wrong -

The essential framework

Is identifying how asset volatility interacts with finite time and changing market conditions.

There is further depth in every direction here

But as always, the key is a firm grasp of the principles,

Clarity around the math,

And intellectual honesty about the limitations.

That's all for now

Comment if you'd like the excel

English

cason cantrell retweetledi

Compounding Quality's first e-book is ready!

It will be published on Amazon soon (price: $30).

Today I am giving it away for free.

To receive it:

1️⃣ Follow us (so I can DM you)

2️⃣ Retweet this tweet

3️⃣ Reply 'Book' below

English

Men's testosterone levels are in crisis.

Luckily, I've created the ultimate testosterone-boosting guide.

I usually only give this info to my paid clients...

But for 24 hours, it's yours for FREE.

Like & Comment "💪" and I'll send it to you.

*Must be following

English

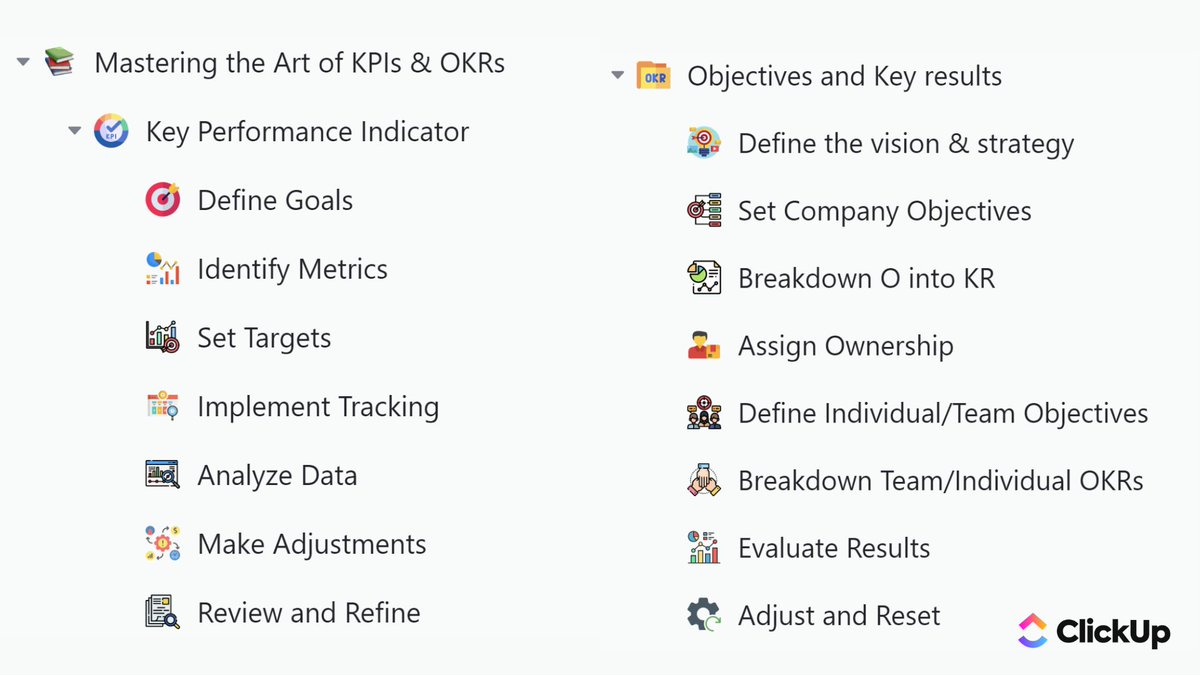

KPIs and OKRs are confusing

But it is used in EVERY company, still, 42% don’t know the difference

So here's the guide for you to Master the Art of KPIs & OKRs

And for 24 hours, it's yours for FREE

Like + comment "want” and I'll send it

(Must be following)

English

cason cantrell retweetledi

I Built a "Warren Buffett Blueprint"

It shows you step-by-step how to find high quality stocks, at a fair price.

Using Buffett's core investing rules.

Get it FREE, just:

1️⃣ Follow us (so we can DM you)

2️⃣ Retweet & Like this tweet

3️⃣ Reply 'Buffett' below

English

Big announcement! We are sharing our first investing course!

In this course you'll learn how to analyze Financial Statements like a professional.

It's free for the first 1,000 people only.

To receive it:

1️⃣ Follow us

2️⃣ Retweet this tweet

3️⃣ Reply 'free course' below

English

Warren Buffett once said Accounting was the "language of business."

So I made it my mission to help.

I created a FREE guide that breaks down:

• Financial Statements basics

• managing cash flow

• how to pick KPIs

• and more!

Like + comment "PNL" & I'll DM it to you.

English

Our systems are currently experiencing downtime. We’re determined to restore full functionality as soon as possible. We’ll be sharing updates here and on status.robinhood.com.

English

@AskRobinhood Robin Hood toy really do need better consumer service you can’t even call to talk to a real person. But 9:30 is coming up quick and I would really hope I could get at least a real understanding of this problem before I lose money again because of you.

English

@AskRobinhood You reply faster when I actually tweet at you can you please look into this problem. I am totally for real or give me a real answer. I have photo proof of my account in my DM.

English

Robinhood is now fully restored. We know this has been frustrating and we will work diligently to provide the level of service you deserve.

English