Darius

370 posts

This week I'm sitting down with @Jkylebass on the podcast.

Kyle is the CIO of Hayman Capital Mgmt - an investment manager of private funds focused on global event-driven opportunities.

What would you like to know?

English

@flynn_bob Hey Bob, I might have a deal for you. Let me know if the below might interest you:

- CA strip center

- 40% LTV ($2mm needed)

- one of the tenants sells medical marijuana so difficult to get traditional financing

Please DM me if interested!

English

Just starting (finally)..

James E. Thorne@DrJStrategy

It’s called Deflation. No one should be surprised!!!

English

@moseskagan Thank you for pointing this out.

Have owned multi tenant industrial since 05 in Orange County and NorCal.

The GFC took no prisoners and many of our tenants went out of business or couldn’t pay rent.

English

As we get deeper into looking at assets with non-credit tenant bases (mainly, multi-tenant industrial) in SoCal, three things are becoming clear:

1. Even though the tenants are superficially in different businesses, the reality is likely that they're ~all cyclical businesses, so you're vulnerable to large increases in vacancy / big rent drops

2. Bc of the above, you want to keep large reserve and/or limit or eschew leverage, so as to avoid becoming a forced seller at precisely the moment you would not want to be

3. The pricing for these assets reflects the fact that we have not had a real down-cycle in a very long time

English

I am going to my wife's Office Christmas Party

Looking forward to it

English

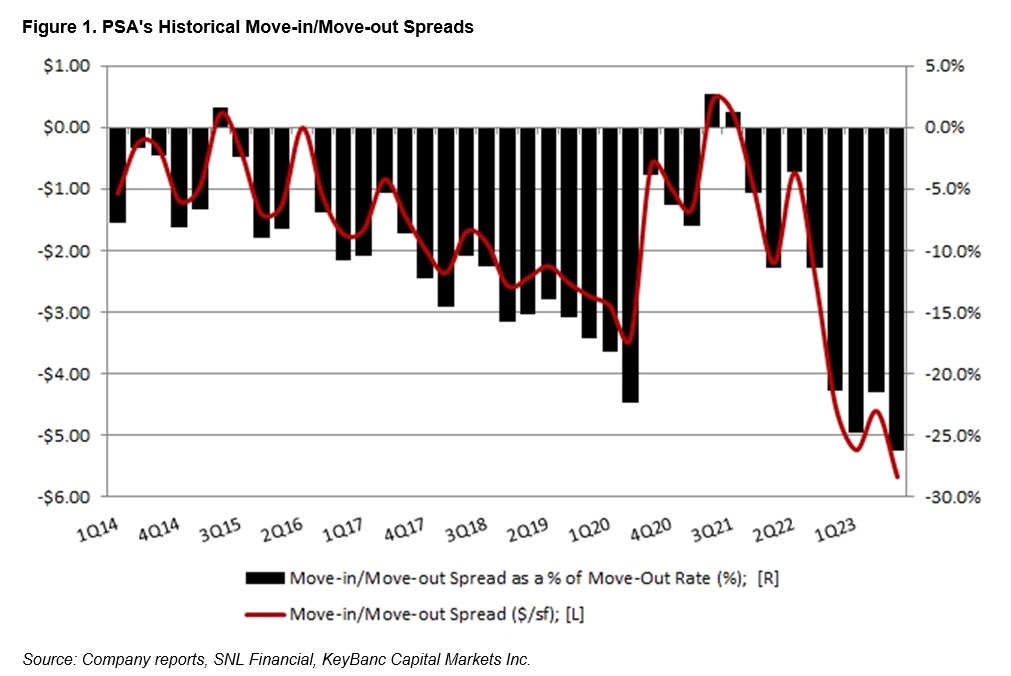

@ZeroBasis Yes

It’s the spread between the price a tenant is paying that moves out vs moves in.

Right now it’s 26% for PSA and I’m sure it’s higher for EXR.

English

@chewwwna Why do earnings keep going up?

finance.yahoo.com/news/public-st…

English

@realEstateTrent I banker learned this years ago

Practical way of concealing your laptop if you are leaving the office before 10pm on a weekday 💰

English

Have my laptop, and didn’t want to carry it around New York City.

I was today years old when I learned it fits inside a FedEx envelope.

Perfectly.

English

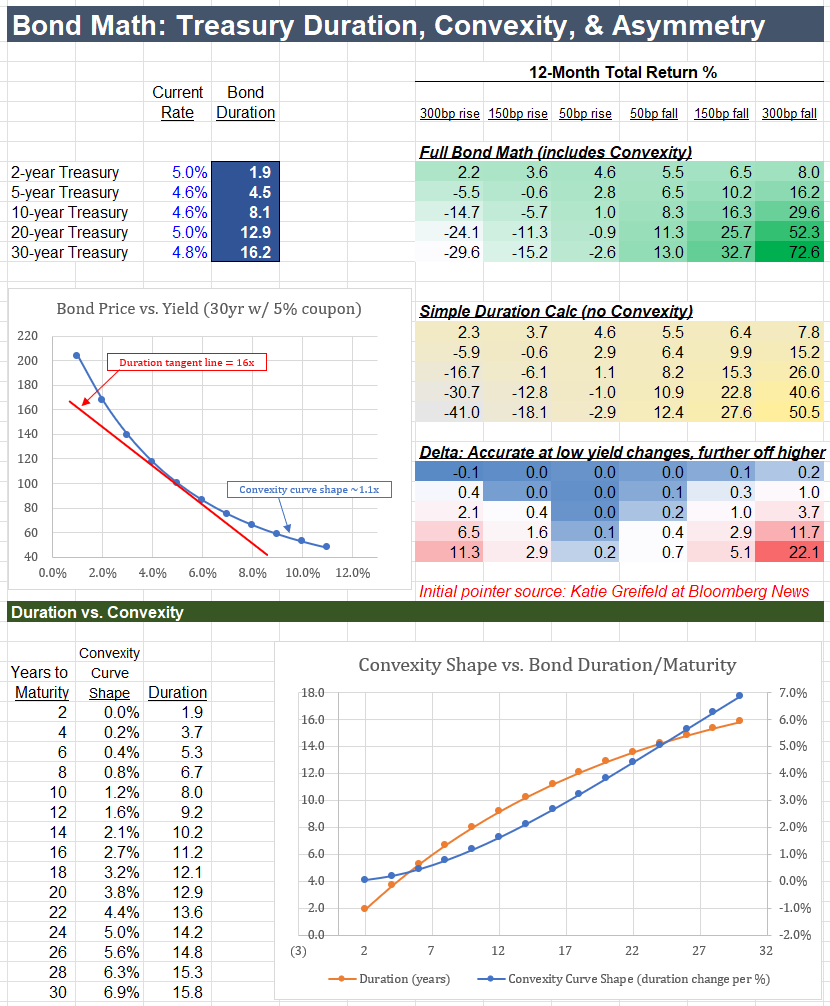

Bond math is now key to today's financial markets

Let know if you'd like the sheet.

The table on the right reflects a powerful new dynamic:

If rates fall 50bps, 20yr Treasuries earn 11.3% over the next year.

But if rates rise by 50bps, they lose just 0.9% -- an 11:1 up/down ratio.

The 5 year-average 20yr yield is just 2.5%, compared to today's 5%+ yield.

At that lower history, the same 50bps up/down math sat at just 2:1, much less skewed.

So in the context of recession fears, commodity shock, and mixed econ data, that return skew is drawing cross-asset investors -- hedge funds & asset managers normally less involved in Treasuries.

This competition for capital is one of many mechanisms by which higher rates challenge equity returns.

Several items are pushing long rates up: the rise of JGB long rates, US deficits, persistent inflation, the dollar, and others.

But implicit in the new investor framing of long-bond risk/reward is also the changing impact of the duration math, and the role of convexity across the curve.

Which is worth understanding.

Duration describes the average time it takes to receive any set of cash flows.

Whereas a bond's maturity is simply the date principal is repaid.

As a result, maturity and duration differ if there is a coupon: the larger the coupon relative to the principal (& price), the shorter the relative duration.

So, if a 10yr bond at par has no coupon, its duration is 10 years.

If the same bond has a 10% coupon, its duration is 6.5 years, since much of the total cash investors get comes in every year via coupon.

But the duration has another very useful property:

It also exactly equals the bond price change associated with a 1% change in its yield.

Thus, for the same 6.5 year duration bond, if the yield falls to 9%, the price rises from 100 to exactly 106.5.

The next question is how duration changes:

Is the 6.5 duration constant as yields move from 10% to 9% to 8%?

No -- because the weighted average life has changed at each increment.

This change is the bond's "convexity."

And it is the driver of why a 3% rate fall means a gain of 70%+ while a 3% rise means a loss of just 30%.

You can see that difference in the first chart below:

Red is the duration of a 5% coupon / 5% yield 30-year bond: 16 years.

Blue is the actual bond price across yields.

The difference between the two lines is the effect of convexity:

The price change slows as yields rise

And rises steeply as yields fall.

Next shows the curve of convexity itself shifting across maturities.

Directional views on Treasuries here are a function of growth path, fed policy, and a host of other factors.

Sometimes you make that bet.

But other times, or if you're restricted to markets competing for scarce capital,

Knowing the asymmetries & reaction functions across markets

Improves your ability to anticipate and act

In your area of focus.

That's all for now.

Let know if you'd like the math.

English

@STLChrisH @fortworthchris @FortCapitalLP This is really just equity with capped upside (equity risk but capped upside)

Need a bigger slug to get downside protection

In a BK scenario this won’t be the fulcrum and will get 🍩

(Note: Chris seems like a very talented operator, just a comment on the capital stack)

English

I have not met @fortworthchris or anyone at @FortCapitalLP. But I’ve put $100,000 into nearly every deal of theirs since 2022. Roughly $1,500,000 total.

I guess I like his pod.. but what I like most: their “Class A Mezz” offering.

The latest offering was at an 11% yield. First-in-line for cash flows from both operations and from any refinancing / sale proceeds.

Risk-return characteristics are attractive. Typical deal structure includes 65% senior bank debt, with another 5% Mezz (where I like to play) and rounded out with 30% equity.

If the bank is taking SOFR plus 200bps on debt up to 65% LTV, that next 5% sliver is taking on small incremental risk beyond the bank’s dollars contributed at the 65th percentile, but earning a return roughly 50% greater than the bank’s senior secured debt (7% vs 11%).

Another way to look at it: I have a 30% equity “buffer” before my capital is at risk and receive an 11% return. The bank has a 35% buffer before their capital is at risk and receives a 7% return. Seems like a good trade.

Not a bad risk adjusted return in today's market. Now don’t go filling up FCs mezz offerings before I can subscribe…

English

The recent oil price spike may continue a bit longer given the major 2H23 draws & speculators rushing back into long futures exposure right before a nasty recession, ala mid 2008…

English

@ADeermount Can’t believe more people aren’t talking about the impending maturity wall in storage

English

Hearing rumors of a tsunami of lease maturities hitting in the self storage industry on Thursday.

Newport Beach, CA 🇺🇸 English

Time to back up the truck and buy duration #zroz

Long term deflationary FORCES:

- US DEBT (US government/economy cannot survive in this rate environment)

- DEMOGRAPHICS (aging population / low growth)

- TECHNOLOGY (inherently deflationary, AI will only accelerate the trend)

English

@awealthofcs Look at the 04-06 hiking cycle, takes a long time for the economy to feel rate increases

English

The Fed went on one of the most aggressive rate-hiking cycles in history

It's been 18 months yet the unemployment rate hasn't budged, GDP growth is accelerating & housing prices didn't crash

Can we just admit that no one really understands how the US economy works?

English