zet

22 posts

Yup, called it. U.S. investors ate the dip fast.

Feels like the conviction is stronger overseas while the home market is still hesitant.

Once more people actually understand what $SIVE is building in photonics/AI infra, sentiment could shift quickly.

High conviction here, but execution is everything.

DYOR.

English

I see a lot of people scared about $SIVE unprofitability.

But what about $AXTI? What about $AAOI?

$SNDK went from deeply unprofitable to highly profitable because the AI/memory cycle changed everything.

Sometimes it’s less about current profitability and more about revenue growth + positioning before the demand wave fully arrives.

English

@ciainvestor Bro i did my own research and this had been clear for weeks. It's because of the NASDAQ listing.

English

New position TLDR:

$LASE at ~$27M MC.

Industrial + defense laser company scaling aggressively after posting 144% YoY revenue growth.

Recently raised ~$4M from warrant exercises while continuing expansion into defense, anti-drone, and industrial laser systems.

Thesis is the company is trying to evolve from a small industrial laser business into a higher growth defense-tech player.

The interesting part is management keeps emphasizing military applications, counter-drone systems, aerospace, maritime, and government contracts.

Feels like they’re positioning themselves as a small-cap defense laser growth story before major adoption happens.

Main risk is obvious though.

Still deeply unprofitable and financing growth through dilution/warrants, so execution matters a lot here.

If they land meaningful defense contracts and keep scaling revenue, valuation disconnect could get interesting.

Basically a speculative small-cap laser/defense growth play with high upside if execution works.

Of course DYOR

English

@AtlasShrug1 Holy shit this was made by ai, your ai is delayed brother

English

$SIVE $SIVEF

Something seems very wrong here…I’ll be staying far, far away from this even on a pullback bc what the following release tells me is that the institutional clearing price for just a small amount of shares was 14.5 Skr, about 30-35% of where the stock is currently trading on persistent retail hype. To me this is even worse than $IQE having to raise strategic money at 19.8p, at least they got $MTSI involved on the board, but both of these in combination should give folks great pause about how much they are paying for all of these microcap photonics related names that have gone parabolic in the first half of the year. There is a clear message being sent here imo:

The Extraordinary General Meeting in Sivers Semiconductors AB (publ) (the "Company") has been held on 11 May 2026 and in particular the following decisions were resolved.

KISTA, Sweden, May 11, 2026 /PRNewswire/ -- Resolution to approve the Board of Directors' resolution on a directed new issue of shares

The Extraordinary General Meeting resolved to approve the Board of Directors' resolution of 15 April 2026 to increase the Company's share capital by SEK 4,310,000 through a directed share issue of 8,620,000 ordinary shares, at a subscription price of SEK 14.5 per share. With deviation from the shareholders' preferential rights, the new ordinary shares were subscribed for by a limited number of Swedish and international institutional and other qualified investors, including both new and existing shareholders: DNB Disruptive Opportunities, DNB Nordic Small Cap, Storebrand Sverigefond, Alcur Fonder, Atlant Fonder, Cicero Fonder, Hudson Bay Capital Management and Waterside AM. The subscription price was determined by the Board of Directors based on arm's length negotiations with the investors.

English

Feels like the same cycle every week with $SIVE.

New local bearish article drops:

“CPO isn’t new”

“$LITE and $COHR will dominate”

“Nasdaq listing dilution is bad”

“Delayed report looks suspicious”

“They’re too small to scale with $JBL”

Stock sells off, local retail panics, then more sophisticated investors quietly absorb the float.

Meanwhile the actual thesis hasn’t changed: AI networking scale-up keeps accelerating, CPO adoption is coming, and specialized optical suppliers with hyperscaler exposure remain extremely scarce.

Makes total sense why they’re pursuing Nasdaq instead of staying confined to local markets.

English

Still funny watching Swedish media constantly doubt $SIVE.

One article literally visited an empty administrative office unannounced and treated it like some exposé because the CEO was in Silicon Valley and engineering work is heavily US-based around hyperscaler + CHIPS Act development.

Then they say:

“Lots of companies make these lasers.”

Yeah — companies like $LITE and $COHR… multi-billion-dollar optics leaders.

Same people also dismissed CPO as “nothing new” while the TAM is projected to explode this decade.

Feels like many still don’t understand hyperscaler supply chains, forward growth curves, or how valuable specialized optical IP can become once AI networking scales.

But thankfully USA takes the opportunity and buys the dip.

English

Why I like $LPK / $LPKK:

LPKF looks like a key bottleneck supplier for glass core substrates via LIDE technology. Over 80% of major players reportedly selected its equipment for validation. As AI infrastructure scales with names like $SIVE, $SNDK, and $LITE, glass core packaging and advanced interconnect demand could accelerate significantly from here.

English

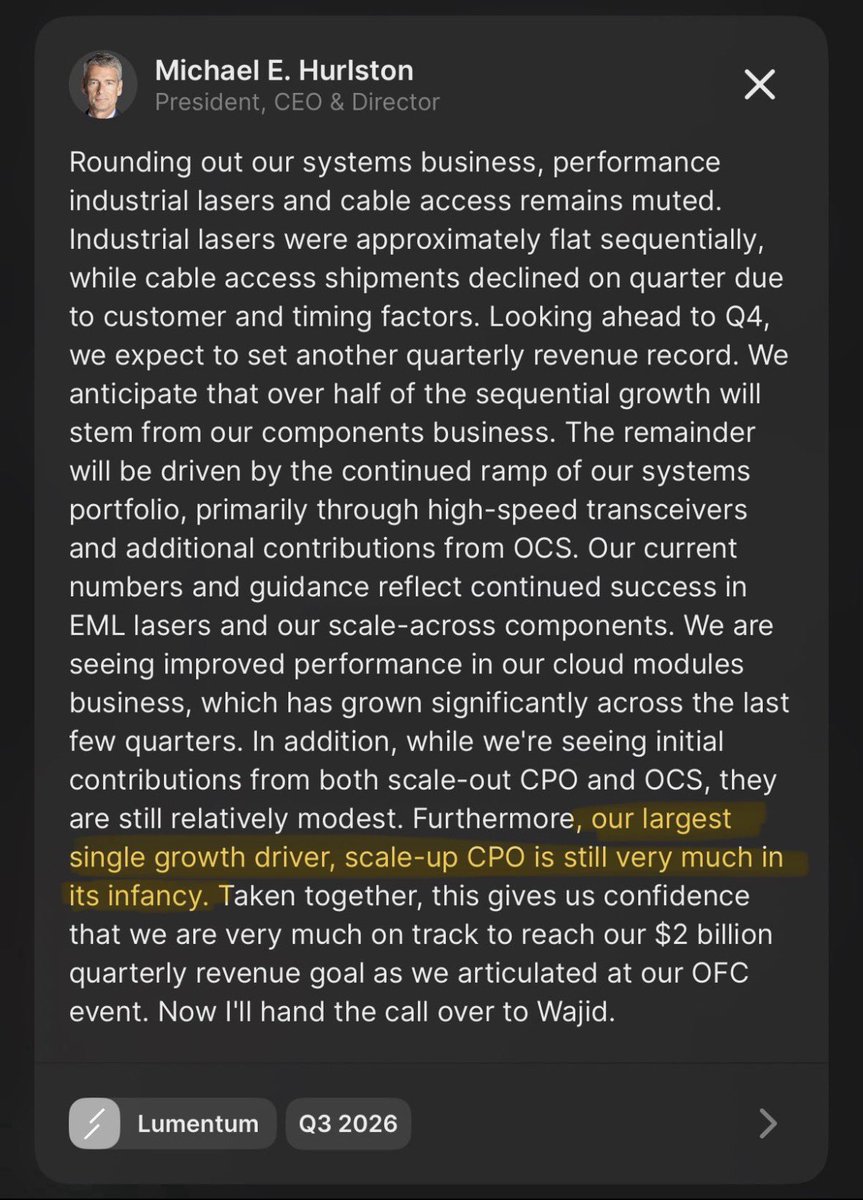

Lumentum just confirmed what the market is starting to realize: scale up CPO is still in its infancy, yet already their biggest growth driver. That’s why names like $SIVE are so bullish. AI scaling needs optical interconnects to solve power, latency, and bandwidth bottlenecks.

English

It's funny how $SIVE investors are panic selling because of a dump.

But 2 days ago sive went up 46%, it's really a problem if you panic in this situation.

Lesson: if a stock can go 30-40% a day, it also can drop 30-40% a day. So don't panic and buy the dip.

But always DYOR.

English