Circumsedere

937 posts

Circumsedere

@circumsedere101

Knowledge Sharing

Toronto Katılım Şubat 2012

171 Takip Edilen151 Takipçiler

@fundmyfund Sold around $6. Personally hoping for a re test lower to get back in

English

Old friend $NRGV is moving

It looked really nice towards end of April but then did this nasty action in the orange box after... so was off my menu after that

Everyone has their own style

Fund.Drone.DefenseTech.Photonics $LPTH $UMAC 🐋@fundmyfund

$NRGV beast mode engaged Just droppin' alpha left and right. "this is insane!" 😂 Forgettaboutit!!! 🇨🇭

English

@fundmyfund Think it still has upside? Been a huge runner

English

T minus ~30 minutes until $CBRS goes live at $185/share on Nasdaq.

Quick recap on how things progressed:

> $115-$125 range filed May 4

> Bumped to $150-$160 on May 11

> Priced at $185 the night of May 13

> Trading at nearly 2x on Perps

$56B+ valuation. $5.55B raised. Officially one of the largest US IPOs ever and the biggest tech IPO of the year.

> $25B+ backlog vs $56B valuation - still a strong backlog to MC ratio for an AI infrastructure company at IPO

> $510M 2025 revenue with 47% net margin (76% YoY growth)

> OpenAI 750MW multi-year deal, $AMZN AWS deal already signed, $META as a customer

> 20x oversubscribed at the original range, IPO priced well above the revised range

> Customer concentration risk (G42 was 24% of revenue last year)

When the largest AI hardware IPO of the year prices 48% above its original range with $5.55B raised… the market is telling us where we should stack our investments.

Validates the entire AI infrastructure thesis.

Validates the “alternative to $NVDA” thesis.

Most importantly, this reaffirms institutional capital is still flooding into this supercycle at scale.

And no, you don't need to invest in $CBRS directly...

We've pointed out many proxy plays. And every single asymmetric opportunity we've highlighted recently will benefit from capital & demand flowing into the ecosystem.

Wayne Liang@wliang

$CBRS (Cerebras) IPOs on Thursday at ~$26B, raising up to $3.5B. Largest IPO of the year so far (in the US). $CBRS builds wafer-scale AI chips, an alternative architecture to GPU based approaches. Customer base includes OpenAI ($20B deal), $AMZN, and $META. Now this is pretty interesting... $25B in contracted backlog vs ~$26B IPO. That's nearly a 1:1 backlog to market cap... much better than $CRWV's ratio at the time. Or $10B of demand for a $3.5B raise... Validates the entire AI chip and inference market once again. More money flowing into competitive architectures means more confidence in the thesis. New capital flowing into the same supercycle... and if you've been following my posts, you can guess what benefits directly from the $CBRS IPO.

English

A lot of dinosaur tech stocks are climbing out of massive bases.

Many of them date back to the dot-com bubble.

Here's what can happen when stocks break out of gigantic bases like this...

$TTMI +550% in a little over a year after climbing out of its two-decade base

$CSCO $INTC $AMKR 👀

English

@LeaderInvests Crazy discount compared to companies like NBIS. $IREN should be almost a 2x from here?

English

Big money will always position themselves before the moves happen. Same will be for $IREN.

Most just don't have the patience to wait for days / weeks / months.

Weekly breakout is confirmed. $IREN got upsized $2.6B Convertible Notes showing HIGH demand.

Let time do it's thing now.

ChinoAleman@chinoalemano

The point isn't how many $IREN shares BlackRock bought last quarter. Still, it's impressive they have $250,000,000 invested in IREN. The real question is how many shares they bought this quarter, crazy dark pool volume.

English

@fundmyfund Been watching this the whole way down from $100….. when would you step in? Im thinking of finally getting back in this morning

English

$LITE blue skies.... probably nothing.

Elite Swing Traders@1ChartMaster

$LITE Another 8 week pivot. Probably nothing

English

Episodic pivot innit? $GLW

Connor Bates@ConnorJBates_

$GLW Tightening up on the right side of this base. Investor day on Wednesday.

English

What non-memory/photonics semi are you most bullish on?

English

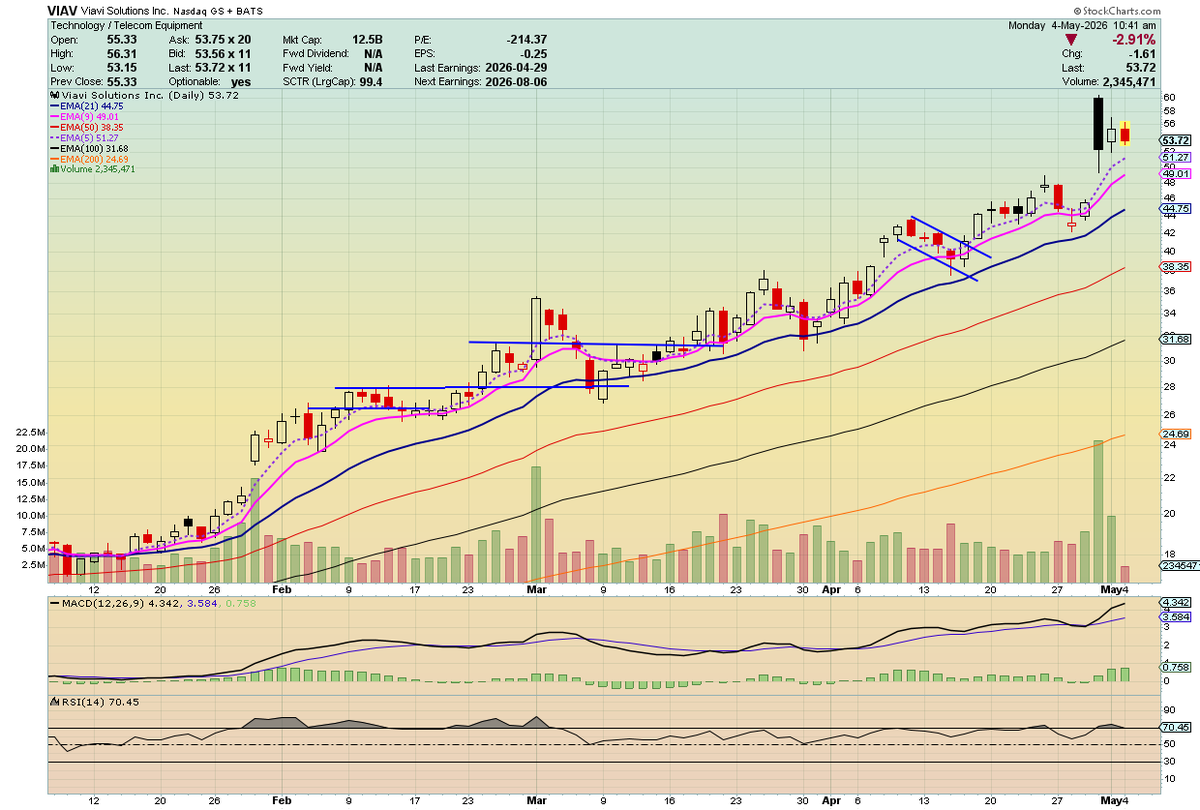

$VIAV setting up nicely for entry post earnings

Will be interested in this mid to later this week if it can continue to build this little range

Fund.Drone.DefenseTech.Photonics $LPTH $UMAC 🐋@fundmyfund

I like what $VIAV is doing I hope it can sit and range for about a week, then middle to end of next week it can be a candidate

English

It's nice to see "Rambo" making the rounds. Finding an interview with the prior CEO was like finding the Loch Ness monster. $KRMN

KARMAN Space & Defense@karman_spacedef

Jon Rambeau, CEO of Karman Space & Defense, says strong demand in defense and space is driving growth, with capacity, scale, and supply chain positioning playing a key role as the company supports major programs like Artemis. cnbc.com/video/2026/04/… #Karman #KRMN #KSD #KarmanSD #ImpossibleEndsHere #SpeedAgilityScale #space #defense

English

@fundmyfund Good opp to get in if you missed the move higher?

English

$RMBS -16%ish in pre

Market is going to require home runs from these names after their parabolic runs

Falling to 21 ema, marked by orange box. Shows how extended these were when a bad day yesterday and a bad morning today only take it back to that level.

Fund.Drone.DefenseTech.Photonics $LPTH $UMAC 🐋@fundmyfund

Initial reaction is -8%ish $RMBS That's on top of the -11%ish during the day. Will see after the call. Could be up 20% tomm morning or down the same. Casino bets. With these run ups going into earnings season, companies in the semi space or adjacent (even memory storage whatever) going to need home runs

English

@fundmyfund @ljh_100 Shocking whats going on with $KRMN, thankfully stayed away since chart looks horrible. Monster in the making though

English

@ljh_100 $KRMN $KTOS $AVAV , all of their primes, and their suppliers

English

@AaronRentfrew Thinking the same thing! Easy stop is a break of the previous ATH?

English

@eliant_capital Happened to see this today. Looks like $TRT finally getting some real attention. With $AEHR exploding, this could be a catch up play on steroids

English

Yep, I can confirm , he mentioned it to me on Friday after hours 🐐 $TRT

Stock Talk@stocktalkweekly

$TRT This didn’t make it on Twitter, but I spent the weekend discussing this play w/ friends as a comparison to peer $AEHR $AEHR: +1600% past 1-year, $16.6M 2021 rev, negative EBITDA, $660M mkt cap vs. $TRT: +25% past 1-year, $33M in 2021 rev, POSITIVE EBITDA, $19M mkt cap

English