Confluence.VC

53 posts

Confluence.VC

@confluence_vc_

"The VC operating playbook"

MIA Katılım Ocak 2024

1 Takip Edilen39 Takipçiler

what my Gmail sees after watching me be reactive to email requests for 16 hours every day

English

Confluence.VC retweetledi

thoughts about starting a business after five years of running one:

- 99% of the skills you learn as a business owner cannot be learned through reading. Incorporating your business, building an offer, improving your product, selling through persuasion, finding profitable sales channels, handling customer support, recruiting affiliates, setting up payroll, handling DMARC records for a new domain, scaling cold outreach without burning your original domain, improving site speed, creating backlinks, staying compliant, building a tracking system for your team, etc. Blog posts will not save you for most of the situations you’re thrown into - you have to solve them on your own and learn through experience.

- Running a business will expose you to “reality” more than just about anything else you can do. I think I originally got this from @callicrates_ . When you’re an employee, you’re shielded from reality. Every problem as a business owner is your problem. Most problems at your job can get passed off to become somebody else's problem.

- If you want even more of a reality check, bootstrap a business. No outside funding, started with your own savings, reputational risk, true skin in the game, lights only stay on if you figure out how to operate profitably.

- Drowning yourself in delusion is better than being “realistic”. Delusional optimism will force you to do things that a rational person wouldn’t. A “rational” person would tell you to never quit a job, never abandon the safe path, and definitely never take the risk of starting a business. Shoutout to @TheRealEstateG6 for this.

- “Founder” usually means you have 5+ jobs. You’re in charge of building the product, getting feedback for product improvement, website maintenance, the entire marketing department (socials, newsletter, ads), customer support, and a million other jobs. If you want specialized work, don’t start your own business.

There is always more that can be done, but if you don’t create some sort of schedule, you will go insane. Time freedom is arguably the best part of entrepreneurship, but if you don’t put some sort of guardrails on how you spend your time within your business, you create a prison for yourself.

- Five non-work things have helped my business more than almost anything else: lifting weights, consistently getting sun, walking, playing sports, and having other founder friends. Without lifting, my spirit and mindset changes for the worse. Without sun, my energy drops. Without walking, I am not creative. Without sports, my competition gets worse (plus the right sports create the easiest networking opps you’ll ever have). And without founder friends, I would be left to solve all my work problems by myself.

- When you own the asset, your work output is directly tied to making money. This creates a subconscious feeling that you should be working all of the time, and you start to feel that you are leaving money on the table every second you are complacent. Your previous definition of “chilling” becomes a foreign feeling.

- You can either be hardworking, or you can be smart; you cannot be both. You’ll never be able to outwork somebody with leverage. Build leverage through code, media, capital, or labor so that you can have others work for you.

- I have not found an activity that creates more asymmetric upside for a business than building an audience. This newsletter has introduced me to founders I would otherwise have no chance at meeting, co-investors who I can do business with for decades, LPs who have committed to deals, and talented individuals who can be hired in future roles. The opportunity costs of building in silence are massive, and if you want to attract luck, build an audience.

- At a very high-level, scaling a business as a leader comes down to two things: attracting and hiring new people and attracting and raising money. Being charismatic makes both of these much easier.

- Reality is largely negotiable. You’re not getting enough traffic? Cool - start spending more time, effort, and resources towards ads? Not getting enough conversions to customers? Great - more goes towards optimizing your landing page, segmentation, and funnels. Frustrated with customers? Get better customers. There’s always a way out of your current spot.

- You’ll never have right and wrong answers. As an employee, you're taught to get feedback from your boss and take that feedback as the “right” answer. That’s not how business works, and as a business owner you have to become comfortable making decisions with ~70% of information.

- Decision-making velocity will compound the quality of your business (and life). Velocity creates momentum, and velocity hates indecisiveness. If it takes you days to make simple decisions, you are getting lapped by your competition.

- You have to become a ridiculously good problem solver. You can’t turn to your boss, Google, ChatGPT, or the internet to solve your new niche problems. This separates out a lot of people when they realize how little they were taught to think for themselves as an employee. Academia has created a society of learned helplessness that will kill you as a business owner.

- Avoiding stupidity is easier than being brilliant. Rule #1 for any business: don’t blow yourself up.

- The more complicated you speak, the less people will listen to you. True geniuses can explain complex things to a child.

- Ignoring distribution is the dumbest thing you can do as a business owner. The best product rarely wins. This was counterintuitive to me for the longest time, but look at the adoption chart of Slack vs. Teams if you need a reminder. If you can’t consistently reach new customers profitably, your business is toast.

- The internet rewards the unique and ignores the indistinguishable. You’re not only killing your soul when you think, talk, and act like everybody else; you’re killing your business.

- Your ability to productize yourself is directly proportional to how much money you can make. You can still build a business without many employees / contractors, but if you are the bottleneck on every process in your business, your ability to scale is capped.

- The tighter you hold your money, the less of it you attract. Get comfortable spending to the point where you are constantly uncomfortable.

- It takes bad judgement to create good judgement. So you might as well try a lot of things early. As long as the early mistakes aren’t catastrophic, you’ll come out better.

- Long time horizons improve behavior. Short time horizons worsen your judgement. "There's billions of dollars waiting around for whoever can wait the longest." @WillManidis

- Every day is a constant reminder of how little you know. Even when you start getting progress, you always feel like an idiot.

- Any “luck” you get in business is the macro result of thousands of micro actions. People don’t get lucky. Luck eventually finds them.

- Your biggest regret will be not starting sooner. You build your life up over a long period of time. Since decisions compound, the earlier you get started the better off you will be.

English

when they're mad at you for being terminally online and referencing memes that nobody understands, but you're just a chill guy with a dopamine addiction

English

five mins into a founder call trying to explain all of the ways I add value

English

if your GP dresses like this, it might be time to dust off the resume

English

this man is working drive thru @ McDonald's and you're too busy to respond to a couple of emails today?

English

Confluence.VC retweetledi

Confluence.VC retweetledi

I’ve worked every role imaginable in venture capital over the past seven years.

I’ve worked as an LP, I’ve run a syndicate, I built a private community for VCs, and I cut my teeth as a junior VC working for two different funds.

Here are 93 things that nobody told me about VC:

1. It used to be a requirement for VCs to have company-building experience, but that has gone away as more funds have popped up. The advice you get from most VCs today is based on something they read and not personal anecdotes. Do not take this advice as gospel.

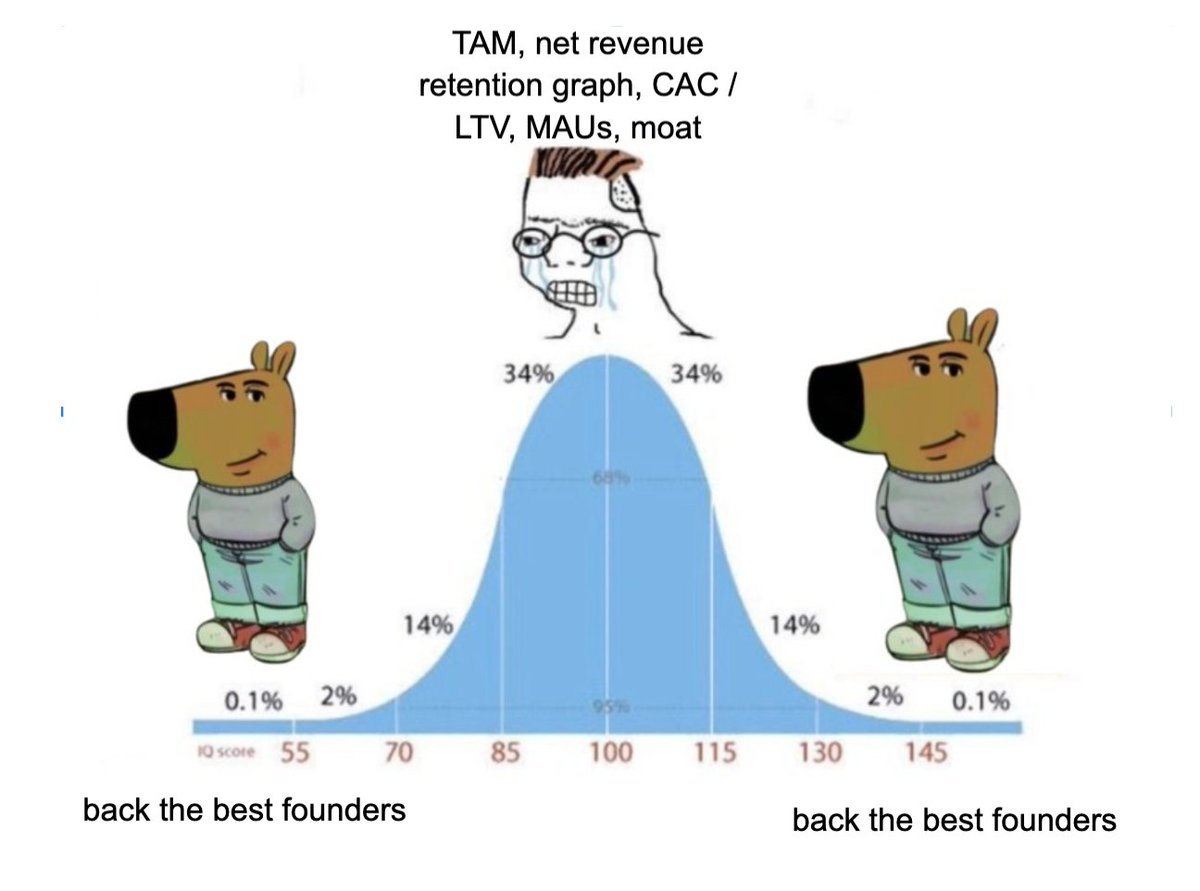

2. The best founders spend the least time fundraising. If you make your diligence process a burden on the founder, you’ll have to settle for bottom-tier deals.

3. VC Twitter is the worst place on the internet. Avoid unless you want to lose brain cells.

4. You'll constantly hear the line "Where can I be helpful?" Most people cannot offer you help. Accept this, and move on.

5. Everybody in VC claims to want to be your friend. It's up to you to figure out a) who you want to work with and b) who you can actually do business with.

6. It is way easier to 3x your money at a $10mm fund than it is at a $100mm fund (both as an LP and a GP).

7. The VC tech stack is ironically horrible for nearly every fund. Spreadsheets and email are the standard.

8. The larger the fund, the more focused your job is on sourcing. The smaller the fund, the more you'll have to be a jack-of-all-trades.

9. Most junior VCs are glorified business development reps.

10. Proprietary deal flow is a myth for 99% of funds. The best deals get shopped around. How do you see it before everybody else?

11. You can raise a fund on influence, but it is very hard to scale one on clout alone (Ashton Kusher + The Chainsmokers are a few of the only ones that have proven this wrong).

12. “Partner track” roles are not as popular as you’re led to believe. Most analyst / associate roles are two-year positions, then you're expected to find something else after that (preferably joining a portfolio company or starting your own company).

13. If you earn carry at your fund, consider yourself lucky. 90% of junior VCs get no upside for their work. (Source: confluence.vc/vc-salary-data/)

14. If you want to be rich, working as an employee in VC is one of the worst fields to do that.

15. If you're a junior VC and want to work directly with founders, you’re better off joining an actual startup. Your involvement with the founding team will peak during the diligence process, and then it will wane off from there.

16. Selling products or services to VCs is incredibly difficult. These people are some of the most selective people in the world, and they say "no" for a living.

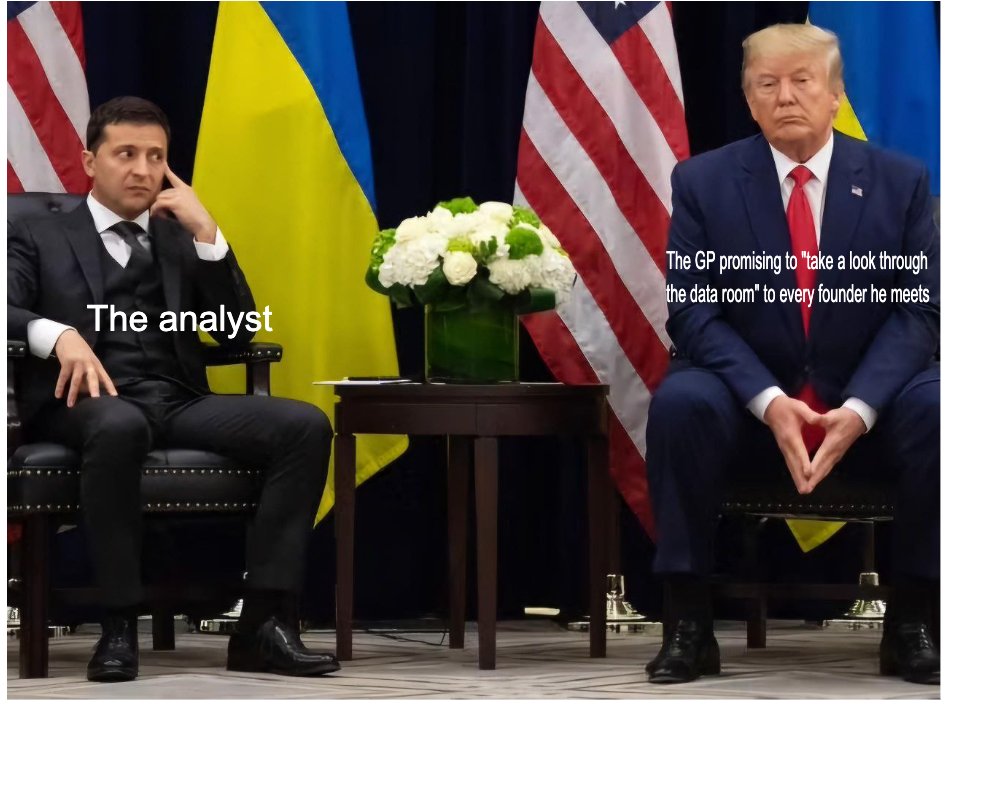

17. Venture capital rewards being solely focused on your job for long periods of time. If you have any plans of being multi-faceted and not obsessed with your work, there are better careers for you.

18. Spray-and-pray seed funds do more harm than good to companies that require large amounts of capital. If a fund isn’t able to follow on into your next round of funding, it sends a bad signal to other investors.

19. Most VCs are extremely lonely in their day-to-day. Small teams and saying “no” all day will do this to you.

20. Venture capital is an apprenticeship game. Because of this, you’ll be expected to be in the office to get facetime. It’s tough to find roles that are open to remote work.

21. You don’t have to focus on content all of the time (I’d argue that many new funds over-index on the importance of having a digital presence). The argument is that more content makes you more discoverable, but that really only applies to a handful of funds (most notably First Round + a16z). Benchmark is one of the best funds to ever exist. Look up their website.

22. The best companies want to work with the best brands of investors. If you aren’t a tier one or tier two fund, you have to figure out another way to get meetings (this typically means more work needs to be done before the call).

23. There are very few contrarians left in VC because almost everybody is scared to say what they actually think.

24. Seed and pre-seed investing is all based on narrative. The easiest way to raise money is to tell a story that feeds into that narrative (web3 in 2021, creator economy in 2020, fintech / embedded finance in 2018 / 2019).

25. The biggest asset an investor has is his / her network, but 90% will scoff at the chance to 10x their network overnight.

If that's not you, check us out: confluence.vc.

26. The best deals come from people you actually take the time to get to know and become friends with. If you view every interaction as transactional ("you send deals if I send deals"), why do you think anybody would send their best deals to you?

27. Relying only on sourcing software will have you competing for the same deals against everybody else. A Pitchbook subscription will not save you.

28. Most inbound deal flow is worth ignoring, but if somebody is smart enough to break the mold and capture your attention in email, meet with them.

29. If you find yourself putting a higher emphasis on financial projections or fund returns for seed investments, you’re thinking about it the wrong way.

30. Serious investors back the best companies. They do have to make up metrics or checklists to justify their decisions.

31. If you hate virtue signaling, you will hate venture capital.

32. There will always be an MBA that wants your job. If you’re a junior VC and think you’re indispensable, you’re not.

33. Venture teaches you to pattern match, but by definition, you are supposed to invest in companies that break patterns. Following the same mental heuristics as your peers will get you nowhere.

34. You don’t have to live in NY or SF to “make it” in venture today (but it definitely helps).

35. If you’re doing a lot of in-person meetings, one easy way to stand out is to not dress like everyone else. Not saying to wear loud outfits, but the Allbirds + vest + Apple Watch + tech pants look has been played out, and you look like everybody else.

36. “Don’t talk politics” only applies if you have conservative values.

37. However many LP meetings you think you need to take in order to raise your first fund, triple it.

38. Most “VC” online communities are trash. You’re better off finding the best one and being engaged there than trying to keep up in 10 different Slack / Discord groups.

39. If you haven’t built a Twitter audience by now, I’d argue that it’s not a great investment of your time. You’re competing for attention on the most-crowded platform, it’s not evergreen content, and good luck consistently saying something that hasn’t already been said.

40. The earlier you decide what you want out of your career, the better off you are. Some start a career in venture to increase their options in the future, but then they never leave. Nothing wrong with this, but if you have a plan, you can realize what actions you need to take if venture is not your final destination.

41. Most VC journalism is written by people who have never invested a day in their lives. If you're looking for VC content written by actual VCs, check this out: confluencevcweekly.beehiiv.com/subscribe.

42. Venture is a branding game. You can only earn your brand through building a track record or being loud on the internet. Which of these options do you think LPs prefer?

43. “Breaking into VC” is played out. “Succeeding in VC” is not.

44. Very little work done within a venture capital fund is repeatable. Writing quality investment memos takes time. Making reference calls takes time. Putting together LP reports takes time.

45. The better questions you ask, the more memorable you become. If you want to stand out, stop asking the same things as everybody else. Go a level deeper, and see what happens.

46. Be open to rescheduling a meeting once, but never take a meeting with somebody who moves meetings around more than that. You’re not a priority, and the meeting will be a waste of time.

47. If you’re raising a pre-seed round without traction, you’re better off finding a handful of angel investors instead of looking for venture money. More institutionalized equals more bureaucracy, and this means more people you need to convince in order to get a deal done.

48. VCs are the most likely group of people to get caught up in the “current thing”. If you work in VC, you can lap your peers by focusing on what actually matters and ignoring trends.

49. Sector specialists outperform generalist funds unless those generalist funds have sector-specific experts. The world changes faster than ever; it’s impossible to be truly knowledgeable about more than a small handful of things.

50. ChatGPT will create less entry-level VC roles, but it will give entry level investors way more leverage. If you know what you’re doing, you can 5x your output by dividing your labor costs.

51. The people that are loudest with their spending habits are usually the most insecure. This is a general life observation, but it lends itself well to VC too.

52. Venture capital sells the dream better than every other industry other than startups. What are the odds that you break into VC? If you do, what are the odds you land at a fund with returns that beat the market? If you succeed then? What are your odds of eventually earning carry? If you make it that far, what are your odds of negotiating a meaningful amount that can create wealth for yourself?

53. People like to draw patterns, and there are no patterns in the family office world. Every family is different - different paths to wealth, different generational interests, and different opinions towards investing.

54. Investing is all about longevity. You can be the best at what you do for years or even decades, but your strategy can blow up in your face at any time. The longer you stay in the game, the more impressive it becomes.

55. Positioning is the most important skill you will ever learn. Good positioning means that the best opportunities come to you instead of you having to constantly find them. Once you reach this point in investing, it’s game over.

56. Everybody wants a remote investor role except for the people hiring.

57. If you’re raising money from people and all of your marketing slides are about how your market or asset class outperforms, that gives no detail into how you are going to outperform the other players in that market or asset class.

58. Venture capital = money + deal flow + access + judgement. If you don’t have one of these, you don’t have any.

59. The majority of investments you make aren’t going to change the world, and even in a successful outcome, only a small percentage of the world will know about the company. Investing as an idealist will cloud your judgment.

60. Ego drives and kills fund returns. You don’t have to hold until and IPO for a successful outcome. A 5x on a secondary exchange is better than watching your equity position go to zero because of unexpected news.

61. The smartest investors I have met also talk the least.

62. Tech social norms are not the same as societal social norms. Trying to “fit in with the crowd” is actually making you incredibly unrelatable.

63. You are better off downplaying how smart you are vs. trying to convince everybody you’re the smartest in the room. I can’t remember a bad interaction with somebody that says, “I don’t know much about this industry, but here’s what I’m thinking. You know much more than me, so I’d rather hear your opinion”.

64. Marketing is the new software engineering. If you can find marketing channels (or engineer them yourself) for your portfolio companies, that has become more valuable than finding them another software engineer.

65. Avoid 50/50 partnerships. There is no such thing as an equal partnership, and somebody is always bringing more to the table. You’re better off addressing this early instead of waiting until resentment kicks in.

66. I have never met a person I consider successful who writes formal emails.

67. Closing deadlines aren’t real for 98% of opportunities. This applies more in fund investing than direct investing, but it applies in both worlds; it’s not very difficult to adjust legal docs to make more room for investors.

68. The bar for people you take meetings with should be rising rapidly each year.

69. In a venture firm internal political power comes from getting deals done. When the main currency for the culture is getting credit for making investments it aligns every activity around deploying capital and judges it against that bar.

70. Phone contacts > email contacts. If you aren’t close enough to text, you’re not top of mind for that person when something relevant comes in. This is a quote about investing.

71. Writing good investment memos is a skill, but it doesn’t make you irreplaceable. Great investors are great evaluators, so the more time you can spend doing this, the better.

72. The more time you spend building up pipeline, the harder it becomes to prioritize assignments. (A good rule we’ve played with us forcing the investment team to rank their top three live deals after every pipeline call to force simplicity.)

73. People forget a lot of things, but they don’t forget people that offer favors without asking for anything in return.

74. At its core, venture capital is legalized insider trading. If you’re completely reliant on publicly available information, you have no edge, and you’re not going to win in the long run.

75. Innovation pockets are real, and you should be living in one if you want to make it in this game. To the point above, do you think that the information you want is being shared in a random remote town?

76. The best investors of all time don’t get labeled that until they are in the later stages of their life. If you want early wins and acknowledgment, this isn’t the job for you.

77. All fund managers pitch J-curve returns to investors. The earlier you invest, the longer that curve becomes. If you're an LP with a shorter time horizon, you probably shouldn't be investing in seed funds.

78. The era of LP investing based only markups is over. Distributed capital is what funds are being graded on in LP meetings.

79. As a general rule, don’t trust people in VC or startups who use avatars to represent themselves. Ironically many of these people are the loudest ones on the internet when they’re too self-conscious to show their own face.

80. As an investor, you’re not the man in the arena. It’s easy to get a big ego when you act as a gatekeeper, but it’s a good reminder that magnitude of your problems are a fraction of those faced by founders.

81. Claim you're an evergreen fund if you don’t want other people to know how much money you manage. They will always assume it’s higher than it actually is.

82. If you aren’t close with somebody, they won’t directly tell you the information you want to hear. The info you actually want starts to come out after a few drinks. Rare example of drinking positively affecting your career.

83. When the cost of capital is cheap, the cost to distribute a narrative is also cheap. The inverse of this is also true.

84. The best investments should smack you in the face. If you’re spending three weeks debating it, it’s probably not right.

85. Investment managers don't actually want the best returns. They want to do things that make them feel clever, interesting, or different.

86. There are asset managers, and there are investors. Asset managers preserve capital; investors grow it.

87. You can be the smartest one in the room, but if you have no charisma, you’ve made it WAY harder to convince anybody of anything.

88. The most competition is in the middle. Companies that improve a process by 10% fill rounds WAY faster than companies that can make a dent in the universe (maybe that’s changing).

89. The best venture investors usually have orthogonal paths. Having the same path as everybody else will make you see the world through the same lens (this doesn’t equate to power law outcomes).

90. Most VCs avoid frontier tech because of the perceived R&D risk. It exists, sure, but once you get over that hurdle and prove demand, these companies develop MASSIVE moats that allow them to dominate categories. Compare this to traditional software investing where feature parity has made it harder for moats to develop.

91. If you are meeting with VCs to fundraise and aren’t talking to the partners, you should quickly try to understand how decisions are made at that fund. Not saying it’s a waste of time to talk to junior folks (they will actually grind for you), but it is WAY harder to pitch a deal upwards than it is for partners to sign off on a deal and hand off the work to the junior team.

92. Investing is a game of finding better flows of information (there is a reason that hedge funds spend billions on proprietary data). If you have no information edge (most don’t), you’re cooked.

93. Branding is about being associated with the winners of the portfolio. The brand of Sequoia has been built on the fact that they were early into Apple, Google, and others; their content marketing has very little to do with the brand they have built.

English

Chad (associate with a Wharton MBA), Steve (junior intern from Harvard), and Carl (analyst with bachelor's from Stanford) five mins before an intro call with a founder referred over by an "out of network" firm

English