Sabitlenmiş Tweet

Warren Buffett says, where others are greedy be fearful (green/renewables). Where others are fearful be greedy (black/oil).

English

Leonard Corby

4.5K posts

@corby_leonard

There's nobody like me, well maybe one. Retired IT guy. Wannabe financial advisor/tax consultant. Life lessons learned through experience. Views are my own.

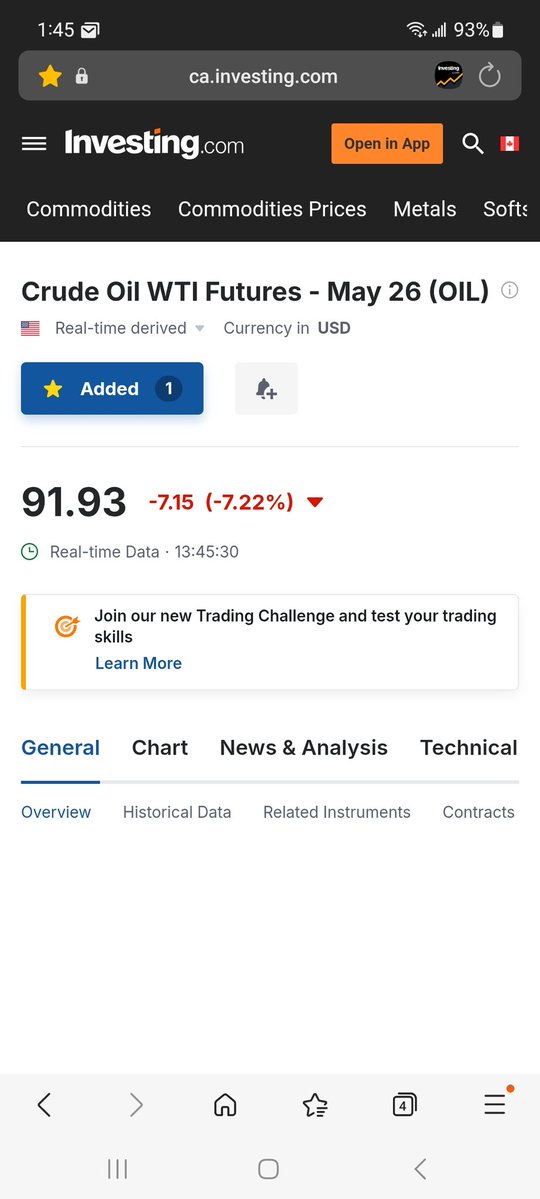

Food for thought. Chevron’s move into Venezuela says more about the new world than any communiqué from Ottawa. What Canada needs now is concrete deals and shovels in the ground at home, not another performative boondoggle dressed up as an investor summit. In recent weeks, as war and great‑power tension have snapped energy security back to the top of the agenda, Chevron has signed a deal to pour fresh capital into Venezuela’s Orinoco Belt. It is increasing its stake in a major joint venture and securing new drilling rights in one of the world’s dirtiest heavy‑oil basins, because Gulf Coast refineries need those barrels now. That is how capital behaves when energy security, not climate targets, is the first priority. Against that backdrop, Prime Minister Mark Carney will host 100 of the world’s biggest investors in Toronto this September, pitching Canada as a safe, green home for their trillions. It is an odd spectacle for a country that has spent a decade in an investment drought. Business spending has lagged peers, capital per worker has slipped, and Canadian firms and pension funds have put more money abroad than at home. Trillions have passed through Canadian hands. Too little has stayed. The core irony is that the problem is not the barrel. It is the politics wrapped around it. Canadian heavy crude is already cleaner and more tightly regulated than Venezuelan heavy. Alberta producers operate under carbon pricing, methane rules and environmental standards that Venezuela does not match. If the world is going to burn heavy oil for decades yet, it is rational to prefer more Canadian barrels and fewer Venezuelan ones. Yet the fresh capital is going to Caracas, not Calgary. Canada has turned its advantage into a liability. Ambitious climate policy has often been implemented in a way that feels performative to investors: ever‑shifting rules, sprawling reviews, talk of hard caps and now an emerging expectation that large‑scale carbon capture is a de facto requirement for future growth. Each measure can be defended on its own terms. Taken together, they signal a jurisdiction where politics moves faster than permits and long‑term projects are continually reopened. Pipelines crystallize the issue. For a decade, Canadian leaders have talked about “economic sovereignty” and reducing dependence on the U.S. market. The minimum requirement is obvious: east–west pipelines to tidewater so Canadian oil can reach Europe and Asia. Instead, major projects have been cancelled or delayed, and the only large expansion has required a federal rescue and long overruns. The most reliable route to tidewater for Canadian barrels still runs south, through American pipes and American politics. The environmental outcome is as perverse as the economic one. By making it harder and riskier to invest in relatively cleaner Canadian heavy, Canada constrains supply that could displace higher‑emissions barrels from places like Venezuela. Demand does not disappear; it shifts to producers with weaker standards. On paper, slower growth in domestic output and higher carbon prices can be presented as climate progress. In practice, what matters is which barrels actually get burned. What Canada needs now is not another stage‑managed gathering in Toronto, but bankable projects, clear approvals and real deals on Canadian soil. The world has changed; energy security is back at the top of the hierarchy. Canada, sitting on cleaner crude in a dirtier world, needs to wake up and act like it. cbc.ca/news/business/…

A few thoughts with oil down 11% on the SoH being "opened" (until April 22nd): 🛢️voyage time for tankers out is ~25 days to Asia and 25 days back = ~ 2 months of continued production loss = ~600MM Bbls = still heading to lowest inventory levels in history 🛢️IEA yesterday saying will take ~ 2 years to fully normalize production 🛢️80 facilities have been damaged, 1/3 "severely or very severely" which will take quarters/years to fix 🛢️political risk premium of $10+/bbl likely and the floor price for oil is now higher given inventory reset 🛢️SPR restocking will = ~0.3MM Bbl/d of new demand for the next 4 years 🛢️oil equities were on average discounting $70WTI. Won't matter at the open but will again soon.

God, please give me a sign