DA Sails

41K posts

DA Sails

@da_sails

Soli Deo Gloria; Policy, Supply Chain/Procurement, Clean Energy, Veteran

Katılım Ağustos 2021

5.7K Takip Edilen7.5K Takipçiler

U.S. CRITICAL MINERALS SUPPLY CHAIN HAS A PROCESSING PROBLEM…AND IDAHO NATIONAL LAB JUST MAPPED 27 FIXES

Source: INL/RPT-26-91489, DOE Office of Critical Minerals and Energy Innovation, May 2026

inl.gov/content/upload…

Permitting Gap

• U.S. mine permitting averages 7-10 years vs. 2-3 years in Canada and 1-2 years in Australia

• GAO found ineffective interagency coordination alone adds up to 3 years to project timelines

Import Dependence

• 100% reliant on imports for 13 critical minerals

• 50%+ reliant for 20 more

• China controls 91% of refined rare earth output

The Real Bottleneck

• Domestic ore is routinely exported for processing - the mine-to-market gap is a refining problem, not a geology problem

• Top 3 refining nations hold 86% of key energy mineral market share as of 2024

• China captured nearly all supply growth in cobalt, graphite, and rare earths

Workforce

• Mining engineering degrees fell 39% between 2016-2022 - only 327 degrees awarded in 2020

• 50%+ of U.S. mining workforce projected to retire by 2029

• China operates 44+ mining engineering programs

Policy Risk

• Section 45X advanced manufacturing credit phases to zero after 2033 under OBBBA

• Mine project lifecycles run 20+ years - a 2033 sunset doesn't pencil for a project starting today

• INL recommends extending the credit through at least 2040

INL can map 27 reforms. Congress has to act on 9 of them. That's the part that hasn't worked in 30 years.

$UUUU $MP $LEU $CCJ $BAM $USAR

English

DA Sails retweetledi

DOE AWARDS $94M TO EIGHT COMPANIES FOR GEN III+ SMR DEPLOYMENT

Site Preparation

· Constellation SMR Development: $17.3M for NRC Early Site Permit, New York location

· Nebraska Public Power District: $27.9M for NRC Early Site Permit, Nebraska location

Supply Chain

· BWXT Nuclear Energy: $21.4M to equip Mount Vernon, Ind. facility for reactor pressure vessel final assembly and large component manufacturing

· Framatome U.S. Government Solutions: $8.8M to expand Richland, Wash. fuel fabrication facility, adding roughly 200 MT of uranium annual pellet production capacity

· Scot Forge: $12.3M for large vertical turning lathe and gantry milling machine in Spring Grove, Ill. for large component production

· North American Forgemasters: $2.9M for new furnace in New Castle, Pa. for domestic large forging production

· Global Nuclear Fuel Americas: $3M to add a second boiling water reactor fuel rod production line in Wilmington, N.C.

· Container Technologies Industries: $548K to expand nuclear QA certifications in Helenwood, Tenn. for SMR-grade steel production

These Tier 2 awards complete the $900M Gen III+ SMR program alongside December 2025 Tier 1 awards to TVA and Holtec - the supply chain investment layer that makes the 2030s build-out executable, not just fundable.

$CEG $BWXT $GEV

English

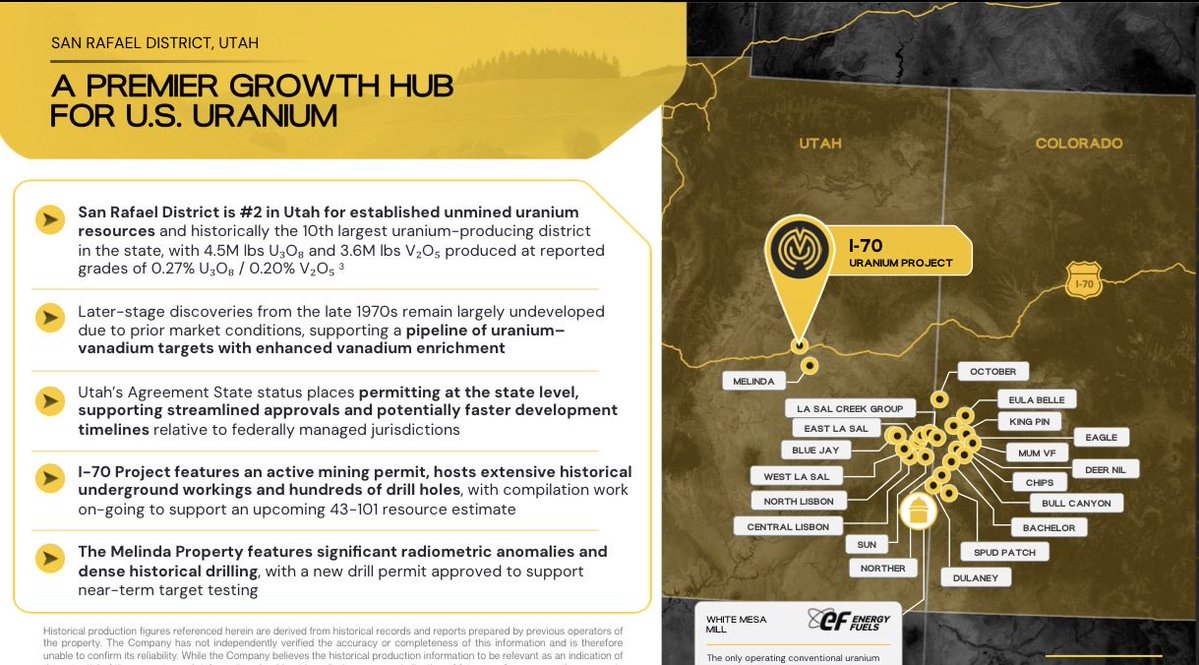

U.S. URANIUM IMPORT DEPENDENCY IS THE SETUP. MANHATTAN URANIUM IS POSITIONING FOR THE REBUILD.

Supply Context

• Per EIA data cited in the presentation: imports accounted for 99% of uranium concentrate used by U.S. nuclear generators in 2023

• Domestic production fell from roughly 43-45M lbs annually in 1980 to just 50K lbs in 2023, with a partial recovery to ~677K lbs in 2024

• One operating conventional uranium mill remains in the U.S. - Energy Fuels' White Mesa facility in Utah - with excess capacity

Portfolio Footprint

• 25 U.S. projects spanning Utah, Colorado, and Nevada - 15 with historical production - totaling 25,000+ acres

• Core districts: San Rafael, Lisbon Valley, La Sal, and Uravan (Utah/Colorado); Apex Mine (Nevada)

• Apex Mine: largest historical uranium producer in Nevada's history - historically accounting for roughly half the state's all-time output

• Athabasca Basin (Saskatchewan): Murmac and Strike projects along proven mineralized corridors

Key Catalysts - 2026

• Murmac (Athabasca Basin): 25-30 hole drill program fully funded for H2 2026; 2024 discovery hole returned 8.4m of 0.3% U3O8 including 1.2m of 1.79% U3O8

• I-70 Project (Utah): footprint expanded ~255% via Jupiter and Energy Sands additions to 4,416 acres; 43-101 resource estimate work ongoing

• Apex (Nevada): drill permits expected H1 2026; historical intercepts include 34.1m of 0.37% U3O8 and 15.2m of 0.51% U3O8

• Historical resource base across portfolio: ~9.66M lbs U3O8 at avg 0.12% eU3O8 - not yet NI 43-101 compliant; 43-101 upgrade work is a stated objective

The domestic uranium supply gap is a policy problem with a procurement dimension - explorers with permitted U.S. conventional assets and proximity to White Mesa are positioned at the earliest stage of a potential rebuild.

$MANU $UUUU $EFR

English

S&P GLOBAL: OIL AND LNG VOLATILITY IS ACCELERATING THE NUCLEAR CASE

Macro Driver

• Middle East conflict has shifted from a flow disruption to a broader supply crisis, sharply downgrading 2026 global demand growth expectations for oil and LNG

• Nuclear is being repositioned as an energy-security hedge against geopolitical instability and fossil fuel supply chain exposure

Reactor Build Momentum

• More than two-thirds of the world's reactors under construction are in Asia, with close to 40 units in China alone

• Japan's return of large reactors to commercial operation in Q2 2026 is reducing LNG exposure at scale

• S&P estimates a 1-GW reactor displaces roughly 850,000 mt/y of LNG, 26,710 bbl/day of oil, and 2.22 million mt/y of coal

Supply Squeeze

• Platts assessed U3O8 spot at $83.75/lb on Jan. 14, 2026 - the highest since August 2024 - with utility and investor buying cited as the driver

• Kazatomprom cut its 2026 production guidance in April, prioritizing value over volume, signaling limited elasticity even at elevated prices

• Recent projects - Burke Hollow (US), Phoenix ISR/Wheeler River (Saskatchewan), DASA (Niger) - are only emerging from a decade-long post-Fukushima downturn with limited operating track records

• New mine volumes typically arrive years after construction greenlight, leaving near-term supply response structurally constrained

S&P's read: supply response is slower and more complex than headline resources suggest, keeping uranium prices supported and volatile as Middle East risk intermittently tightens risk premiums.

$CCJ $NXE $UUUU $LEU $URNM

English

INDIANA MOVES TO BECOME AN NRC AGREEMENT STATE

Agreement Request

• Gov. Mike Braun formally requested Agreement State status from the NRC on Jan. 29, 2026

• Under the proposed agreement, NRC would transfer regulatory authority over 213 active licenses to the Indiana Dept. of Homeland Security (IDHS)

• Indiana's Radioactive Materials Control Program (RMCP) would assume jurisdiction over byproduct material, source material, and special nuclear material in quantities not sufficient to form a critical mass

NRC Retained Authority

• NRC retains full authority over production and utilization facilities, uranium enrichment, import/export, and byproduct material under Section 11e.(2) of the AEA

• Indiana cannot regulate any activity reserved to the Commission under 10 CFR Part 150

Program Structure

• RMCP staff will total four FTEs operating under IDHS

• Indiana adopted NRC regulations in 10 CFR Parts 19, 20, 30-37, 39, 40, 61, 70, 71, and 150 into Indiana Administrative Code Title 290

• NRC staff concluded the program is adequate to protect public health and safety and compatible with NRC's regulatory framework

E.O. 14300 Wrinkle

• The notice flags that as NRC revises its regulations under E.O. 14300, Indiana and all Agreement States will need to update their own rules to maintain compatibility within specified timeframes

Public Comment

• Comment period: 30 days from May 15, 2026 publication

• Docket ID: NRC-2026-1387 at regulations.gov

Agreement State expansion is steady-state regulatory decentralization - but the E.O. 14300 flag embedded in this notice signals that every state radiation control program in the country now carries reform-era regulatory update obligations.

English

CCEC RESTART FACES ACTIVE OPPOSITION ON TWO REGULATORY FRONTS

FERC Front - CIR Waiver Challenge

• CEG filed March 31, 2026 requesting waiver of three PJM OATT provisions to transfer Capacity Interconnection Rights from Eddystone Units 3 and 4 to Crane (859 MW)

• PJM's Independent Market Monitor filed answer May 11, 2026 urging denial on four grounds: impermissible assumptions about study outcomes, harmful precedent, circumvention of independent review, and availability of existing Tariff-compliant alternatives

• PJM stated on record it has not reviewed or validated CEG's analysis and that planning studies control

• IMM notes waiver denial would not prevent Crane from operating - CEG could proceed as an Energy Resource pending full deliverability determination

NRC Front - License Amendment Challenge

• CEG filed three amendments to Renewed Facility License No. DPR-50 to reauthorize power operations through April 19, 2034

• Intervenor filed hearing request April 27, 2026 with two contentions

• NRC Secretary dismissed first contention May 11, 2026 as procedurally deficient

• Second contention referred to Atomic Safety and Licensing Board - board formally established May 15, 2026 (Docket 50-289-LA)

FERC has not yet ruled. With a Microsoft PPA anchoring the project economics, CEG is navigating simultaneous grid interconnection and license amendment proceedings on a compressed timeline.

Sources: FERC Docket ER26-2028-000, Accession 20260511-5073 (May 11, 2026) / Federal Register Vol. 91 No. 94 (May 15, 2026)

$CEG $MSFT

English

WHAT WE CALL EXPENSIVE SAYS MORE ABOUT OUR METRICS THAN OUR ENERGY

Source: EIA AEO2026 Electricity Market Module Assumptions, April 2026

New Build Overnight Costs (2025$)

· Nuclear LWR: $8,255/kW | 2,156 MW | 6-year lead time

· Nuclear SMR: $9,831/kW | 480 MW | 6-year lead time

· Natural Gas CC: $1,086/kW | 627 MW | 3-year lead time

· Wind (onshore): $1,712/kW weighted regional avg

· Solar PV: $1,484/kW weighted regional avg

Gas Build Costs Are Rising

· Simple-cycle turbines up ~40% vs prior estimates

· Combined-cycle up ~20%

· Driven by labor and material shortages

· Source: Brattle/Sargent & Lundy PJM CONE Study, April 2025

What Overnight Cost Misses

· Nuclear eligible for up to 80-year operating life via NRC renewals

· Gas plant design life: ~30-40 years

· Wind/Solar: ~25-30 years

· Nuclear figures exclude post-2024 IRA/OBBBA production tax credits

· Nuclear LWR regional range: $7,866/kW (Texas) to $9,792/kW (Chicago)

Full System Cost (LFSCOE)

· Nuclear: $90-$122/MWh

· Wind: $131-$483/MWh

· Solar: $177-$749/MWh

Source: Idel (2022), cited in Quantified Carbon/UNECE FSCOES Report (2025)

Federal Financing (DOE Title 17 / EDF Program)

· DOE loan guarantees available for new nuclear at Treasury + 0.375%

· Merchant nuclear credit spreads historically 300-500 bps above Treasury

· On an $8-9B debt stack over 30 years, EDF financing can reduce interest burden by $200-400M+ vs. private markets

· EDF covers up to 80% of eligible project costs

· No innovation requirement for new nuclear construction under Section 1706

Source: DOE Office of Energy Dominance Financing, Title 17 Program Guidance, May 13, 2026

The metric you choose determines the conclusion you reach. Nuclear's cost premium over wind and solar narrows sharply or disappears entirely when the full picture is counted.

$CCJ $BAM $LEU $URNM $NXE $VST $CEG

English

UAE IS BUILDING THE NUCLEAR WORKFORCE PIPELINE FROM THE GROUND UP

Agreement Details

• ENEC and Abu Dhabi's Department of Government Enablement signed a 5-year strategic cooperation agreement via Mawaheb Talent Hub

• Target: qualify at least 100 UAE Nationals across high school, vocational diploma, and postgraduate levels

Candidate Pipeline

• Mawaheb Talent Hub supplies curated candidates and provides facility access for awareness workshops, technical assessments, and interviews

• ENEC leads training program development and funding, including financial support for trainees

Workforce Integration

• Completers who meet hiring criteria are placed directly into ENEC's workforce and subsidiaries supporting Barakah operations

• Barakah's 4 operating units produce 40 TWh/yr of clean baseload power, covering 25% of UAE electricity demand

Context

• ENEC has already involved 2,000+ Emirati professionals in Barakah's development and operation across six talent pipeline programs

The Barakah model is maturing into a full domestic workforce ecosystem - the UAE is not just operating reactors, it is building the human capital base to own them generationally.

$URNM $URA

English

DA Sails retweetledi

FY2027 HOUSE ENERGY-WATER BILL DROPS: NUCLEAR AND AI SURGE, RENEWABLES CUT DEEP

Top-Line Numbers

· $58.5B total discretionary, $461M above FY26 enacted

· $35B defense / $23.5B nondefense

· DOE total: $50.359B, $456M below FY26 enacted

NNSA and Nuclear Deterrent

· $27.072B for NNSA, up $1.67B from FY26

· $22.07B for Weapons Activities

· $2.39B for Naval Reactors, including Columbia-class submarine reactor development

· $2.08B for Defense Nuclear Nonproliferation

· Additional funding for Uranium Processing Facility ahead of commissioning

Civil Nuclear

· $1.8B for Nuclear Energy account, up $15M from FY26

· HALEU fuel cycle funding included to reduce reliance on Russian and Chinese sources

· $2.675B transferred from unobligated BIL funds into Nuclear Energy for SMR and advanced reactor demonstrations (Sec. 313)

· $100M credit subsidy for advanced nuclear loan guarantees

· Goal stated: quadruple U.S. nuclear energy capacity by 2050

Science and AI

· $8.525B for Office of Science, up $125M from FY26

· Increased funding for HPC, quantum computing, and AI; funds Genesis Mission EO

· Advances fusion energy sciences toward grid deployment

· NRC: $878.1M appropriated, offset by fees

What Gets Cut

· Critical Minerals and Energy Innovation (formerly EERE): $1.85B, down $1.25B from FY26

· ARPA-E: $300M, down $50M from FY26

· Office of Clean Energy Demonstrations: eliminated

· Office of Energy Justice and Equity: eliminated

Timeline

· Subcommittee markup: May 15

· Full committee markup: May 21

· Senate passage requires bipartisan support

· Final bill unlikely before November elections

The Section 313 transfer is the most consequential nuclear supply chain provision in the bill. Congress is redirecting $2.675B in stranded clean energy funds directly into SMR and advanced reactor deployment, turning unspent Biden-era infrastructure dollars into nuclear buildout capital.

$CCJ $BAM $LEU $UUUU $NXE $URNM

English

POLAND'S NUCLEAR PIVOT IS A BILATERAL STRATEGIC ASSET

Secretary Wrochna Remarks

· Coal represented roughly 90% of Polish electricity production five to six years ago, standing near 60% today

· First AP1000 unit targeted for commissioning in 2036, with Westinghouse and Bechtel as partners; Polish government committed $17 billion directly from the state budget for the first three units

· EU-ETS carbon pricing is forcing expensive coal to remain online during the 10-year nuclear bridge period; Secretary Wrochna framed faster reactor deployment as the most direct solution

· Gas-fired capacity seen as a necessary bridge technology through 2036; LNG is a central component; Poland is among the top-three importers of U.S. LNG in Europe, having fully phased out Russian gas

· Baltic Pipe delivers Norwegian gas through Denmark; U.S. LNG accounts for roughly half of Poland's ~20 BCM annual gas consumption

Supply Chain Signal

· Polish government objective is not just reliable electricity; it is building a qualified domestic nuclear supply chain that can compete globally for new builds across Europe

· Universities and engineering schools being incentivized to grow nuclear workforce; Polish construction sector cited as a comparative advantage given its large-scale infrastructure delivery record

Energy security without sovereignty is not sovereignty. Poland is building nuclear to end dependence on Russian leverage and inviting U.S. industry to build alongside them.

$CCJ $BAM $LEU $BWXT $SMR

English

DA Sails retweetledi

DOE JUST DROPPED UPDATED TITLE 17 ENERGY FINANCING GUIDANCE - NUCLEAR IS A PRIMARY TARGET

What Changed

• "Energy Infrastructure Reinvestment" renamed Energy Dominance Financing Program (EDFP) per One Big Beautiful Bill Act, signed July 4, 2025

• GHG requirements and community benefit plan eliminated

• Critical minerals explicitly added as eligible category

• Funding extended through FY 2028

EDFP Nuclear-Eligible Projects

• New nuclear plant construction

• Expansion at existing nuclear sites

• Advanced reactors, components, and front-end fuel cycle facilities

• No innovative technology requirement

Loan Terms

• Up to 80% of eligible project costs

• Tenor up to 30 years

• Loans typically $500M or more; $250B in authority available

$250B sitting behind the nuclear buildout. The policy runway is clear.

$CCJ $BAM $LEU $NXE $URNM $XE

English