Sabitlenmiş Tweet

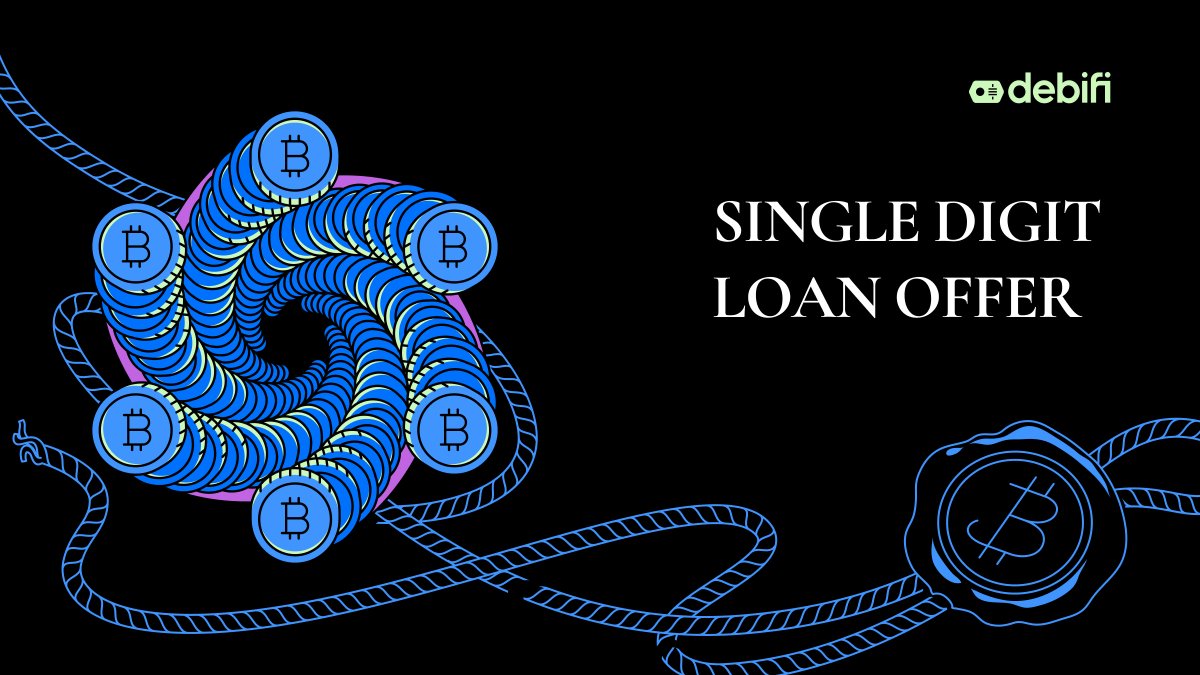

Unlock Debifi’s lowest APR #Bitcoin backed loan! 🔥

Goldstream Fund now offers 8.5% APR (+ 1% origination fee = 𝟵.𝟱% total) 🚀

💰 $1,000,000–$3,000,000 in USDT

⏳ 6–12 months

🔒 50% LTV

Visit: debifi.com/offers/1f0ebca…

English

Debifi

3.7K posts

@debificom

Non-custodial Bitcoin-backed lending with institutional-grade liquidity and zero rehypothecation.