bir yudum su

9 posts

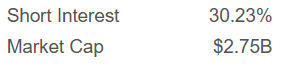

Paylaştığım görselde de görüldüğü üzere, $EOSE hissesinde short interest oranı %30 seviyelerinde.

Bugün gelen bilanço ve pozitif haber akışı, bu yüksek short pozisyonu potansiyel bir squeeze’e dönüştürebilir.

Kısacası, bu oran doğru katalizörlerle birlikte hissede ciddi bir yukarı yönlü hareketin yakıtı olabilir.

Yatırım tavsiyesi değildir.

Türkçe

Agreed high-level directionally, $FLNC compelling at $3B valuation post-earnings after taking a closer look.

Very rare to see a US energy player that small get 2 direct Hyperscaler deals...

The $5.6B+ backlog derisks the company growth, not including new hyperscalers backlog like $GOOGL or $MSFT.

The hyperscaler deals were framework agreements, which are likely to convert "soon" Q3 this year, and aren't included in numbers.

Once that's released it's major positive catalyst, similar to qualification -> volume ramp in semi players.

Citi Analyst: "The possibility of a hyperscaler order will likely overshadow everything else in the quarter. We expect a positive reaction to the announcement"

I'm going to go ahead and guess they'll likely rerated once they announce their hyperscaler orders maybe anytime in the next 3 months so I jumped on the boat as a short term catalyst trade. (not just 1 but 2)

Also, if they hit ~$288M net income off gross-margin expansion ($6B revenue, 13.0% gross margins) from their software segment expansion, ~11.6x fwd p/e for 2027.

The current stock price is -50% Feb's prices despite hyperscalers + backlog de-risking the company looks like a great entry point to me (NFA).

KaizenInvestor@Kaizen_Investor

Just listened to the earnings call from $FLNC and decided to add to my position at $16.67. The earnings were spectacular in my opinion. Yes, they missed revenues due to a delayed shipment of $80 million, but the backlog keeps rising and Fluence management is confident they can deliver. 50% of the backlog comes from new customers and the main part of this backlog is for datacenter purposes. The datacenter backlog is around 12 GW, with the major part of this connected to 2 hyperscalers. To give you an idea, Fluence now have around 22GW deployed or contracted globally. So, this is a major deal. They announced 2 MSA's with major hyperscalers and are expecting a first order in Q3 already. They also said that they would speed up delivery for these hyperscalers and are expecting deliveries within a year. So, we should see first revenues from these deals in 2027. They also explained the heavy selection process for these hyperscalers. Apparently 26 companies were notified, but due to the difficult technical specifications most of the companies could not fit the standards. The main reason they were able to agree these MSA's was due to the fact that their technology is already proven. He spoke about the Fluence lab, so I suppose these Hyperscalers visited the lab and approved. The main focus remains on top-line growth. There were some questions about the high OPEX costs in percentage of revenues but Fluence want to control these by growing revenues instead of lowering costs. Happy to have started a stronger position here. Datacenters are looking for high quality of power to get them through the fluctuations and it looks like Fluence can provide it. Now valued at $3.4B with a $5.6B backlog, still looks pretty cheap.

English

@rzayev7895 Üstad, ONDS için fikirlerin nelerdir? Son günlerde iyi satış yedi, 17 Mayısta sanırım bilançosu var, fikrini merak ediyoruz.

Türkçe

$IONQ babalar sözünü tutar. Quantum tarafında doğru düzgün para kazanan tek şirket.

The Earnings Correspondent@earnings_guy

$IONQ (IonQ) #earnings are out:

Türkçe

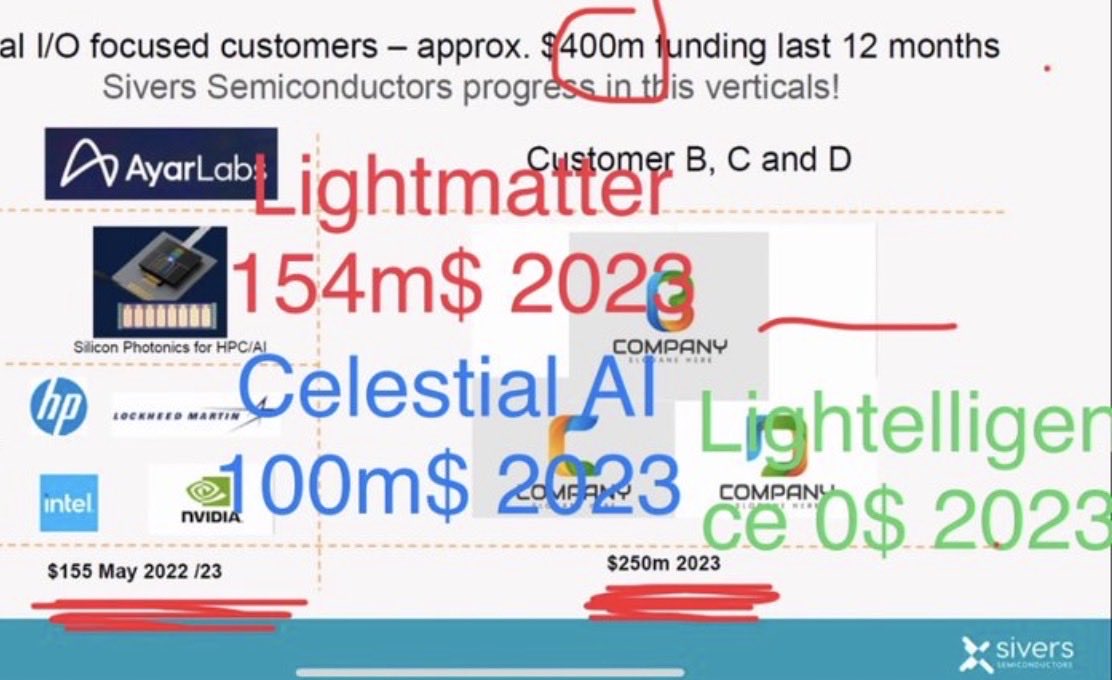

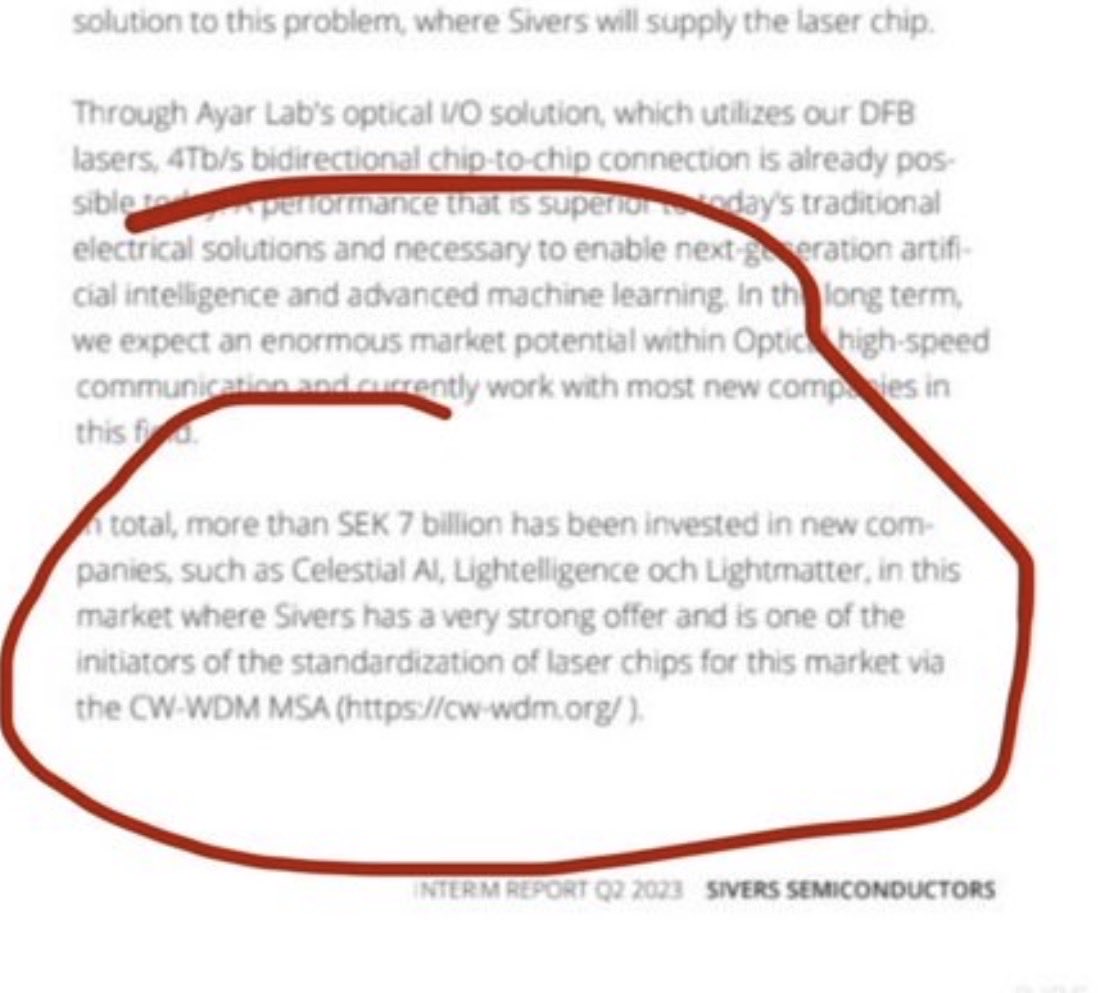

Fun thing to note: $SIVE / $SIVEF is the likely undisclosed laser supplier for Lightelligence as well.

Credit to: Plaskpojen for the OSINT find.

Zephyr@zephyr_z9

Lightelligence is developing a CPO solution for Biren And if u believe in optical computing, then it's the best pure play available on the public markets anywhere

English

@aleabitoreddit Dear Serenity, when should we take into account Valens Semiconductor?

English

It's pretty insane to see $SIVE become a Tier 1 laser supplier for CPO.

This is my prediction/guess with est. mapping:

$NVDA ate up all the capacity with $COHR, $LITE after their new $2B+ spending spree.

Same playbook with EML early 2025, causing the bottleneck seen today.

Now, $AMD / hyperscalers are scambling for upstream laser suppliers.

Hence why $SIVE + Win / $GFS became likely primary route to go down.

You can see this with:

-> $MVL CPO through Celestial (Nvidia signed a deal, but they don't have lasers)

-> $AMD CPO

-> Ayar

-> $POET

-> Lightmatter

-> and other programs (eg. Jabil 1.6T)

As a result, Sivers/Win emerged as the Tier 1 bleeding edge + critical independent laser supplier.

And there's hints for this when:

1. $GFS listed $SIVE / $LITE as the two only public laser suppliers in their ecosystem.

2. Ayar removed $LITE / $MTSI off their website and elevated $SIVE to their primary laser supplier.

So everyone else ended up going with Sivers since $COHR / $LITE are fully allocated.

My guess is that a lot of the secondary suppliers also capture overflow as architectures standardize.

But scramble for this chokepoint will be insane early next year given $NVDA bottleneck.

And a small $1.2B Swedish company in $SIVE will be in the center of it.

English

@doganay_kaya35 Ne zaman bölüneceğiyle ilgili net bir tarih var mıdır?

Türkçe

#ktlev

Haftaya başlamadan önceki projeksiyon;

Öncelikle bizi ilgilendiren en önemli veri PKZ, PCS fonları ve kredili işlem yasağından dolayı taşıdıkları kredi pozisyonu.

Büyük bir kısım teminat verimliliği ve hareket öncesi PKZ den PCS ye geçti.

Haliyle;⬇️

Türkçe

@doganay_kaya35 Hocam 600 hedefi bedelsiz bölünme dahil hedef midir?

Türkçe

Son olarak büyük hareket yasak bitince başlayacak. Öncelikle PKZ de güçlü pozisyonu sebebiyle kredili hemde diğer fonlarda ki para girişi vasıtasıyla ana hedefimiz olan 600 bandına gideceğiz inşallah.

Yatırım tavsiyesi değildir.

#ktlev

Türkçe

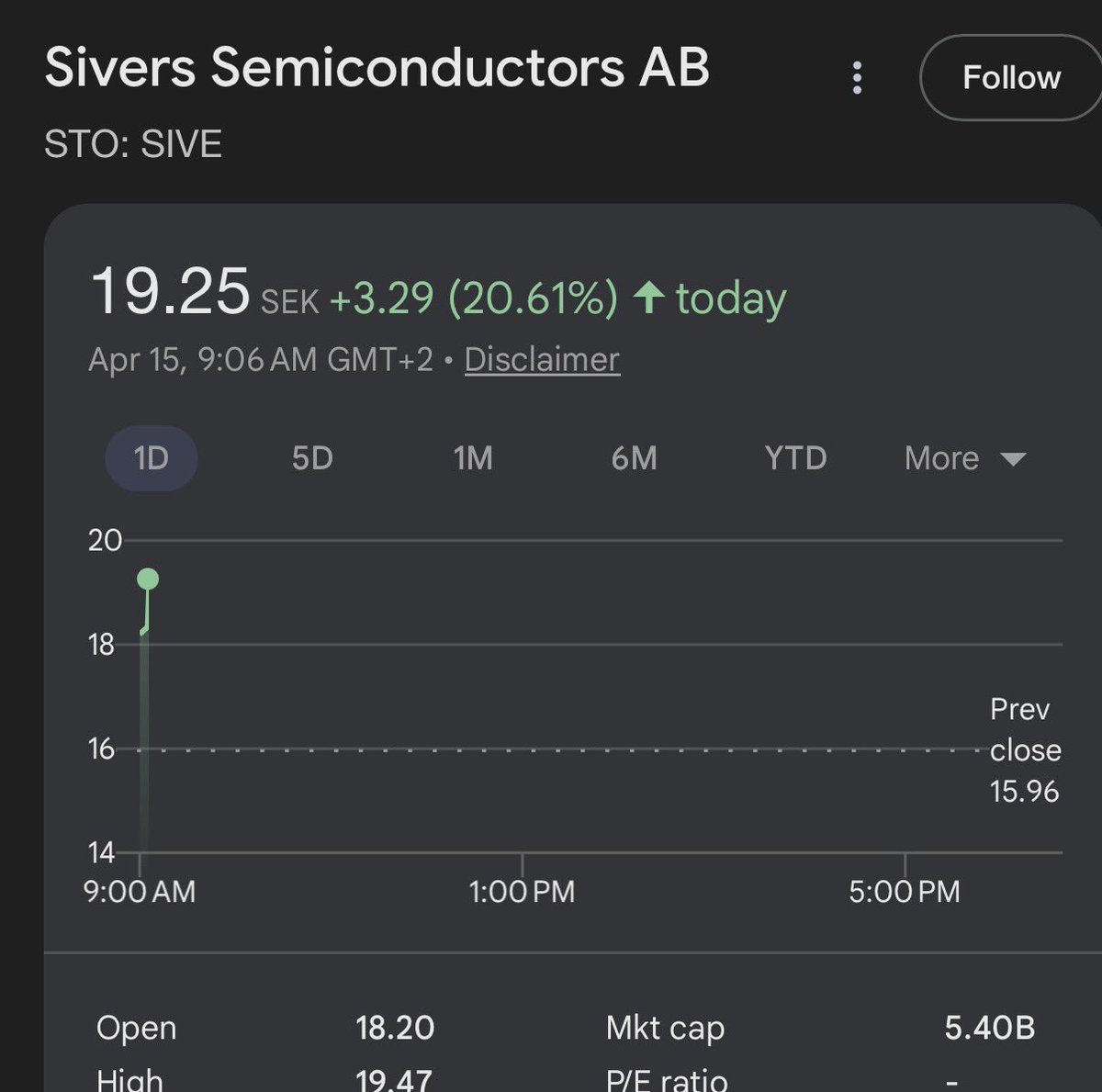

$SIVE is the next $LITE at $560m MC.

Institutions just got full confirmation today:

Sivers is now the light source in hyperscaler supply chains and the direct supplier of $JBL optical transceivers.

It’s only a matter of time.

Serenity@aleabitoreddit

IT'S OFFICIAL: $JBL to use $SIVE Lasers for their optical transceivers. Today: "Jabil plans to develop a 1.6T linear receive optical (LRO) transceiver module using Sivers’ high-performance Distributed Feedback (DFB) lasers" Jabil Photonics: :Working with Sivers will allow us to deliver a 1.6T LRO solution that meets both data center performance and power targets at scale" Where have you seen the LIGHT SOURCE for hyperscaler supply chains... At a $500m MC? We had this hinted from physical sources at OFC, but many institutions needed actual confirmation like this.

English

07 Nisan 2026 Salı - Tera Yatırımın Bugün En Çok Sattığı Hisseler Analizi

Net satış yaptığı hisseler.

- Toplam Alış: 10.46 Mr

- Toplam Satış: 9.31 Mr

- Net Pozisyon: Yaklaşık +1.15 Mr net alım

- Kar/Zarar: -18.40 Mn (gün içi hafif zarar)

En Çok Satılan Hisseler

1. #MRGYO → -2.16 Mn net satış

2. #EKGYO → -1.89 Mn

3. #BUCIM → -1.21 Mn

4. #EYGYO → -1.16 Mn

5. #FROTO → -1.06 Mn

6. #ISKPL → -741.647

7. #MARTI → -540.484

8. #PSGYO → -526.198

9. #YKBNK → -425.500

10. #TEKTU → -410.586

Daha aşağıda #MERKO, #SANFM, #YESIL, #SKTAS, #FORMT, #KZBGY, #YYAPI, #SELVA, #GUNDG gibi orta ve küçük ölçekli net satışlar devam ediyor.

Net Hacim tarafında en yüksek satış hacimleri #FROTO (-104.31 Mn), #GUNDG (-182.76 Mn) ve #YESIL (-535 bin adet) öne çıkıyor.

Kısa Yorum & Analiz

- GYO ve Gayrimenkul Ağırlığı: Listenin başında #MRGYO, #EKGYO, #EYGYO, #PSGYO gibi gayrimenkul yatırım ortaklıkları yoğun şekilde satılmış. Bu, portföyde GYO tarafında kar realizasyonu veya pozisyon küçültme yapıldığını gösteriyor. Özellikle #SVGYO alım tarafında güçlü yer alırken, diğer GYO’larda net satış olması ilginç bir ayrışma.

- Otomotiv ve Sanayi: #FROTO (Ford Otosan) ciddi miktarda net satış görmüş. #BUCIM (Bursa Çimento) ve #ISKPL gibi sanayi hisseleri de satış baskısında.

- Banka ve Diğer: #YKBNK’ta da net satış var. Bu, bankacılık tarafında hafif pozisyon azaltma olarak okunabilir.

- Genel Strateji Bağlamı:

Önceki alım listesinde #SASA ağır yüklenirken, burada #FROTO, #GUNDG, #MRGYO gibi hisseler satılarak fon yaratılmış görünüyor. Bu, kar realizasyonu + agresif #SASA long’u şeklinde bir takas stratejisi olabilir. Hesap genel olarak net alım yapmış olsa da gün sonu -18.40 Mn zarar yazması, satılan hisselerin gün içinde daha iyi performans göstermesi veya alınanların geri çekilmesiyle ilgili olabilir.

Bugün BIST-100 yatay-negatif bir seyir izledi (gün içi dalgalı, kapanış civarı %0.9-1.3 civarı kayıp bölgesinde). Bu satışlar, portföyü #SASA ve seçili kimya/enerji/holding hisselerine doğru kaydırma hareketi olarak duruyor.

Özetle:

#TERA / #FON_EKO bugün #SASA’ya çok ciddi alım yaparken, GYO grubu (#MRGYO, #EKGYO vb.), #FROTO ve bazı sanayi-bankacılık hisselerini net satmış. Bu, sektör rotasyonu ve kar realizasyonu içeren aktif bir portföy yönetimi gibi görünüyor. Özellikle GYO’larda satış baskısı dikkat çekici.

Risk uyarısı:

Bu sadece ekran görüntüsüne dayalı gözlem ve yorumdur. Kişisel yatırım tavsiyesi değildir. Piyasa çok volatil, kendi araştırmanızı yapın ve profesyonel danışmanlık alın.

Yenimahalle, Türkiye 🇹🇷 Türkçe