Dhaval Parikh

10.2K posts

Dhaval Parikh

@dhavalp

Investor/Trader since 2005 | Arbitrage | Building financial bots using AI / ML | Birder | Wildlife | Founder @ https://t.co/5bV8t1GiZC | DM for collabs.

Mumbai / Ahmedabad Katılım Aralık 2008

119 Takip Edilen13.9K Takipçiler

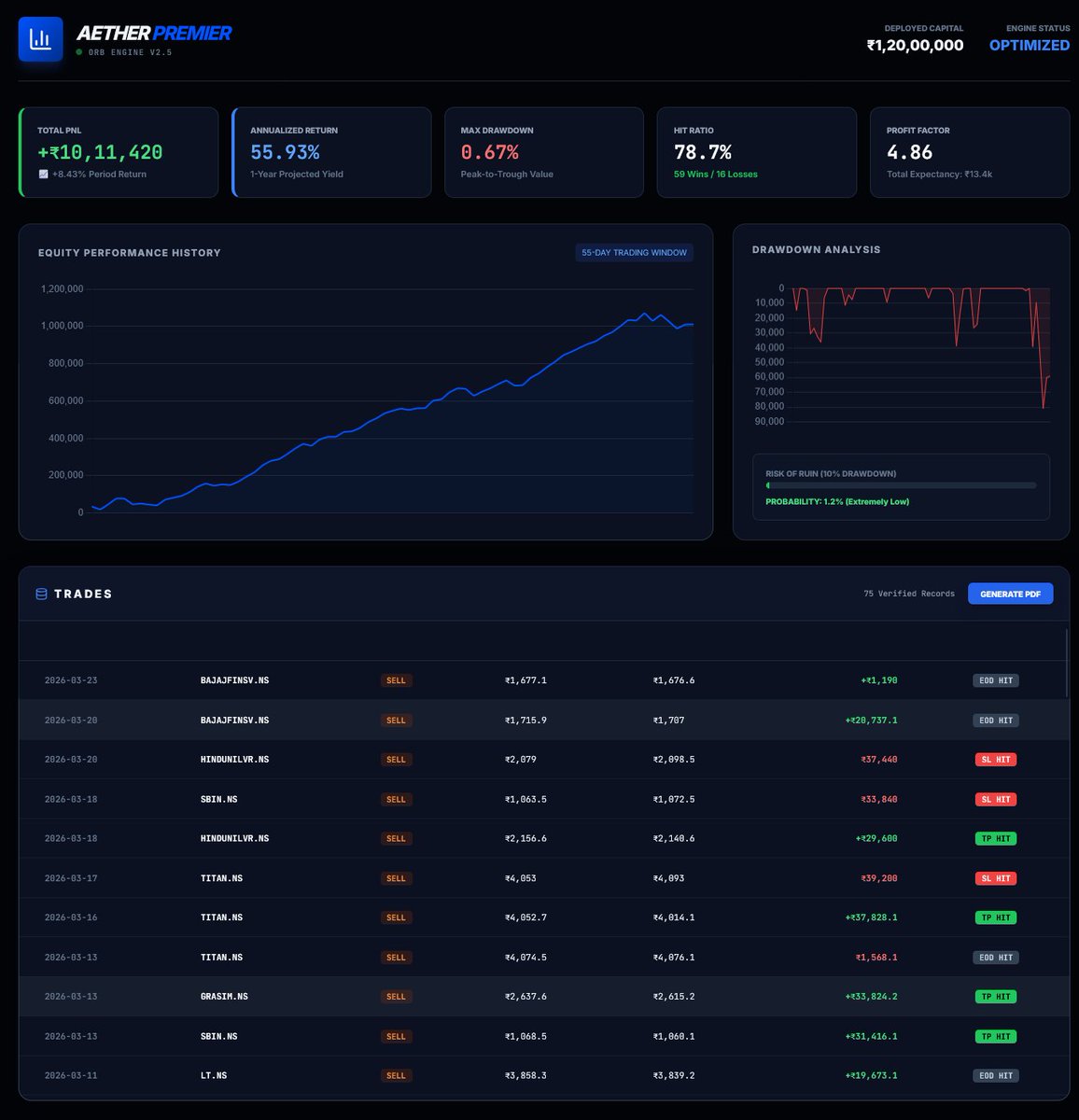

A complete automated trading system which generate alpha on my existing portfolio. It does trading on both the sides. Buy trades when trend is up and sell when trend is down. Trades only nifty 50 stocks

A system I was working on past several years. Last 2 months real performance with actual trade execution.

#TradingStrategies #bots #algotrading

English

@Prabinmen One of my favorite stock. Below 150 its a doubler in 2 years.

English

@mystock_myview Short term mein paisa ban gaya to trading

Loss me aa gaya stock to Investing 😆

Indonesia

Trading aur Investing me farak nahi samjha…to paisa market le jayega.

Mostly, log 2 galti karte hai 👇

📉 Investment ko trading bana dete hai

📈 Trading ko investment bana dete hai

Result. = Confusion + Loss

Clear hona padega 👇

👉 Short term

👉 Long term

Aap kya kar rahe ho ? .. express yr self

Trading 👍🏻

Investing 💪🏻

Filipino

IT Sector Update - Sound and Fury: The AI Question!

The Nifty IT index has witnessed a sharp correction over the past few months, declining ~25% YTD, primarily driven by rising concerns around the potential impact of Generative AI (Gen AI) on the long-term business model of IT services companies, along with macro and geopolitical uncertainties. Large-cap and midcap IT stocks have corrected meaningfully despite relatively stable operating performance and continued deal wins, as investors reassess near-term growth visibility and the potential structural implications of AI on traditional services delivery models.

However, historical technology transitions such as ERP adoption, cloud migration and digital transformation cycles suggest that while new technologies may initially compress revenue growth, they eventually expand the total addressable market (TAM) for IT services companies.

For details, click on the link below:

icicidirect.com/mailcontent/id…

English

Stock to Study : MSP Steel & Power Ltd (MSPL) - 3 weeks of continuous promoter buying

Company Snapshot

MSP Steel & Power Ltd is a mid-sized integrated steel player in India, primarily producing sponge iron, billets, TMT bars, structural steel, and power (captive). It operates facilities in Chhattisgarh with a focus on long products for construction and infrastructure. The company benefits from domestic steel demand (infra, real estate), but remains highly cyclical with exposure to raw material volatility (iron ore, coal) and realizations. Promoter group has been actively increasing stake (recently to ~40.22% via open market purchases), signaling confidence.

Guidance & Outlook from Q3 FY26 Concall (Feb 2026)

No detailed public concall transcript or explicit numerical guidance was available. Management commentary (inferred from results and filings) focused on operational resilience amid weak steel prices and demand softness. Key highlights include ongoing debt restructuring (Right of Recompense liability impacting 9M results) and efforts toward cost optimization. Promoter buying in Feb-Mar 2026 indicates internal optimism on recovery. No formal FY26/FY27 revenue or margin targets disclosed; focus remains on volume stability and margin protection in a challenging environment.

Valuation Analysis & Projections

FY26 Estimates (conservative, based on 9M trends and Q3 performance):

- Revenue: ~₹2,600–2,800 Cr (modest decline/flat YoY amid pricing pressure).

- EBITDA: ~₹140–160 Cr (margin ~5–6%, compressed).

- PAT: Negative to marginal (impacted by exceptional items of ~₹101 Cr in 9M related to debt restructuring).

Implied Multiples at ~₹28–29 (as of 23-24 Mar 2026 close):

- TTM P/E: Negative (~ -19x to -20x due to losses).

- EV/EBITDA: ~12–14x (elevated on low EBITDA).

- P/B: ~1.7–1.9x (Book Value ~₹15–17).

Order-book visibility: Limited (typical for steel long products; more volume-driven than contracted backlog). Compared to steel peers (often 10–30x P/E on recovery), MSP trades at deep discount reflecting losses and cyclical weakness, but with potential re-rating on steel price recovery and debt resolution. Limited analyst coverage; no strong consensus targets available.

Key Positives

- Promoter confidence: Aggressive stake increase to 40.22% in recent months via open market buys.

- Q3 sequential improvement: PAT turned positive ₹5.49 Cr (vs loss in Q2); EBITDA ~₹32 Cr.

- Integrated operations with captive power helping cost control.

- Low absolute valuations for a steel play with infra tailwind potential.

Key Risks (mitigated but monitor)

- Weak Q3/9M performance: Revenue down YoY/QoQ; 9M net loss ₹51 Cr due to exceptional RoR liability.

- Cyclical steel sector headwinds (low realizations, muted demand from construction/infra slowdown).

- Debt-related overhang (restructuring ongoing; exceptional items).

- Thin margins and high operational leverage in downturns; limited growth visibility.

Longer-term: Steel demand recovery from infra push + operational efficiencies could drive earnings turnaround and 15–20%+ CAGR potential once cycle improves. Position size accordingly; suitable for deep-value, high-risk cyclical steel portfolios with patience for recovery. Monitor Q4 FY26 results, steel price trends, debt resolution, and promoter actions closely.

Stock Valuation and Projected Price Target :

At current valuations (~₹28–29), MSP Steel & Power offers high-risk, high-reward as a deeply discounted, cyclical steel player. The combination of promoter buying, sequential PAT improvement, and extremely low multiples justifies a re-rating on any steel cycle upturn (target price ₹40–55 over 12–18 months, 40–90%+ upside potential if realizations recover and losses reverse; limited analyst coverage implies higher volatility).

#MSPL #StockMarketIndia #Nifty #Investing #StocksToWatch #ShareMarket #Sensex #promoterbuying

English

Nifty support at 22931.

Crossing todays high will open up target of 23618

All levels are SPOT levels

#nifty

English

@Harshit28Arora @Ashish1Nanda I agree historical data, 5 min data atleast should be made available. Other providers like dhan is giving it via api

English

@Ashish1Nanda Please make historical data available as it is essential to calculate indicators during trading

English

‼️ Trade API users ‼️

Static IP mandatory from 1st April. After 2 more trading sessions, you won’t be able to trade, if static IP is not updated.

All details here: kotakneo.com/platform/kotak…

English

Same thing happened with me in goldstone infra (olectra). I bought at 18 rs and after holding for 5 years or so it went to 180 rs and i sold all based on valuations etc etc

After few years another friend of mine who had bought on my suggestion (had invested some 1 lakh at 18 rs) called me and said my broker told me ki aapke stock ka value 1 cr ho gaya hai ab kya karu.. I just laughed and said give it to me 😜

Sometimes forgetting about a stock May be a boon in hindsight.

Sunil Gurjar, CFTe@sunilgurjar01

I bought TTK Prestige at Rs.15, and got chance to meet TT Jagannathan in Banglore, but I skipped it and sold my shares at Rs.200. Today it is trading at Rs.6,500. A client held TTK till Rs.750, but on my advice about Value of Money and Opportunity cost, he sold.😆 - Govind Parikh.’19

English

Same thing happened with me in goldstone infra (olectra). I bought at 18 rs and after holding for 5 years or so it went to 180 rs and i sold all based on valuations etc etc

After few years another friend of mine who had bought on my suggestion (had invested some 1 lakh at 18 rs) called me and said my broker told me ki aapke stock ka value 1 cr ho gaya hai ab kya karu.. I just laughed and said give it to me 😜

Sometimes forgetting about a stock May be a boon in hindsight.

Sunil Gurjar, CFTe@sunilgurjar01

I bought TTK Prestige at Rs.15, and got chance to meet TT Jagannathan in Banglore, but I skipped it and sold my shares at Rs.200. Today it is trading at Rs.6,500. A client held TTK till Rs.750, but on my advice about Value of Money and Opportunity cost, he sold.😆 - Govind Parikh.’19

English

@WealthLab_ Let’s see I’m happy with even 20% if i actually get it in live trading. Last two months good but need to see consistency

English

@Stockgeeks_in analysis on irb x.com/dhavalp/status…

Dhaval Parikh@dhavalp

🚨 Promoter Buying Disclosures (Open Market) • IRB Infrastructure: Promoter group (IRB Holding) bought 12L shares today (~₹49.8 Cr); ~36L over 3 days (~₹1.48 Cr total) • Orient Ceratech: Promoter group bought 11.6L shares (~₹4.29 Cr) • Jindal Drilling: Promoter group bought ~98.5k shares (~₹4.57 Cr) • Maharashtra Seamless: Promoter group bought 30,185 shares (~₹1.64 Cr) • Premier Polyfilm: Promoter group (D L Millar & Co) bought 1.70L shares (~₹2 Cr) Smaller buys: • Beryl Drugs: 7,500 sh (~₹1.57L) • Clinitech Lab: 2,400 sh • Tiger Logistics: 40k sh • Sacheta Metals: Multiple tranches (~55k+ sh) • Marathon Nextgen Realty: Multiple promoter group purchases (ongoing) • Prataap Snacks, Gem Aromatics, GLEN Industries, etc. Skin in the game = Bullish signal? 📈 #PromoterBuying #IndianStocks #StockMarket

Lietuvių

🔶 Insider Buying & Selling Today👇🏻

👉🏻 IRB Infra

Promoter Group bought total 36,00,000 shares worth ₹14.77 Cr

👉🏻 PG Foils

Promoter Group bought 4,00,000 shares worth ₹8.62 Cr

👉🏻 Mangalam Global Ent

Promoter bought total 40,34,712 shares worth ₹4.65 Cr

👉🏻 Jindal Drilling

Promoter Group bought total 98,500 shares worth ₹4.58 Cr

👉🏻 eClerx Services

Trust bought 29,480 shares worth ₹4.24 Cr

👉🏻 Rain Ind

Promoter bought 4,00,000 shares worth ₹4.15 Cr

👉🏻 Premier Polyfilm

Promoter Group bought 3,40,250 shares worth ₹2.01 Cr

👉🏻 Maharashtra Seamless

Promoter Group bought 30,185 shares worth ₹1.64 Cr

👉🏻 Gem Aromatics

Promoter & Director bought 1,00,000 shares worth ₹1.56 Cr

👉🏻 Savera Ind

Promoters bought total 57,714 shares worth ₹1.01 Cr

👉🏻 Ganesha Ecosphere

Trust bought total 12,376 shares worth ₹98.70 Lakh

👉🏻 Vibhor Steel Tubes

Promoter & Director & Promoter Group bought total 46,178 shares worth ₹50.81 Lakh

👉🏻 Westlife Foodworld

Promoter bought 12,000 shares worth ₹50.36 Lakh

👉🏻 Sinclairs Hotels

Promoter bought 63,000 shares worth ₹45.42 Lakh

👉🏻 Sangam India

Trust bought 10,235 shares worth ₹43.61 Lakh

👉🏻 Glen Industries

Promoter Group bought 45,600 shares worth ₹31.71 Lakh

👉🏻 Sanstar

Promoter Group bought 30,000 shares worth ₹24.17 Lakh

👉🏻 Suprajit Eng

Promoter bought 6,000 shares worth ₹24.07 Lakh

👉🏻 Aerpace Ind

Promoter Group bought 82,001 shares worth ₹20.46 Lakh

👉🏻 Mayur Uniquoters

Promoter bought 3,000 shares worth ₹14.75 Lakh

👉🏻 GEM Enviro

Director bought 40,000 shares worth ₹14.23 Lakh

👉🏻 Mach Conferences

Promoter & Director bought total 10,200 shares worth ₹11.43 Lakh

👉🏻 Resgen

Director bought 20,250 shares worth ₹10.77 Lakh

👉🏻 Tiger Logistics

Promoter Group bought 40,000 shares worth ₹10.49 Lakh

👉🏻 BLB Ltd

Promoter & Director bought 54,514 shares worth ₹8.53 Lakh

👉🏻 Paramount Comm

Promoter & Director bought total 24,724 shares worth ₹8.22 Lakh

👉🏻 Sugs Lloyd

Director bought 7,000 shares worth ₹7.57 Lakh

👉🏻 Whirlpool of India

Designated Person bought 544 shares worth ₹4.75 Lakh

👉🏻 Mudunuru

Director bought 36,115 shares worth ₹4.34 Lakh

👉🏻 Bright Brothers

Promoter bought 2,000 shares worth ₹3.92 Lakh

👉🏻 Signet Ind

Promoter & Director bought total 6,345 shares worth ₹2.79 Lakh

🔻⸻⸻⸻⸻⸻⸻

👉🏻 Anzen India Energy

Other sold total 26,25,000 units worth ₹32.81 Cr

👉🏻 Safari Ind

KMP sold 3,009 shares worth ₹48.20 Lakh

👉🏻 Bartronics India

Promoter sold total 18,08,364 shares worth ₹1.61 Cr

🔁 Like, Bookmark & Repost

#stockmarket

English

@WealthLab_ Its there in the image. Last 2 months real data 10% and rest 10 months backtested data 55% annualized.

English

@bsridhar00 x.com/i/status/20371… just wrote my analysis on irb infra..

Dhaval Parikh@dhavalp

Stock to Study : IRB Infrastructure Developers Ltd (IRB) - Another stock with continuous promoter buying Company Snapshot IRB Infrastructure Developers Ltd is one of India's largest road infrastructure developers and operators, with a strong focus on highways under BOT, TOT, and EPC models. It has a massive portfolio of operational toll roads, InvIT holdings (IRB InvIT Fund), and a shift toward asset-light strategy via monetization and TOT bids. Benefits from government’s highway expansion, NHAI’s TOT pipeline, traffic growth, and InvIT-driven capital recycling. The company is transitioning to a more annuity-like model with long-duration O&M revenues. Guidance & Outlook from Q3 FY26 Concall (Feb 2026) Management was confident on toll growth, asset monetization, and long-term visibility; no major downward revisions: - Toll Revenue: Q3 aggregate toll ₹2,152 Cr (+12% YoY); Q4 expected growth >15–17%; FY27 toll revenue growth ~20%+. - Asset Base: Expanded from ₹80,000 Cr to ₹94,000 Cr; on track to scale to ₹1,40,000 Cr over next 3 years. - Order Book (as of Dec 2025): ₹37,300 Cr (EPC ₹1,600 Cr; O&M ~₹35,000–35,700 Cr providing 10–18 years visibility). - Monetization: Assets worth ₹8,500 Cr monetized in recent period; capital recycled into new projects. - FY26 EPC + O&M Revenue: Guided ~₹3,400 Cr. - O&M Margin: ~20%. - Debt: Consolidated net debt reduced; targeting net debt-free by FY30 through disciplined allocation and monetization. - Q4 FY26: Strong toll momentum expected. - Medium-term: 30% profit CAGR targeted through 2030; focus on TOT segment (market share ~44%), InvIT platforms, and calibrated bidding. Bonus issue 1:1 + interim dividend announced. Valuation Analysis & Projections FY26 Estimates (conservative, based on 9M trends + guidance): - Revenue: ~₹7,500–8,000 Cr (EPC slowdown offset by toll/InvIT). - EBITDA: Strong contribution from toll + O&M. - PAT (before exceptional): Growth trajectory with 14%+ in Q3 pre-exceptional. Implied Multiples at ~₹41.2 (as of 25 Mar 2026): - TTM P/E: ~31x (elevated due to one-offs; forward lower). - EV/EBITDA: Reasonable on toll cash flows. - P/B: ~1.2x (Book Value ~₹33–34). Order-book-to-MCap ratio: Strong visibility (~1.5x MCap on total OB; O&M annuity-like). Compared to road/infra peers (often 15–40x P/E on growth), IRB trades at a discount considering asset-light shift, toll stability, and long O&M book. Analyst consensus target ~₹57–58.5 (range ₹48–72), implying 40%+ upside. Key Positives - Robust toll revenue growth (+12% YoY in Q3) and traffic momentum. - Massive ₹37,300 Cr order book with long-duration O&M annuity (~₹35,000 Cr). - Successful monetization (₹8,500 Cr) and debt reduction; asset base scaling to ₹1.4 lakh Cr. - 1:1 bonus issue + dividends; shift to higher-margin TOT/InvIT model. - 30% profit CAGR ambition through 2030. Key Risks (mitigated but monitor) - EPC revenue weakness and slow ordering environment. - One-off exceptional items impacting reported PAT. - Execution delays in new TOT assets or monetization. - Interest rate sensitivity on debt and traffic volume risks (macro/seasonal). Longer-term: Highway monetization + TOT pipeline + InvIT recycling will drive sustainable 15–20%+ CAGR in cash flows and earnings with improving ROE. Position size accordingly; suitable for infra/annuity-style growth portfolios. Monitor Q4 FY26 toll collections, further TOT wins, and monetization progress closely. Stock Valuation and Projected Price Target : At current valuations (~₹41.2), IRB Infrastructure offers compelling risk-reward as a leading road developer with strong annuity visibility. The combination of robust toll growth, ₹37,300 Cr order book, asset base expansion to ₹1.4 lakh Cr, and debt reduction path justifies a re-rating toward 18–22x forward multiples (target price ₹55–65 over 12–18 months, 35–60%+ upside; analyst consensus ~₹57–58.5 implies ~40% potential, highs up to ₹72). #IRBInfra #StockMarketIndia #Nifty #Investing #StocksToWatch #ShareMarket #Sensex #promoterbuying

English

@bsridhar00 x.com/i/status/20371… just wrote my analysis on irb infra

Dhaval Parikh@dhavalp

Stock to Study : IRB Infrastructure Developers Ltd (IRB) - Another stock with continuous promoter buying Company Snapshot IRB Infrastructure Developers Ltd is one of India's largest road infrastructure developers and operators, with a strong focus on highways under BOT, TOT, and EPC models. It has a massive portfolio of operational toll roads, InvIT holdings (IRB InvIT Fund), and a shift toward asset-light strategy via monetization and TOT bids. Benefits from government’s highway expansion, NHAI’s TOT pipeline, traffic growth, and InvIT-driven capital recycling. The company is transitioning to a more annuity-like model with long-duration O&M revenues. Guidance & Outlook from Q3 FY26 Concall (Feb 2026) Management was confident on toll growth, asset monetization, and long-term visibility; no major downward revisions: - Toll Revenue: Q3 aggregate toll ₹2,152 Cr (+12% YoY); Q4 expected growth >15–17%; FY27 toll revenue growth ~20%+. - Asset Base: Expanded from ₹80,000 Cr to ₹94,000 Cr; on track to scale to ₹1,40,000 Cr over next 3 years. - Order Book (as of Dec 2025): ₹37,300 Cr (EPC ₹1,600 Cr; O&M ~₹35,000–35,700 Cr providing 10–18 years visibility). - Monetization: Assets worth ₹8,500 Cr monetized in recent period; capital recycled into new projects. - FY26 EPC + O&M Revenue: Guided ~₹3,400 Cr. - O&M Margin: ~20%. - Debt: Consolidated net debt reduced; targeting net debt-free by FY30 through disciplined allocation and monetization. - Q4 FY26: Strong toll momentum expected. - Medium-term: 30% profit CAGR targeted through 2030; focus on TOT segment (market share ~44%), InvIT platforms, and calibrated bidding. Bonus issue 1:1 + interim dividend announced. Valuation Analysis & Projections FY26 Estimates (conservative, based on 9M trends + guidance): - Revenue: ~₹7,500–8,000 Cr (EPC slowdown offset by toll/InvIT). - EBITDA: Strong contribution from toll + O&M. - PAT (before exceptional): Growth trajectory with 14%+ in Q3 pre-exceptional. Implied Multiples at ~₹41.2 (as of 25 Mar 2026): - TTM P/E: ~31x (elevated due to one-offs; forward lower). - EV/EBITDA: Reasonable on toll cash flows. - P/B: ~1.2x (Book Value ~₹33–34). Order-book-to-MCap ratio: Strong visibility (~1.5x MCap on total OB; O&M annuity-like). Compared to road/infra peers (often 15–40x P/E on growth), IRB trades at a discount considering asset-light shift, toll stability, and long O&M book. Analyst consensus target ~₹57–58.5 (range ₹48–72), implying 40%+ upside. Key Positives - Robust toll revenue growth (+12% YoY in Q3) and traffic momentum. - Massive ₹37,300 Cr order book with long-duration O&M annuity (~₹35,000 Cr). - Successful monetization (₹8,500 Cr) and debt reduction; asset base scaling to ₹1.4 lakh Cr. - 1:1 bonus issue + dividends; shift to higher-margin TOT/InvIT model. - 30% profit CAGR ambition through 2030. Key Risks (mitigated but monitor) - EPC revenue weakness and slow ordering environment. - One-off exceptional items impacting reported PAT. - Execution delays in new TOT assets or monetization. - Interest rate sensitivity on debt and traffic volume risks (macro/seasonal). Longer-term: Highway monetization + TOT pipeline + InvIT recycling will drive sustainable 15–20%+ CAGR in cash flows and earnings with improving ROE. Position size accordingly; suitable for infra/annuity-style growth portfolios. Monitor Q4 FY26 toll collections, further TOT wins, and monetization progress closely. Stock Valuation and Projected Price Target : At current valuations (~₹41.2), IRB Infrastructure offers compelling risk-reward as a leading road developer with strong annuity visibility. The combination of robust toll growth, ₹37,300 Cr order book, asset base expansion to ₹1.4 lakh Cr, and debt reduction path justifies a re-rating toward 18–22x forward multiples (target price ₹55–65 over 12–18 months, 35–60%+ upside; analyst consensus ~₹57–58.5 implies ~40% potential, highs up to ₹72). #IRBInfra #StockMarketIndia #Nifty #Investing #StocksToWatch #ShareMarket #Sensex #promoterbuying

English

Stock to Study : IRB Infrastructure Developers Ltd (IRB) - Another stock with continuous promoter buying

Company Snapshot

IRB Infrastructure Developers Ltd is one of India's largest road infrastructure developers and operators, with a strong focus on highways under BOT, TOT, and EPC models. It has a massive portfolio of operational toll roads, InvIT holdings (IRB InvIT Fund), and a shift toward asset-light strategy via monetization and TOT bids. Benefits from government’s highway expansion, NHAI’s TOT pipeline, traffic growth, and InvIT-driven capital recycling. The company is transitioning to a more annuity-like model with long-duration O&M revenues.

Guidance & Outlook from Q3 FY26 Concall (Feb 2026)

Management was confident on toll growth, asset monetization, and long-term visibility; no major downward revisions:

- Toll Revenue: Q3 aggregate toll ₹2,152 Cr (+12% YoY); Q4 expected growth >15–17%; FY27 toll revenue growth ~20%+.

- Asset Base: Expanded from ₹80,000 Cr to ₹94,000 Cr; on track to scale to ₹1,40,000 Cr over next 3 years.

- Order Book (as of Dec 2025): ₹37,300 Cr (EPC ₹1,600 Cr; O&M ~₹35,000–35,700 Cr providing 10–18 years visibility).

- Monetization: Assets worth ₹8,500 Cr monetized in recent period; capital recycled into new projects.

- FY26 EPC + O&M Revenue: Guided ~₹3,400 Cr.

- O&M Margin: ~20%.

- Debt: Consolidated net debt reduced; targeting net debt-free by FY30 through disciplined allocation and monetization.

- Q4 FY26: Strong toll momentum expected.

- Medium-term: 30% profit CAGR targeted through 2030; focus on TOT segment (market share ~44%), InvIT platforms, and calibrated bidding. Bonus issue 1:1 + interim dividend announced.

Valuation Analysis & Projections

FY26 Estimates (conservative, based on 9M trends + guidance):

- Revenue: ~₹7,500–8,000 Cr (EPC slowdown offset by toll/InvIT).

- EBITDA: Strong contribution from toll + O&M.

- PAT (before exceptional): Growth trajectory with 14%+ in Q3 pre-exceptional.

Implied Multiples at ~₹41.2 (as of 25 Mar 2026):

- TTM P/E: ~31x (elevated due to one-offs; forward lower).

- EV/EBITDA: Reasonable on toll cash flows.

- P/B: ~1.2x (Book Value ~₹33–34).

Order-book-to-MCap ratio: Strong visibility (~1.5x MCap on total OB; O&M annuity-like). Compared to road/infra peers (often 15–40x P/E on growth), IRB trades at a discount considering asset-light shift, toll stability, and long O&M book. Analyst consensus target ~₹57–58.5 (range ₹48–72), implying 40%+ upside.

Key Positives

- Robust toll revenue growth (+12% YoY in Q3) and traffic momentum.

- Massive ₹37,300 Cr order book with long-duration O&M annuity (~₹35,000 Cr).

- Successful monetization (₹8,500 Cr) and debt reduction; asset base scaling to ₹1.4 lakh Cr.

- 1:1 bonus issue + dividends; shift to higher-margin TOT/InvIT model.

- 30% profit CAGR ambition through 2030.

Key Risks (mitigated but monitor)

- EPC revenue weakness and slow ordering environment.

- One-off exceptional items impacting reported PAT.

- Execution delays in new TOT assets or monetization.

- Interest rate sensitivity on debt and traffic volume risks (macro/seasonal).

Longer-term: Highway monetization + TOT pipeline + InvIT recycling will drive sustainable 15–20%+ CAGR in cash flows and earnings with improving ROE. Position size accordingly; suitable for infra/annuity-style growth portfolios. Monitor Q4 FY26 toll collections, further TOT wins, and monetization progress closely.

Stock Valuation and Projected Price Target :

At current valuations (~₹41.2), IRB Infrastructure offers compelling risk-reward as a leading road developer with strong annuity visibility. The combination of robust toll growth, ₹37,300 Cr order book, asset base expansion to ₹1.4 lakh Cr, and debt reduction path justifies a re-rating toward 18–22x forward multiples (target price ₹55–65 over 12–18 months, 35–60%+ upside; analyst consensus ~₹57–58.5 implies ~40% potential, highs up to ₹72).

#IRBInfra #StockMarketIndia #Nifty #Investing #StocksToWatch #ShareMarket #Sensex #promoterbuying

English

@prsablue Perfect. My momentum ETF tool also has psubees, gold etf and mon100 for current month momentum

English

🚨 #PSUBanks just did what strong stocks do —Bounced from support on HEAVY volumes.

This is not noise. This is a signal.

Signal for the next high probability setups.

Wait & watch for the next setup👇

1️⃣ #UNIONBANK

2️⃣ #MAHANANK

3️⃣ #BANKOFINDIA

4️⃣ #INDIANBANK

#nifty #nifty50 #sensex #stockmarket #banknifty #StocksToWatch #giftnifty #StocksInFocus #stocks #watchlist #investment

Trading Zone@prsablue

4 PSU Banks.All at critical support. 📊One of them bounces hard from here. Which one do YOU think recovers first?👇 1️⃣ #UNIONBANK 2️⃣ #MAHANANK 3️⃣ #BANKOFINDIA 4️⃣ #INDIANBANK #nifty #nifty50 #sensex #stockmarket #banknifty #StocksToWatch #giftnifty #StocksInFocus #stocks #watchlist #investment

English