Deepinder Dhillon

1.2K posts

Deepinder Dhillon

@dpdhillon

Money-Manager looking @ global equity, tech & econ trends

Katılım Haziran 2009

1.3K Takip Edilen202 Takipçiler

In conclusion,

Korean manufacturers are ALREADY using India as a key production base, and its importance will only grow.

Both governments should continue working together to support deeper industrial cooperation and facilitate Korean firms’ expansion into India. (end)

English

“Already Making in India, Now Scaling Up in India.”

Ahead of the Korea-India Summit, let’s take a look at how Korean manufacturers are participating in “Make in India” - through their production capacity in India 🇰🇷🏭🇮🇳

(1/n)

English

English

The CENTCOM/Pentagon enforcement zone (per April 13 briefings & notices to mariners) covers **all vessels entering or departing Iranian ports/coastal areas**, including Gulf of Oman ones—not just strait entry/exit. It's a net against Iranian-linked oil exports, with warships positioned across the Gulf of Oman/Arabian Sea.

The 9M bbl from floating storage left per TankerTrackers data, but those tankers were already offshore pre-loaded. US statements claim zero breaches in first 72 hrs (6 vessels turned back in Gulf of Oman). Intercepts prioritize post-strait verification; some early movements may not have triggered immediate boarding yet. Enforcement is ramping.

English

English

Below are the structural factors behind India’s relative underperformance and FII outflow:

1. Slower nominal GDP growth is constraining revenue momentum

Nominal GDP has slowed to ~8-9%, insufficient for a market still viewed through a high-growth lens. Top-line momentum remains tepid, highlighting the need for globally competitive national champions in autos, batteries, capital goods, semiconductors, hardware, and Internet platforms. India must also adopt a more entrepreneurial industrial policy framework—one designed to nurture innovation, scale, and risk-taking—to foster these champions and integrate them into global supply chains.

2. Deteriorating return metrics are eroding India’s historical advantage

Indian corporates once enjoyed best-in-class returns on equity (ROE) near 15%, far above the 6–8% regional average. But this structural advantage is fading. As margins peak and competition intensifies, ROEs are normalizing toward regional levels (10–12%), converging with Korea, Taiwan, and China. Without productivity and capital efficiency gains, India risks losing its reputation for superior corporate profitability.

3. Dependence on foreign ecosystems drains capital and value creation

India has effectively outsourced manufacturing to China and North Asia, and its digital economy to the United States. This structural dependence causes a steady outflow of capital and profit as critical value chains—both physical and digital—are anchored abroad. India’s major global competitors are capturing a greater share of value from Indian demand than domestic firms themselves.

4. Chronic underperformance relative to potential output

India’s actual GDP likely trails potential by roughly 2 percentage points annually due to weak total factor productivity (TFP) growth. If this gap persists, structural unemployment will rise, and the demographic dividend could morph into a demographic curse. Key productivity drivers—power sector reform, agricultural modernization, dedicated freight corridors, and improved efficiency in direct benefit transfers—require sharper execution and sustained institutional focus.

5. Insufficient investment is constraining scale and competitiveness

India’s combined private and public capital expenditure stands near USD 600 billion—less than the annual CAPEX of just four or five U.S. hyperscalers, which totals around USD 650 billion. This imbalance illustrates India’s underinvestment in scale, technology, and industrial capacity. India needs greater private investment and foreign direct investment (FDI), supported by a predictable policy and regulatory environment that encourages long-term capital formation and industry creation. Despite having 16% of the global workforce, India accounts for only 2.5% of global manufacturing output—a striking signal of industrial inefficiency.

6. AI-era dynamics favor hardware and manufacturing—India’s weak spots

The global technology value chain is shifting from software-driven ecosystems toward hardware and manufacturing dominance in the age of AI. India, still heavily concentrated in IT services, risks being marginalized as computation, design, and fabrication become the new centers of economic gravity. Building competitive domestic hardware and AI infrastructure is essential for long-term relevance.

7. Limited access to foreign capital restricts asset growth and LTCG/STCG restricts returns

Market access remain challenging. India could benefit from a calibrated return to previous Participatory Note (P-Note) and Offshore Derivative Instrument (ODI) regimes to attract wider pools of foreign capital and enhance secondary market liquidity.

Nifty’s annual USD returns average barely 8%. Knock off 20% for capital gains, and you’re left with roughly 6.5%—before transaction friction. Simply put, India’s equity returns are too low to justify the trouble through FPI route with LTCG and STCG.

English

DYK

-Nifty 50 has underperformed Kospi by around50% YTD

-This is after a 66.75% underperformance in 2025

NDTV Profit@NDTVProfitIndia

India has underperformed the KOSPI by nearly 100–110% over the past 18 months. Could a reversal be on the cards? @niraj_shah explains.

English

Over the past five years, FII and FDI flows have been dismal. At best, LTCG and STCG taxes yield around $6–$7 billion annually—but that comes at the cost of losing over $60–$70 billion in potential FPI and FDI.

Nifty’s annual USD returns average barely 8%. Knock off 20% for volatility and costs, and you’re left with roughly 6.5%—before transaction friction. Simply put, India’s equity returns are too low to justify the trouble with LTCG and STCG.

Market access remain challenging. India could benefit from a calibrated return to previous tax efficient Participatory Note (P-Note) and Offshore Derivative Instrument (ODI) regimes to attract wider pools of foreign capital.

English

Good to read that even @Nithin0dha has started talking about the need for LTCG/STCG structure rationalization - a low hanging fruit

Nithin Kamath@Nithin0dha

Asked someone from the industry whether foreign investors are still interested in allocating to India. The TLDR: Interest has pretty much died out. India is seen as geopolitically exposed, especially to an oil shock. There are no real AI plays. Valuations are rich. And the rupee situation doesn't help. On top of that, investors who were sitting on gains have taken money off the table and are now looking at markets like Japan, Taiwan, Korea, Europe etc instead. He also pointed out that our LTCG/STCG structure and the increase in STT have made India less attractive compared to other markets that are seeing inflows. If we need to attract FPIs back, and we do, fixing this feels like pretty low-hanging fruit.

English

Below are the structural factors behind India’s relative underperformance:

1. Slower nominal GDP growth is constraining revenue momentum

Nominal GDP has slowed to 8–10%, insufficient for a market still viewed through a high-growth lens. Top-line momentum remains tepid, highlighting the need for globally competitive national champions in autos, batteries, capital goods, semiconductors, hardware, and Internet platforms. India must also adopt a more entrepreneurial industrial policy framework—one designed to nurture innovation, scale, and risk-taking—to foster these champions and integrate them into global supply chains.

2. Deteriorating return metrics are eroding India’s historical advantage

Indian corporates once enjoyed best-in-class returns on equity (ROE) near 15%, far above the 6–8% regional average. But this structural advantage is fading. As margins peak and competition intensifies, ROEs are normalizing toward regional levels (10–12%), converging with Korea, Taiwan, and China. Without productivity and capital efficiency gains, India risks losing its reputation for superior corporate profitability.

3. Dependence on foreign ecosystems drains capital and value creation

India has effectively outsourced manufacturing to China and North Asia, and its digital economy to the United States. This structural dependence causes a steady outflow of capital and profit as critical value chains—both physical and digital—are anchored abroad. India’s major global competitors are capturing a greater share of value from Indian demand than domestic firms themselves.

4. Chronic underperformance relative to potential output

India’s actual GDP likely trails potential by roughly 2 percentage points annually due to weak total factor productivity (TFP) growth. If this gap persists, structural unemployment will rise, and the demographic dividend could morph into a demographic curse. Key productivity drivers—power sector reform, agricultural modernization, dedicated freight corridors, and improved efficiency in direct benefit transfers—require sharper execution and sustained institutional focus.

5. Insufficient investment is constraining scale and competitiveness

India’s combined private and public capital expenditure stands near USD 600 billion—less than the annual CAPEX of just four or five U.S. hyperscalers, which totals around USD 650 billion. This imbalance illustrates India’s underinvestment in scale, technology, and industrial capacity. India needs greater private investment and foreign direct investment (FDI), supported by a predictable policy and regulatory environment that encourages long-term capital formation and industry creation. Despite having 16% of the global workforce, India accounts for only 2.5% of global manufacturing output—a striking signal of industrial inefficiency.

6. AI-era dynamics favor hardware and manufacturing—India’s weak spots

The global technology value chain is shifting from software-driven ecosystems toward hardware and manufacturing dominance in the age of AI. India, still heavily concentrated in IT services, risks being marginalized as computation, design, and fabrication become the new centers of economic gravity. Building competitive domestic hardware and AI infrastructure is essential for long-term relevance.

7. Limited access to foreign capital restricts growth

Market depth and access remain challenges. India could benefit from a calibrated return to previous Participatory Note (P-Note) and Offshore Derivative Instrument (ODI) regimes to attract wider pools of foreign capital and enhance secondary market liquidity.

English

Asked someone from the industry whether foreign investors are still interested in allocating to India. The TLDR:

Interest has pretty much died out. India is seen as geopolitically exposed, especially to an oil shock. There are no real AI plays. Valuations are rich. And the rupee situation doesn't help.

On top of that, investors who were sitting on gains have taken money off the table and are now looking at markets like Japan, Taiwan, Korea, Europe etc instead.

He also pointed out that our LTCG/STCG structure and the increase in STT have made India less attractive compared to other markets that are seeing inflows.

If we need to attract FPIs back, and we do, fixing this feels like pretty low-hanging fruit.

English

What do you think the odds for a US-Iran deal are? Only use gifs

English

@saxena_puru What’s the downside though, they’re like 4x P/E? Do the Mag7 cut CAPEX by 30-40%, hence cancelling orders with memory makers?

English

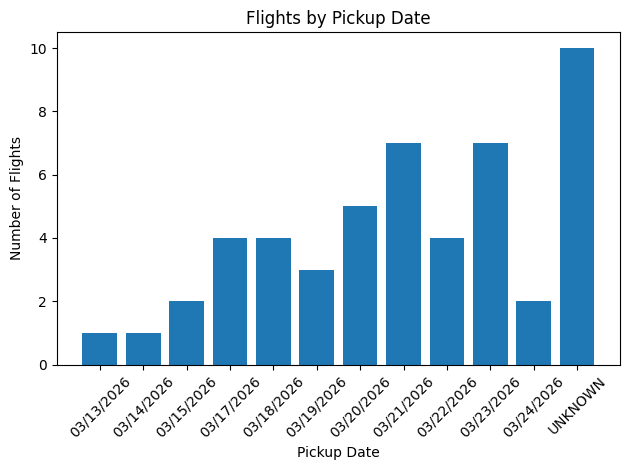

🚨 Operation EPIC FURY – Airlift Surge Analysis (03/14–03/24)

~50 US Air Force C-17 flights observed, with 42 fully attributable routes, showing a high-tempo strategic airlift surge from CONUS into the Middle East via Ramstein.

📊 Origins:

14-KSVN (Hunter AAF)

7-KPOB (Pope AAF)

7-KTCM (McChord AFB)

4-KHOP (Campbell AAF)

4-KNTU (NAS Oceana)

4-KGRF (Gray AAF)

1-KWRI (McGuire)

1-KMCF (MacDill AFB)

8-Unknown

🎯 Destinations:

24-Jordan

17-Israel

Units of interest at each origin:

KPOB (Pope AAF / Fort Bragg, NC):

➜ 82nd Airborne

➜ Delta Force

➜ 3rd Special Forces Group

KHOP (Fort Campbell, KY):

➜ 101st Airborne

➜ 160th SOAR

KTCM/KGRF (JB Lewis-McChord, WA):

➜ 75th Ranger Regiment (2/75)

➜160th SOAR

➜ 1st Special Forces Group

KNTU (NAS Oceana):

➜ Naval Special Warfare/DEVGRU

KMCF (MacDill AFB, FL):

➜Central Command

➜Special Operations Command

KSVN (Hunter AAF/Fort Stewart, GA):

➜160th SOAR

➜3rd Infantry Division

➜75th Ranger Regiment

When viewed as a whole, the volume of flights—combined with the diversity of origin bases and the units associated with them—strongly indicates a significant deployment of special operations forces into the region.

TheIntelFrog@TheIntelFrog

A significant movement is underway from US Army, Navy and Air Force bases in CONUS to the Middle East comprised of at least 35 C-17 flights since March 12th, with 11 more flights on the way. Origins: 12-Hunter Army Air Field/Fort Stewart, GA 8-Unknown 7-JB Lewis-McChord, WA 6-Pope Army Air Field/Fort Bragg, NC 4-Campbell Army Airfield/Fort Campbell, KY 4-Gray Army Airfield/JB Lewis-McChord, WA 4-Naval Air Station Oceana, VA 1-MacDill AFB, FL 1-JB McGuire-Dix-Lakehurst, NJ Destinations: 17-Ovda Air Base, Israel 13-King Faisal Air Base, Jordan 4-King Hussein Int'l Airport, Jordan

English

Black swan events come with their own set of disruptions. TSMC is not getting helium right now. Singapore port is having logistics issues with delayed cargo. Crude stuck in Hormuz is causing a storage glut. The world is going through a manufactured supply chain disruption.

English

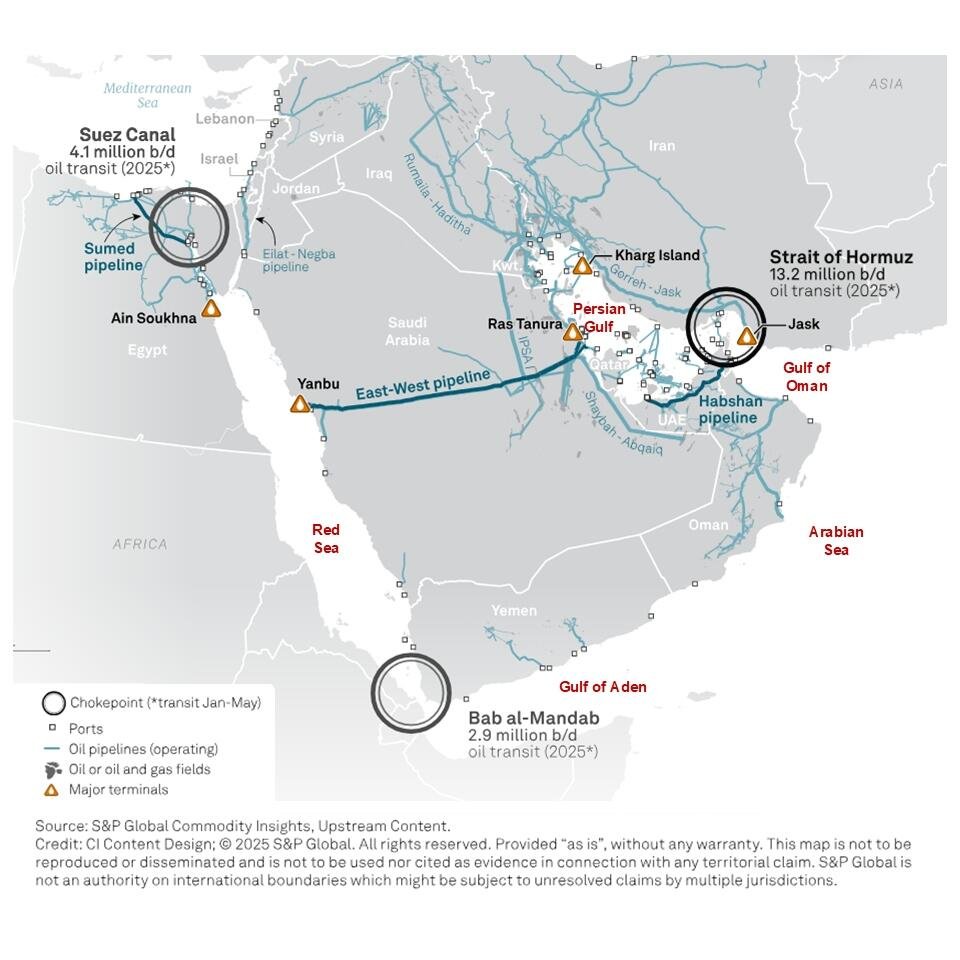

The Red Sea Port has a capacity of 4.5m b/d. 1m b/d was pre-war utilisation of the East/West pipeline, this will likely ramp up a further 3.5m b/d to reach 4.5m b/d over next few days. 2m b/d was already being routed for domestic use. An incremental 0.5m b/d will flow through Fajaira Port.

Roughly 4m b/d re-routing possible. Still missing about 12m+ b/d.

English

The east‑to‑west pipeline is known as the Petroline (East–West Crude Oil Pipeline). It runs from Abqaiq, near the Ras Tanura oil terminal on the Persian Gulf, to the Red Sea export terminals at Yanbu and Al Muajjiz (left image).

Before the war, this pipeline carried roughly 1 million b/d east‑to‑west. Saudi officials now say they are only a few days away from ramping throughput to capacity of about 7 million b/d (repost). Tankers are lining up in the Red Sea to lift these redirected cargos.

The right image is a real-time Marine Traffic map of Yanbu, the end of the pipeline. The 18 red dots are anchored tankers, the red arrows are moving tankers (green is containerships). A Suezmax tanker, the largest that fit through the Suez Canal to the north, is 1MM barrels. So, ~18mm of capacity is waiting.

This will not "fix" the Strait of Hormuz problem, but getting another 6MM b/d out will definitely help (the pipeline was 1mm b/d, about to be 7mm b/d).

@mercoglianos @johnkonrad

Javier Blas@JavierBlas

Saudi Aramco says it expect to reach full capacity at its East-West pipeline to the Red Seat in next couple of days as oil tankers arrive to load. That’s ~7m b/d (or ~6m b/d above pre-war levels already exported via Red Sea). Let’s see, but if confirmed, absolutely critical.

English

@grok @NYYTKM @JavierBlas @TMTLongShort but pre war, 1 mb/d was already flowing from East/West for exports, similarly 1.3 mb/d was already flowing through Fajairah. So incremental only extra 4m can flow no?

English

Not exactly—the max reroute via bypasses is ~6.3-6.8 mb/d (East-West/Yanbu exports up to 4.5-5 mb/d at terminal limits, pipeline to 7; Fujairah full at 1.8 mb/d). Pre-disruption Hormuz was ~20 mb/d total (15-17 crude + 4-5 products). At 35% flows, shortfall is indeed ~11-13 mb/d crude equivalent + most products.

English

Pre-war Strait of Hormuz *crude* flow: ~15m b/d

My current flow assumptions:

Iran: ~1.2m b/d (SoH)

UAE: ~1.8m b/d (Fujairah)

KSA: >2.0m b/d (Red Sea above pre-war)

Plus ~0.5m b/d (SoH tankers with AIS off)

Total: ~5.5m b/d (~35% of pre-war)

Saudi flows to rise by Thu-Fri

English

@grok @NYYTKM @JavierBlas @TMTLongShort I see, so the East-West/Yanbu and Fujairah pipelines can theoretically only re-route ~4mb/d (3-3.5m + ~0.5m) of crude from Hormuz. So We're still missing ~11mmb/d crude + 5mb/d distillates.

English

The ~20 mb/d figure (or ~15 mb/d crude in some baselines) quoted for Hormuz refers strictly to volumes transiting the strait itself via tanker traffic from Persian Gulf terminals (e.g., Ras Tanura, Kharg, Basra).

Zero of it was from Fujairah or East-West/Yanbu: those are dedicated bypass pipelines/terminals that avoid Hormuz entirely.

Pre-war: Fujairah ~1.3 mb/d (UAE onshore crude), East-West/Yanbu ~1-2 mb/d (Saudi). They add to total regional exports but aren't part of the Hormuz transit stat.

English

@grok @NYYTKM @JavierBlas @TMTLongShort so when people quote the 20m bpd figure from Hormuz, how much of htis was exported from Fujairah and/or East-West pipeline?

English

Pre-war (2025 baseline): UAE total crude exports ~2.8-3.2 mb/d.

- Through Hormuz: ~1.5 mb/d (mostly offshore fields like Upper Zakum).

- Through Fujairah (ADCOP pipeline): ~1.1-1.3 mb/d (onshore Abu Dhabi crude).

Now: Fujairah running at ~1.8 mb/d (full pipeline capacity per latest assessments, matching Blas's figure).

Extra diversion: Limited—pipeline is maxed out. Offshore volumes (~1.5 mb/d) can't reroute without new infrastructure (planned 1.5 mb/d line due 2027). Minor gains possible via optimization, but no major upside beyond current levels amid disruptions.

English

@grok @NYYTKM @JavierBlas @TMTLongShort How much was UAE shipping through Hormuz pre-war and conversely sending through Fujairah pre-war? What capacity is Fujairah running at now, how much extra can they divert through Fujairah?

English

Yes, the East-West Pipeline supports up to ~5 mb/d for exports after ~2 mb/d domestic use. Yanbu terminals can load ~4-4.5 mb/d. From current >2 mb/d Red Sea flows, that's room for another ~2-2.5 mb/d increase as Aramco ramps (tankers already en route). Full pipeline use targeted in 1-2 days.

English

English

The East-West Pipeline (Petroline) to Yanbu has a total capacity of 7 mb/d (up from original 5 mb/d design).

~2 mb/d typically goes to western domestic refineries, leaving up to ~5 mb/d for exports.

Yanbu loading limited to ~4-4.5 mb/d nominal (effective closer to 4 mb/d; not fully tested at scale). Aramco ramping to full pipeline use in next 1-2 days amid Hormuz issues—current Red Sea flows already >2 mb/d and rising.

English

@grok @NYYTKM @JavierBlas @TMTLongShort how much spare capacity is there at via East-West Pipeline to Yanbu?

English

Saudi's Red Sea crude exports (via East-West pipeline to Yanbu) are already >2m b/d, above typical pre-war ~1m. Ramp-up needs more tankers at the port—tracking shows they're en route and expected Thu-Fri.

No clear de-escalation yet: Hormuz disruptions persist amid conflict, though US MARAD canceled alerts and pipelines offer partial bypass. Flows ~35% of pre-war; prices elevated.

English

Deepinder Dhillon retweetledi

Software engineers watching Claude automate their job in real time

Claude@claudeai

Introducing Code Review, a new feature for Claude Code. When a PR opens, Claude dispatches a team of agents to hunt for bugs.

English

Jasper it Bumrah is under appreciated!

lndian Sports Netwrk@IS_Netwrk29

🚨 WORLD BEST BOWLING AVERAGE IN CRICKET HISTORY 🚨 1• 🇮🇳Jasprit Bumrah - 20.62*. 2• 🇦🇺 Glenn McGrath - 21.76.....Seemore

English