Sabitlenmiş Tweet

Retweet if you think SILVER is the most precious thing in the world after other living beings.

English

End_Share 🇦🇺

14K posts

@end_share

Protecting Australian silver miners from foreign theft. In particular the 122m oz Maronan deposit. My Federal Court case https://t.co/ZeGmI4eNE5

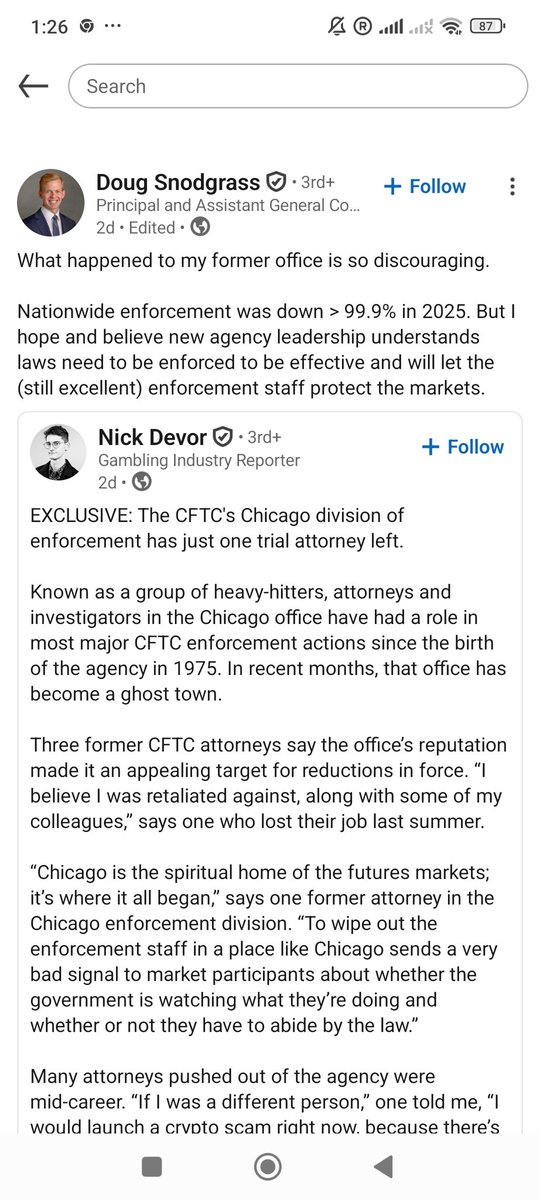

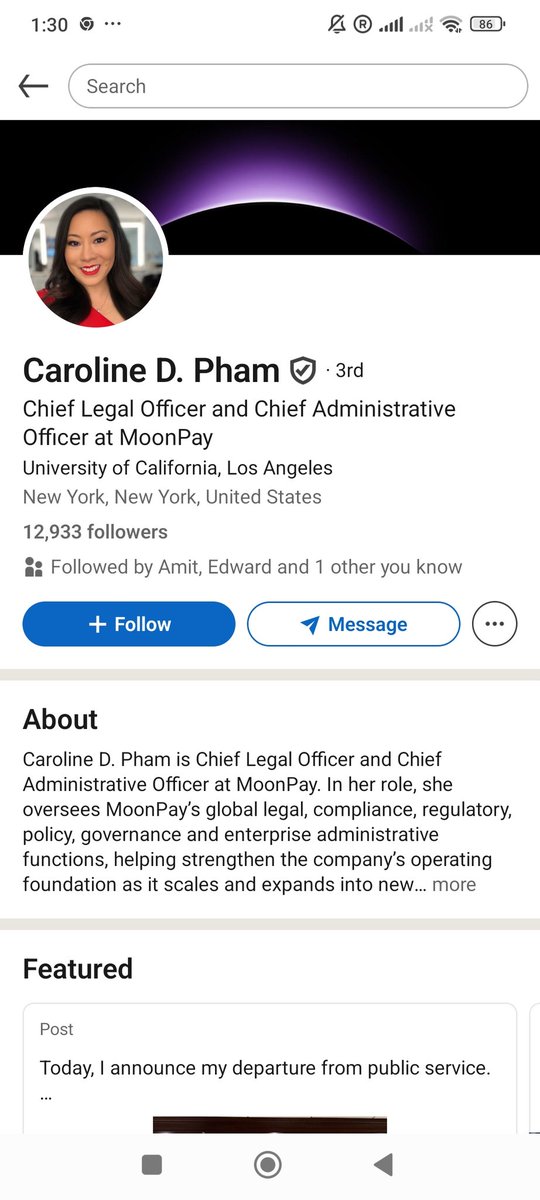

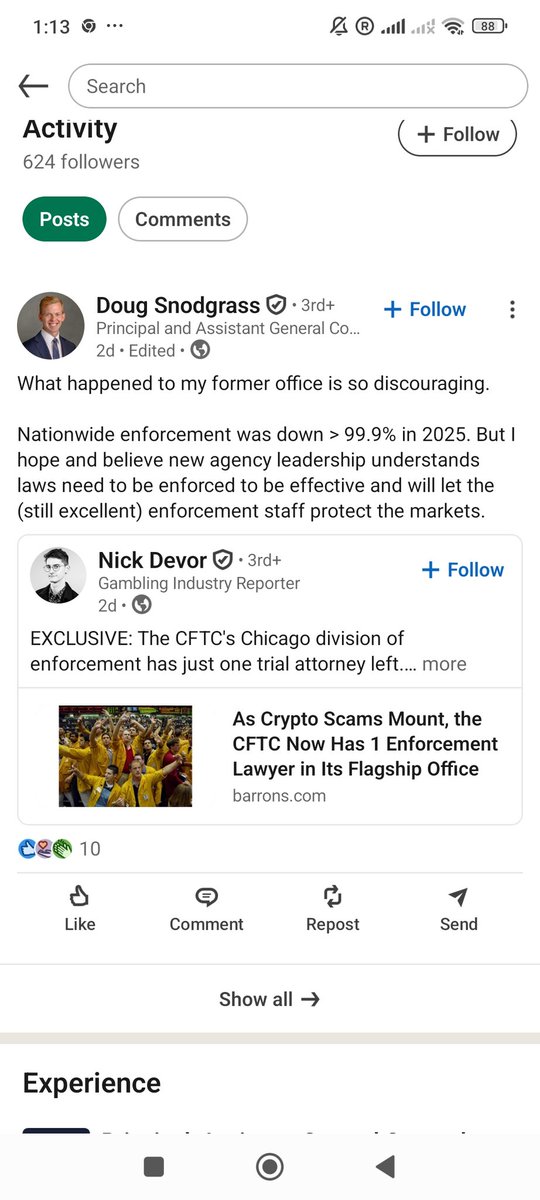

Hey sweetheart - @CarolineDPham Is this correct there was 99.9% less enforcement action while you were Chairman of the CFTC? @PeterRHann1 @BossBlunts1 @davidbateman @WVerily @DavidLe76335983 @oriental_ghost @TheMetalCharts @DonDurrett @KingKong9888 @MakeGoldGreat @realTimHack

The contrast between exchange/supervisory actions in Shanghai and Chicago is so stark - and scary. 17 suspensions of members at Shanghai Futures Exchange to 'close only' status and revised silver delivery priorities to exclude unhedged speculators. No circuit breakers at all at CME in violation of their own rules, but also no investigation because CFTC now has ZERO enforcement lawyers in the Chicago office (normally 20). Trade at your own risk! barrons.com/articles/predi…

The contrast between exchange/supervisory actions in Shanghai and Chicago is so stark - and scary. 17 suspensions of members at Shanghai Futures Exchange to 'close only' status and revised silver delivery priorities to exclude unhedged speculators. No circuit breakers at all at CME in violation of their own rules, but also no investigation because CFTC now has ZERO enforcement lawyers in the Chicago office (normally 20). Trade at your own risk! barrons.com/articles/predi…

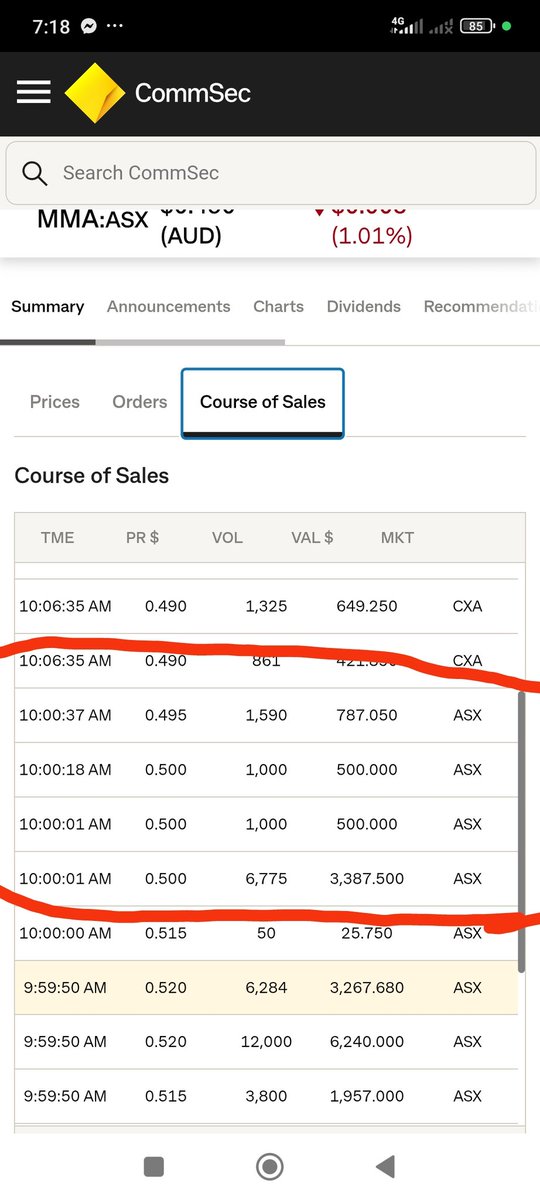

In case you wonder why the price of silver suddenly crashed without a reason or even volumes, clearly as a result of sophisticated spoofing, is because at the current price the banks can arbitrage the $SLV now trading at heavy discount to extract physical to cover naked shorts 👇🏻

Bian Ximing naked shorts on silver at the SHFE are just the tip of the iceberg. People broadly don't think what he describes here can happen because "never happened" to silver, but anyone paying attention to the data can hear them screaming that this can happen at any moment.

Here is the full explanation of how the biggest exploit in the history of precious metals likely unfolded 👇🏻 Comex futures price settlement at the Comex is based on a VWAP between 13:24 to 13:25EST LBMA price settlement instead happens at 12:00 UK time Most of Silver OTC contracts settle using the LBMA reference and many OTC contracts expire into month end. On the 30th Jan LBMA silver price benchmark settled at 103.19$ while the Comex Benchmark a few hours later settled at 78.29$. The following chart (credit @KingKong9888 ) is a great representation of how bullion banks hedge and transact in the silver market (both paper and physical). It is an open secret now how many banks and brokers were under water on their silver positions, gold and other precious metals especially after the rally in January. Beware this flow chart roughly applies to all these metals that all crashed on Friday (not silver alone). What’s even more remarkable is how precocious metals crashed on Friday in isolation, stocks, bonds and other commodities were totally unaffected. Anyone that understands any basic of macro and markets knows how this is logically wrong. Let’s add one more piece to the puzzle now: on Friday the OI at the Comex decreased by 8k contracts at the end of the day. Assuming for simplicity the price differential between the LBMA and the Comex as a reference. That means banks were able to extract ~1bn$ gain from their shorts pushing the Comex price through the floor after the LBMA settlement. Furthermore the $SLV continued trading after the LBMA benchmark settlement creating almost a 20% discount to NAV because of that. Here is the other trick the banks pulled. If you have to settle a lot of physical contracts at the LBMA but you don’t have the metal, because of such a discount to NAV, AP banks could buy $SLV shares in the open market from panic selling investors, tender the shares to claim bars at 103.19$ and make a killing in the process. Not surprisingly, $SLV shares count increased by ~51m shared from Thursday to Friday according to iShares. Because of the NAV discount banks extracted up to 1.5bn$ of profits exploiting this ETF assuming they bought up all that shares differential and then turned around to claim silver bars at a much higher price for contract settlement purposes (keep an eye on the data on the metals redemption from the ETF). The last piece of the puzzle is the exploit against Leveraged silver ETFs like $AGQ that have been forced into liquidating a vast number of derivative contracts during the crash. Here brokers made a killing too, but other people here on X already covered this matter well so no need for me to say more. All in all, it’s fair to estimate how banks and brokers made up to 5bn$ of profits (or lowered their pre existing losses depending on how you look at it) orchestrating one of the biggest price manipulation in the history to abnormally crash the price of silver in a single day. Surely they made more if you consider the same dynamics happened on gold platinum and palladium. However this left the precious metals market in a massive price dislocation not only between physical and paper, but also across financial products and exchanges. Trading resumes in less than 24 hours and there is a chance that what’s about to happen is going to be even more historic than Friday’s events because China and India won’t stop buying silver because of the severe industrial shortage they are dealing with.