@croreclub Appreciate the group .

The learning and interaction is commendable

Specially the regulations

English

𝔸𝕪𝕦𝕤𝕙 𝔾𝕠𝕪𝕒𝕝

1.4K posts

@equityayush

Equity Aashiq / Traveller & Explorer / Sarcastic /Market Research #SME & #PreIPO #FOMO se DUR Unearthing listed & unlisted opportunitites

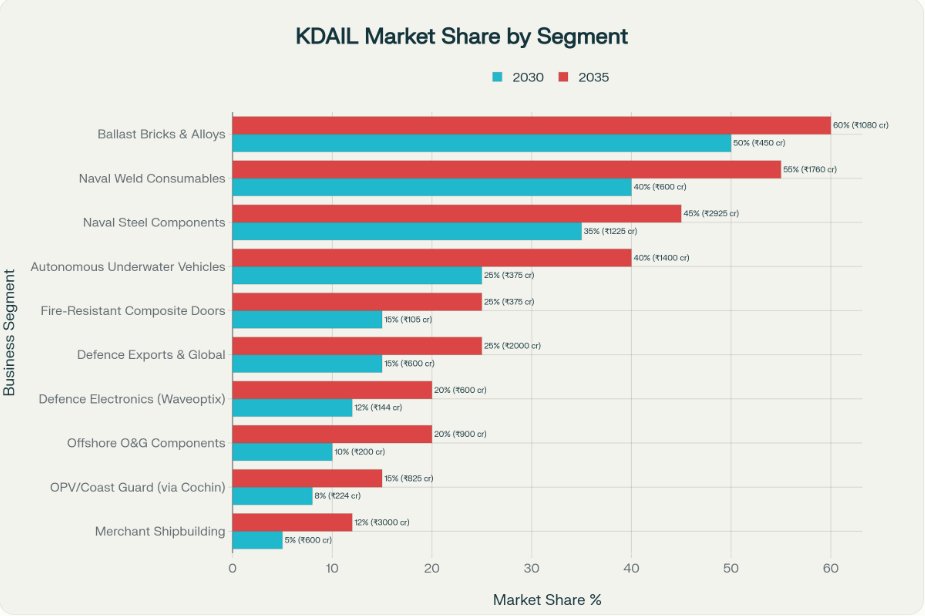

Naval #shipbuilding Process flow map I had created a month ago SMEs and large caps in the image are for illustrative purposes, not recommendation #KrishnaDefence #RappidValves #CFFFLuid #shreerefrigerations #GRSE / #GRSEL #MazagonDock #mdl #CochinShipyard (and shared on Linkedin: linkedin.com/posts/siddhart…)

Sugs Lloyd Limited SME IPO Closing Today Applying 👍 Company is an Electrical Transmission and Distribution (46% Revenue), Solar EPC (43% Revenue) and India's Largest Manufacturer Of Fault Passage Indicators (FPIs) Company Raising 85.6 Cr, Majorly for Working Capital, the backcalculation suggests approx 70-80% growth Hence priced at roughly 10.5× FY26 Company has started operations in Transmission and also bidded for Battery Energy Storage Systems (BESS) The Fault Passage Indicator (FPI) is an unique product in which it competes with Schneider and Siemens (This equipment is used to easily locate faults in Electrical lines used by Discoms and Private utilities, company was the Pioneer in bringing loop automation and FPIs in India); Company claims 50%+ market share in India Clientele : BREDA, NTPC, TATA Power, DPHC, Indian Railways, Multiple State Discoms, Etc. Promoter quality is strong, Good sectors and outlook, Attractive Valuations Good thing to note is the Company and Promoters have no pending legal Litigations, Tax matters which is rare In these businesses Has a management interaction (Posting the interview above this post); The management is seeing no issues on the trade Recievables Part Few risks include Client Concentration, Some stretched working capital and Dependance on Government Sad to see that the company opting for SME IPO, could have easily came in Mainboard in next 6 months

Siemens Energy India Ltd- Going to List on 19th June-Mainboard Investors should looking for opportunity in Siemens If the listing is not hot. ▶️Siemens received the National Company Law Tribunal (NCLT) 's approval for the demerger of the company and Siemens Energy India Ltd. ▶️The equity allotment ratio for this demerger was fixed as 1:1, which means that Siemens shareholders will get one equity share each of Siemens Energy India for every one share that they own as of the record date. ▶️The record date to determine the allotment eligibility was fixed as April 7, 2025. ▶️Expected listing range ₹2,995 – ₹3,711 :Jefferies ▶️Siemens to demerge the ENERGY division as SIEMENS ENERGY INDIA LTD ▶️Siemens Energy is core OEM for transformers, switchgear & HV infra. ▶️Siemens Energy booked Rs 5,100 crore worth of orders, nearly 60% of its FY24 total. It ended March with an order book of Rs 15,100 crore, nearly 2.4 times its FY24 revenue. ▶️Siemens is also doubling its power transformer capacity through a Rs 460 crore capex, signaling confidence in future demand. ▶️Siemens Energy should be a key beneficiary of the over $100 billion transmission capex pipeline. Current margins reflect less than 60% utilisation at its T&D facilities ▶️Largest Power T&D Player in India ▶️Mcap to exceed $10 Bn – ahead of Hitachi & GE Vernova ▶️Hitachi Energy PE (Mar-27E): 66x ▶️GE Vernova T&D PE (Mar-27E): 54x ▶️Jefferies assigns Siemens Energy 60x PE → Target: ₹3,350 (55x Mar-27E EP #Echobox=1750252453" target="_blank" rel="nofollow noopener">financialexpress.com/market/siemens…

#InformationalPurposes #DYDD #NoRecommendation #NotInvested