Paras Defence is exactly the kind of company that looks too small to matter right up until you actually read the numbers.

This is Day 9/100 of Decoding the Defence Sector

For FY26, they reported about ₹478 crore in revenue and roughly ₹88 to ₹90 crore in profit. That is not public sector scale and it is not supposed to be. The company lives in a completely different part of the map spanning space optics, defense electronics, heavy engineering and electromagnetic pulse protection solutions. They sell capability, not volume.

Look at their structure today in May 2026. This is one of the few Indian players building indigenous submarine periscopes, hyper spectral cameras for space and turnkey EMP protection. Those are not brochure items. They are mission critical components where failure gets people fired. Qualification cycles are long and replacement options are limited. That creates a moat built entirely on who else can actually do this.

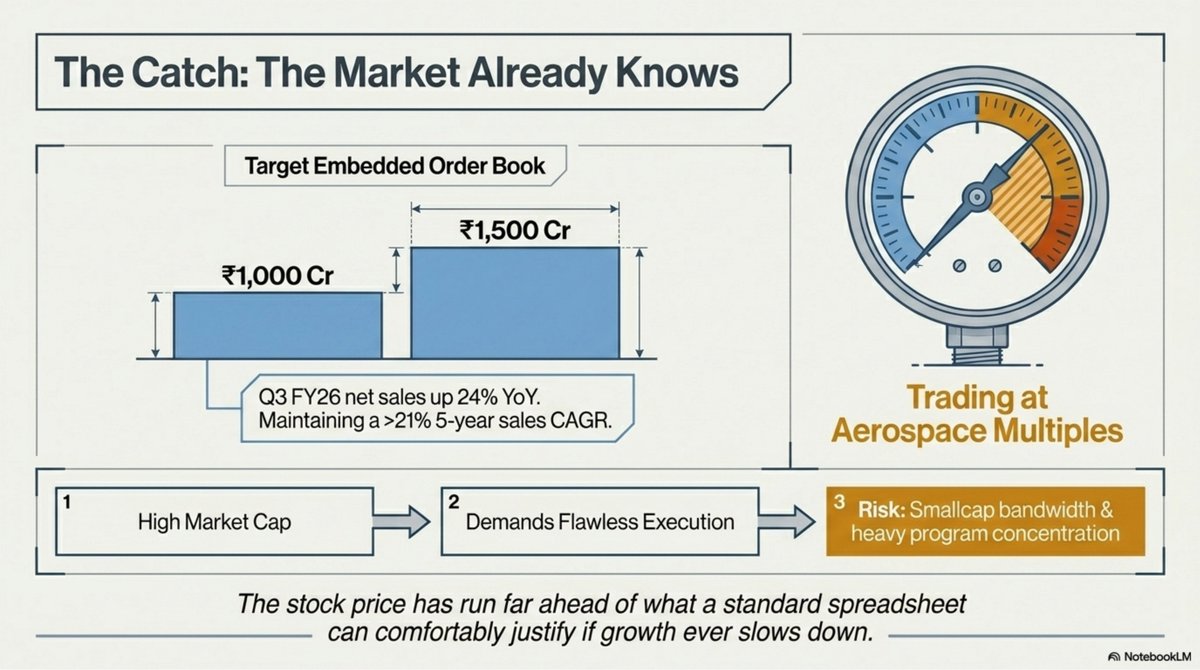

The Q3 FY26 results showed net sales of ₹106.35 crore, up 24% YoY. That full year revenue run rate implies a business scaling aggressively while staying profitable. Management guides the order book to eventually cross ₹1,000 crore. For a sub ₹500 crore revenue base, that is serious embedded demand, not just hope.

But here is the catch. The markets already know this. At a market cap above ₹5,000 crore, Paras screens as very expensive, with some trackers slapping a sell label purely on valuation. That does not make it a bad business. It just means the stock price moved ahead of what a spreadsheet can justify if growth ever slows.

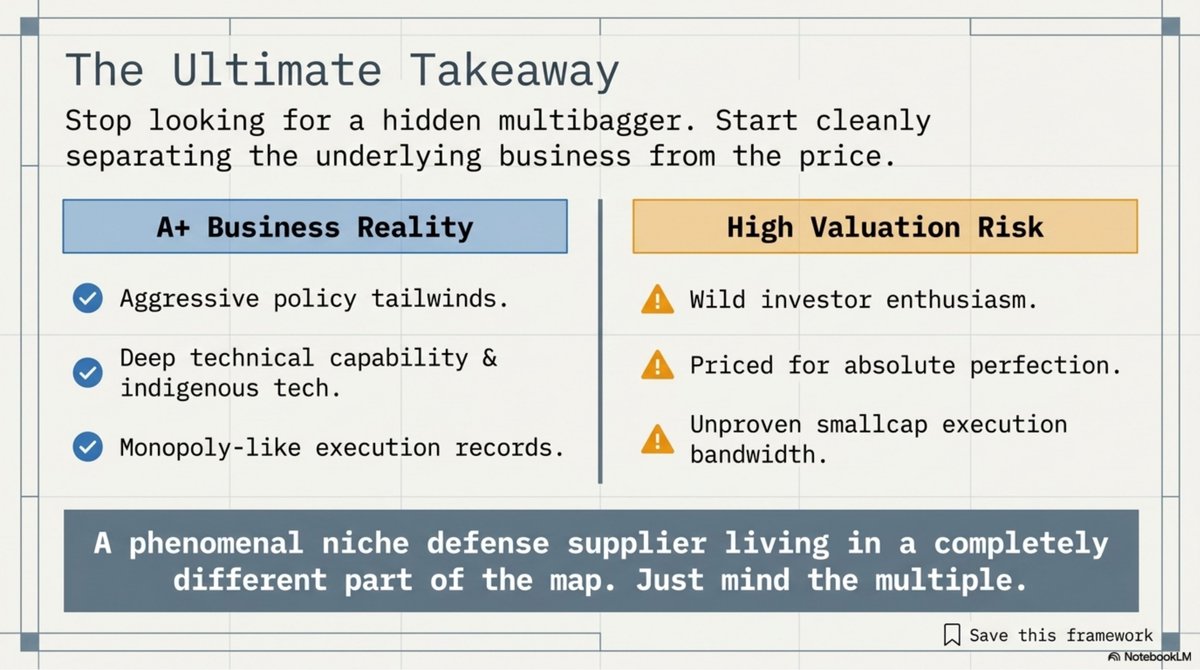

Although Paras sits at a brilliant intersection. The state wants self reliance, DRDO wants domestic partners and foreign OEMs refuse to hand over crown jewel tech. That tension pushes work toward specialized firms with demonstrated execution. The risk is not relevance. The risk is investors paying aerospace multiples for a company still holding smallcap execution bandwidth and heavy program concentration.

Yes, Paras is a small company, but the logic around it is massive. This is exactly what a niche defense supplier looks like when policy tailwinds, technical depth and investor enthusiasm collide. Your job is to separate the business quality from the multiple.

Found this interesting? Follow @equitydecode for more such insights.

Join our Community Channel for FREE on WhatsApp:

whatsapp.com/channel/0029Vb…

Check my deep dives on various topics on Substack.

spicapitalresearch.substack.com

Also if you are on insta (of course you are), Follow me on Insta.

instagram.com/spicapitalrese…

Note: This is not investment advice. Please consult a SEBI-registered financial advisor before making any investment decisions.

#Substack #Finance #Valuation #Invest #Money

English