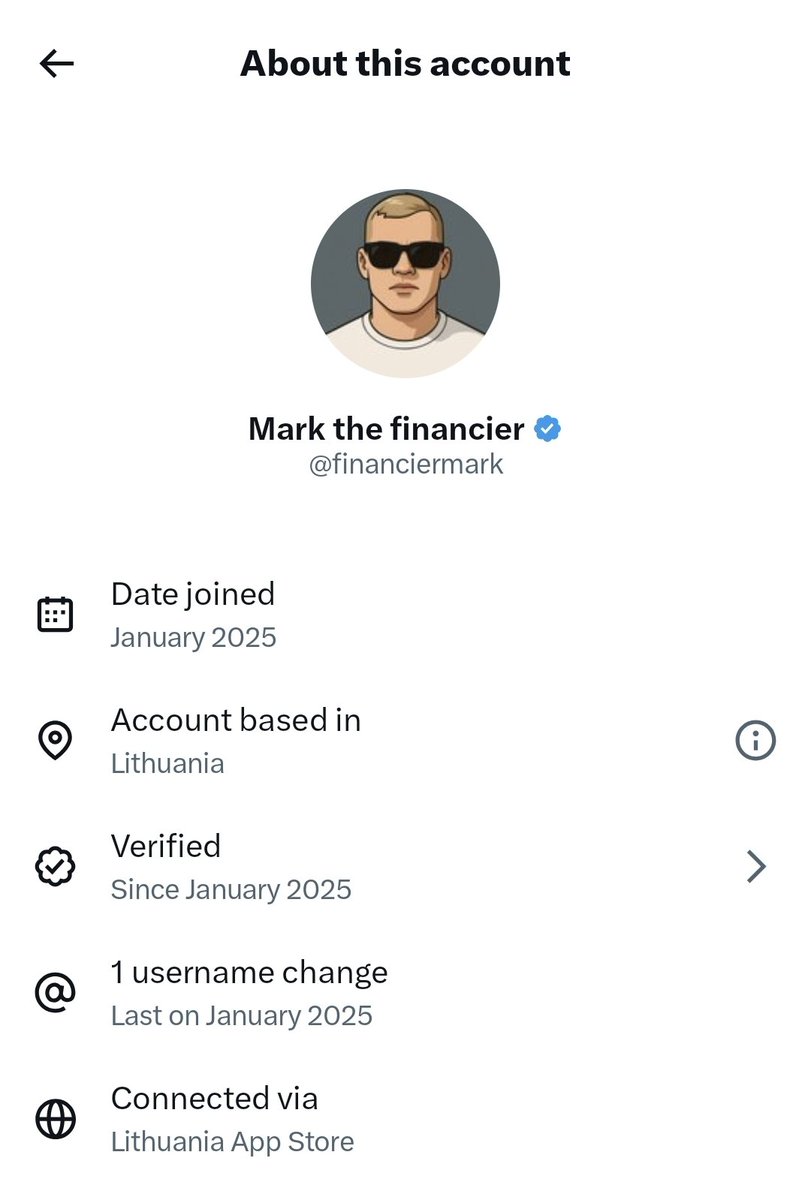

Mark the financier

708 posts

Mark the financier

@financiermark

Tracking global flows, sentiment & liquidity shifts. Macro-driven equity investor | Sharing real-time personal thesis.

Katılım Ocak 2025

1K Takip Edilen2.2K Takipçiler

The Dollar💲 Index's threat of breaching its decade-long channel is concerning.

Major levels below are shown and must hold; otherwise, an inflationary spike won't be the only near term concern.

2007 saw a weakening Dollar Index before the GFC hit.

Nevertheless, it still remains in the safe zone, but something to consider moving forward.

Tuti manete.

English

Japan is learning the hard way that you cannot print your way out of a debt wall once the rest of the world stops playing along.

Prime Minister Takaichi entered office selling the Sanaenomics dream. Massive fiscal expansion. Tax cuts. Growth through confidence. The market’s response was an immediate and violent no.

By pushing food tax cuts with no credible funding source, she did not stimulate demand. She triggered a sovereign risk premium. Investors are no longer debating growth. They are pricing credibility.

The bond market is the canary in the coal mine, and it is screaming. Yields are rising not because of optimism, but because trust is eroding.

Japan is now trapped. If rates rise to defend the yen, the debt loaded economy breaks. If rates stay low, the yen keeps collapsing and imports become unaffordable. Energy, food, and essentials get repriced overnight.

There are no good moves left. Only a decision about which disaster arrives first.

English

We’re seeing yields drop beautifully, especially on the short end. That’s the important part. Bills are getting bid hard. Not because of a pivot, not because of QE, but because money is choosing safety.

The long end is drifting lower too, but it’s still elevated, and that’s completely normal in this environment. Every major economy has a solvency problem, including the US. Long-term promises are not trusted when debt loads are this high and deficits are structural.

So the logic is simple. Why lock money away for 10 or 20 years when you’re getting almost the same yield in T-bills with none of the duration risk? You can roll short-term paper, stay liquid, and reassess as the system tightens.

And this is where it gets important. Money flowing into the T-bill short end pushes those yields down. Every percentage point lower means the US can roll its debt cheaper. That directly reduces the interest burden of servicing the deficit. That’s the objective.

This is not theory anymore. It’s visible in real time. Liquidity is draining from risk markets. Global capital is rotating into US debt at a steady, healthy pace. No panic. No force. Just capital doing exactly what rational capital does when trust disappears elsewhere.

English

The unwind we've seen so far is tiny. We're talking about decades of cheap Yen that funded everything from US tech stocks to emerging market debt. Japan defending the Yen by dumping Treasuries is painful now, but it forces the margin call later. When that levered money implodes, the flight to safety will dwarf Japan's selling.

English

@financiermark carry trade been unwinding for some time already? And JP mainly responsible for the present dump, how they gonna suppress yields, by raising rates? Their bigger worry and priority is Yen dump

English

To understand the strategy, you have to look at the liability side of the U.S. balance sheet. The U.S. sits on a $7 trillion "debt wall" that needs to be refinanced in the very near future.

Here is the math: If the Treasury tries to refinance that debt at current market rates (5%+), interest payments will consume the entire federal budget. It’s fiscal suicide. They need those rates to be 2% or 3%.

But they can't just print money to lower rates (QE) because that would destroy the dollar and reignite inflation. So, they are left with only one option: Fear.

You have to engineer a global environment so terrifying that foreign capital voluntarily accepts 2% yields just to keep their principal safe. The U.S. isn't trying to "fix" the global economy right now. They are creating the specific conditions where the world forces U.S. yields down for them.

Kevin Gordon@KevRGordon

Btw the 3m-10y Treasury yield spread closed at its highest since October 2022

English

They don't need to suppress the medium term. They are waiting for Japan to do it for them.

The entire setup is a trap for the carry trade. High U.S. yields break the Yen -> forced global selling -> massive capital flight into USTs. The moment the carry trade unwinds, the bond market gets the bid the Fed is refusing to provide. It’s a controlled demolition.

English

@financiermark well 1-3 m is almost 1:1 FFR, ie the only thing at Fed's control. and afaik only 20% of their debt is <1y. So not sure how exactly they gonna suppress even the medium term

Whereas even 6m-2y yield pumping noticeably across the globe. Honestly, seems a further los-lose for bonds

English

This move makes total sense in the current setup. Nobody wants to commit capital for ten or thirty years when fiscal pressure is rising globally, so the long end blows out. But once investors step out of those trades, they still need safety and yield. And right now the cleanest place to get both is the US short end. You can roll three or six month bills and avoid duration risk entirely. The auctions this week confirmed that foreign buyers see it the same way. So yes, yields are rising everywhere, but the capital is actually drifting back into the dollar system, which is exactly what the US positioned for.

English

@financiermark and how's that working? esp with JGB yields breaking out. Rates growing substantially over the last month globally - all over the curve

English

**DOLLAR INDEX**💵

Below 98.80 and 96.50 comes into play.

English

@2KsAdamSilver @SpencerHakimian The one year chart shows strong demand on the short end. Yields got crushed. So I genuinely don’t know what point you think you’re making.

English

@financiermark @SpencerHakimian Global capital ISNT piling into Treasuries, that's why bond yields are high. Because the government has to entice investors more with a higher return. You're not a financier, you're a Trump zombie on a troll account with a worm in his brain

English

Do they know that higher bond returns mean a worse economy?

Treasury Department@USTreasury

U.S. Treasuries are having their best year since 2020, and the investors who had confidence and faith in President Trump’s economic policies have been richly rewarded. Never bet against @POTUS or America! 🇺🇸

English

GIF

QME

Talking all things bonds & global employment this evening ⬇️

2 year yield can’t wait for some policy errors in 2026… YCC happening under Trump by end of term is a real possibility.

English

People keep treating the debt size as the core problem, but that’s not how the system works. The real issue is the percentage you refinance it at. When demand for Treasuries is strong and yields move lower, the US gets access to cheap capital again, which is exactly what you need to restart growth. In my view there still has to be a sharp correction at some point because that’s what pulls even more capital into the bond market and drives yields toward something like two percent. That’s the path to making the refinancing wall manageable.

English

@financiermark @SpencerHakimian It means the economy is stalling, in other words. It also means our national debt is sky rocketing. Over 2 trillion more since Trump took over.

English

@GarethSoloway If Japan starts unwinding carry, that’s the ignition point the US is waiting for. It drains global leverage, triggers the risk off move, and pushes safe haven demand straight into US paper. The unwind hurts equities, not the Treasury market.

English

Japanese 10 year yields continue to inch toward 2%. At what point does money parked in the U.S. return to Japan? The Yen Carry trade continues to be something that could suck major liquidity out of U.S. markets.

English

Today’s auctions came in strong. Heavy bidding, real foreign appetite, everything clearing without a hint of stress. And the funny part is how fast the narrative flipped. Not long ago everyone was shouting sell America, warning that nobody would touch U.S. debt. Now foreign buyers are stepping in aggressively, treating it as the most reliable place to park capital. This kind of demand only happens when the world has made up its mind about where safety actually is.

English

We have never seen TLT this heavily shorted. It shows how confident investors are in the higher yield narrative. The problem is that stretched positioning often becomes unstable under stress. Once the market shifts into risk off mode, Treasuries catch the flows instantly and shorts become liquidity. That is how you get a reversal that feels abrupt and far larger than fundamentals alone would justify.

Subu Trade@SubuTrade

$TLT short interest is at a new RECORD high:

English

Everyone already knows the data is bad right now. The job market is weakening, inflation is ticking up, and the overall picture isn’t pretty. But weak data would tell the world the US is slipping first, which is the opposite of the strategy. The goal is to hold steady until another major economy cracks. Japan is the obvious candidate given its debt load and failing currency. The US needs that moment to pull in global capital and drive yields lower.

English

🚨BREAKING: US 3Q GDP REPORT CANCELED

That’s because Trump DESTROYED the economy.

English

This data isn’t great, I agree. But you’re ignoring the cost structure behind it. Factory building is debt financed, and right now, US debt is insanely expensive because of high yields. You don’t rebuild the industrial base with expensive money. You wait for global stress to trigger the flight into Treasuries, yields fall, capital becomes cheap again, and then you rebuild. Everything right now is inflated and overleveraged. A reset is part of the process.

English

@FrankBnOC @SpencerHakimian I’m pointing to the part of reality that actually determines the US future. The debt and the refinancing cost are the central issue. The separation from China naturally creates short-term hits, but it’s necessary.

English

@financiermark @SpencerHakimian I’m not zoomed in on trade noise, I’m paying attention to the reality what is happening. It’s seems like you are ignoring it

English