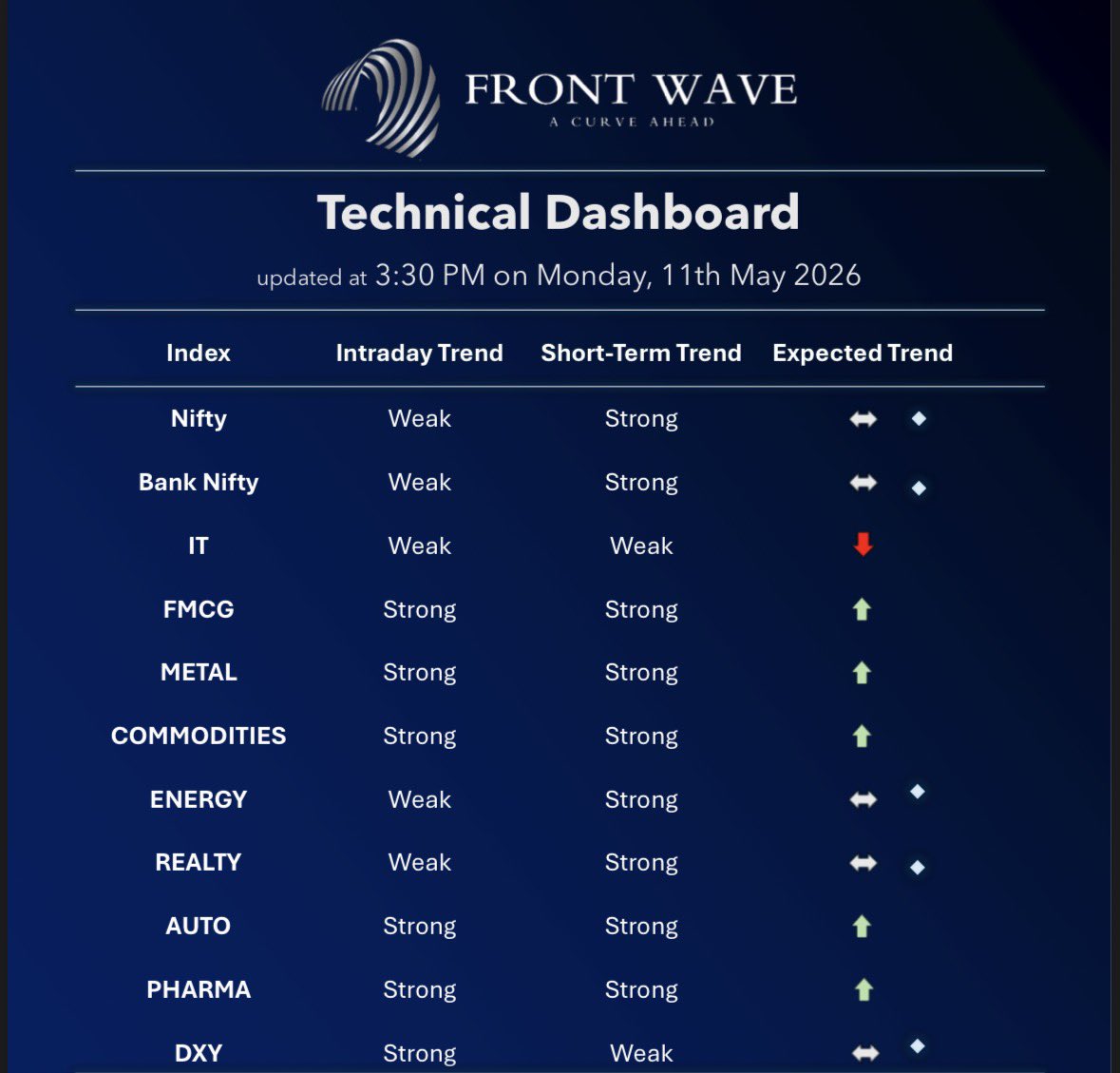

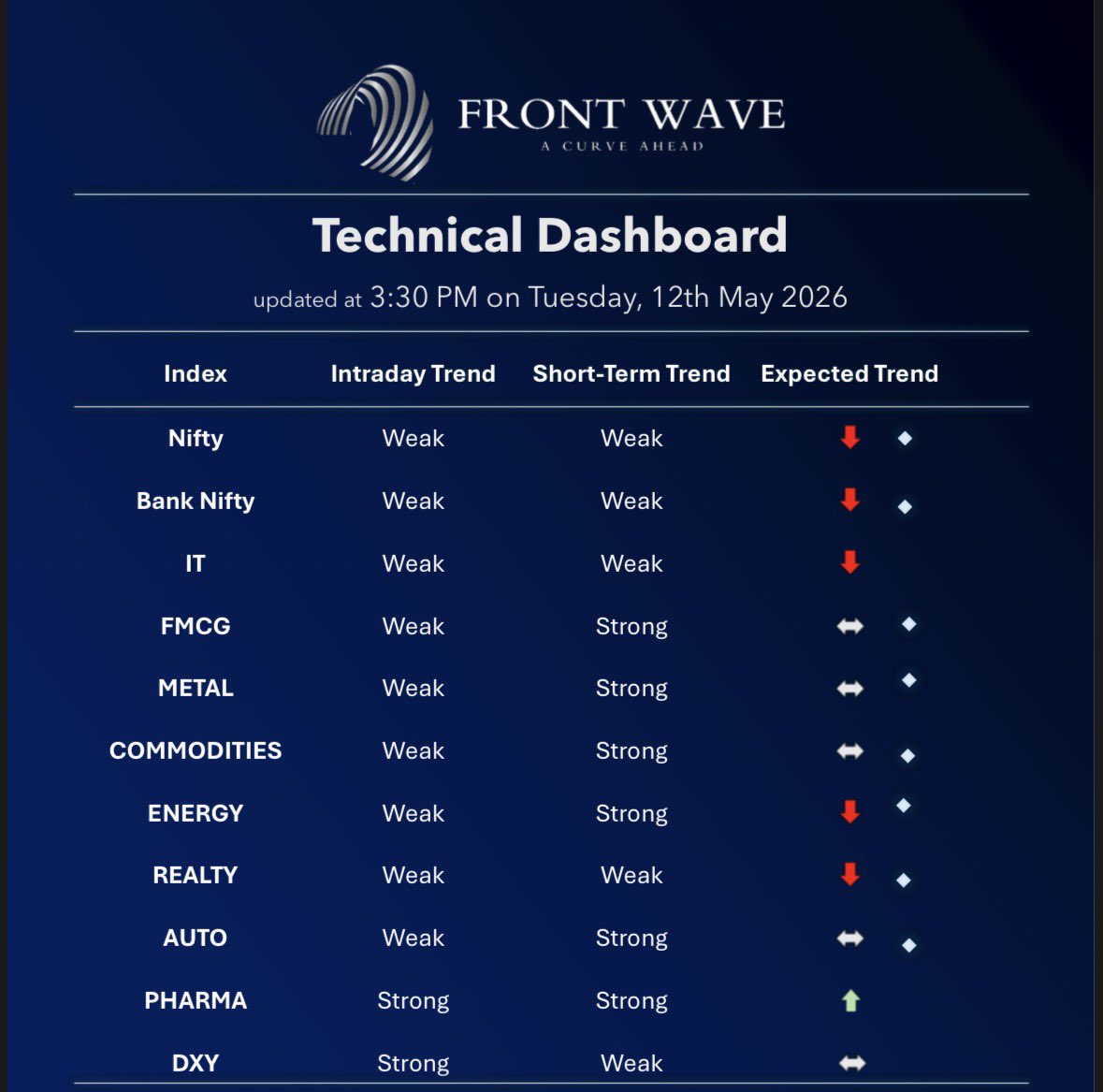

📰 Front Wave Market Insights - 12th May 2026

⚠️ NIFTY downgraded to Weak – Stay Cautious!

The market structure has deteriorated rapidly.

Over the last few sessions, we’ve gone from a strong momentum setup to broad downgrades across the dashboard — and that shift is now clearly visible.

📊 Dashboard Updates:

🔻 Nifty → Weak

🔻 Bank Nifty, Realty, Energy → Weak; Most other indices → Neutral

This is no longer a “buy the dip” environment.

🌍 Macro Pressure:

🛢 Oil near $100 continues to weigh heavily on markets and sentiment.

💡 Strategy:

• Stay cautious

• Cut weak longs / respect stop losses

• Avoid aggressive dip buying

For now, the trend remains negative and we take it day by day until the dashboard turns green again.

📉 In this phase:

Sell on rises, preserve capital, wait for the next clean setup.

English