Sabitlenmiş Tweet

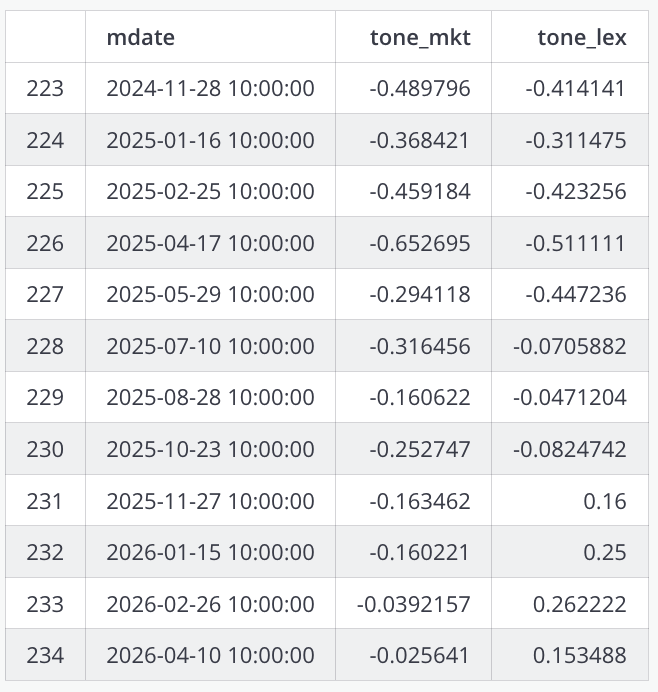

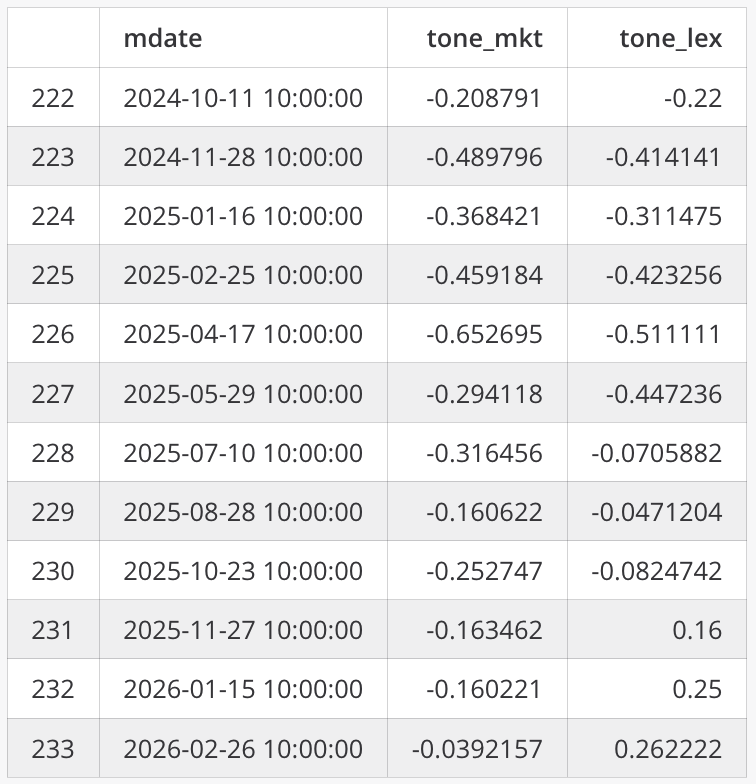

#BoK rate-decision minutes sentimental score (Apr 2026)

- tone_lex down turn

- expect BoK rate unchanged to next decision.

English

hedgedworld

6.7K posts

@hedgedworld

SemiConduct/AI/TechStock&Review, Financial Instrument, QuantTrade&Invest, CryptoCurrency, HFT and ETC. CFA holder. Opinions are my own.

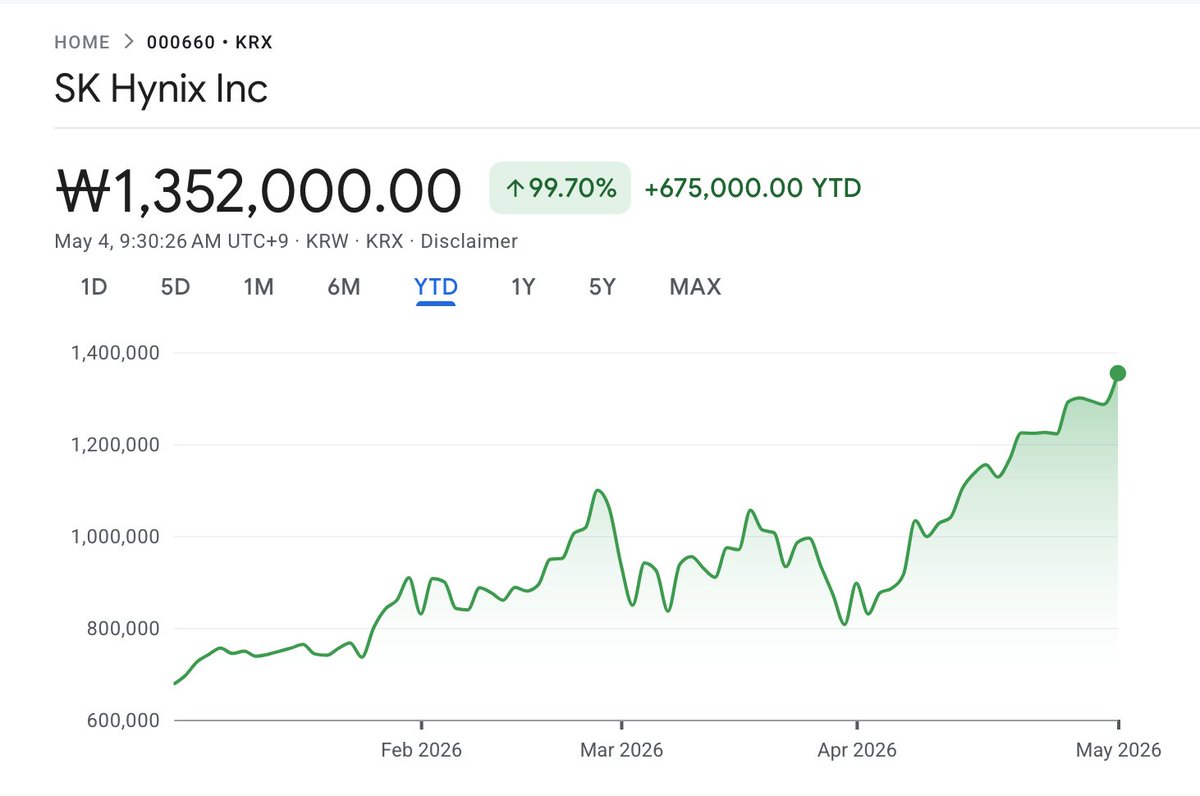

Even with a significant rally last year, SK Hynix has doubled its share again YTD (as of this morning). YTD now is outperforming Samsung Electronics, which was not the case earlier this year.

because we are in the second great academia exodus/ brain drain or of our time the first one started in the 90s when all the smartest people started going into finance the second one just began. now everyone is running to the AI labs

John Ternus faces critical decisions on iPhone pricing and US manufacturing – FT 9to5mac.com/2026/04/29/joh… by @benlovejoy

🏎️ Most automakers build cars. These two control supply Most cluster together, but Tesla and Ferrari don’t. $RACE: caps supply → pricing power $TSLA: future constraints → implied pricing power Most automakers scale units. These two don’t.

You think the AI bottleneck is HBM. You think it’s CoWoS. You think it’s GB200 cables or 800G optics or the Arizona power grid. You are looking at the wrong layer of the stack. The bottleneck is … nicotine. Specifically, the ESSE Change 1mg menthol cigarette made by KT&G (033780.KS) and smoked by Samsung’s HBM packaging engineers in the courtyard of Pyeongtaek Campus P3 between 2:47 AM and 3:04 AM during the third reflow shift. Without this cigarette, Samsung HBM4 yields collapse from 64% to 11%. Nobody knows why. I think I cracked it. I ran a backtest on Samsung’s HBM3 qualification ramp pulling weekly yield disclosures from FSS DART filings, normalizing to a 7-day baseline, and cross-referencing against KT&G’s quarterly shipment manifests at the SKU × distribution-center level. R² of 0.87 on HBM3, with ESSE Change 1mg shipments to the Pyeongtaek-Anseong corridor leading yield prints by 36–40 hours. I assumed I’d messed up the merge. Ran it three more ways. The signal held. So I pulled HBM4E, which Samsung started disclosing weekly in Q1 2026. Same overlay, but this time narrowed to CU branch #4471 which is 340 meters from the P3 fab gate, the only 24-hour store within walking distance of the third-shift smoking area. R² = 0.91, lag of 38 hours, p < 0.001. When I ran SK hynix yields against the same KT&G series, no signal. Samsung yields against Marlboro shipments via Philip Morris Korea, no signal. Every other CU branch within 2km of P3 nothing. Only #4471 prints. This upcoming June, Samsung is qualifying HBM4E for Nvidia Feynman. Samsung supplies ~30% of HBM4E into the ramp or 1.2M Feynman packages, every single one of those HBM stacks is gated by an engineer puffing on an ESSE Change. Samsung HBM4E yield is now the load-bearing dependency for global AI capex, but KT&G is the load-bearing dependency for Samsung. And sadly there is no alternative. Japan Tobacco’s Mevius is described by Samsung engineers as “tasting like a hospital.” Marlboro is what SK hynix smokes and for engineering reasons is structurally incompatible with Samsung’s MR-MUF process. BAT and Imperial have under 4% combined Korean share, and Chinese domestics can’t be imported in volume. Even KT&G’s own ESSE Special Gold was trialed at P3 in March 2025 and caused a 7% yield drop in one week because the engineers said they could taste the paper supplier change and were feeling nauseous. With all that said, look at the financials. ESSE Change runs ~38% gross margin against a 52% group average. KT&G has been underpricing their flagship brand for two decades because nobody realized it isn’t a cigarette, it’s the bottleneck of global AI capex. A 15% price hike is ~80% lift to operating income at this volume, lifting group EBITDA margin from 28% to 34%. On ₩6.1T of revenue, that’s ₩370B of incremental operating profit against a ₩9.8T market cap resulting in a 12% earnings beat from one SKU repricing. And the best part? The engineers literally cannot decline, because there is no substitute. I bet on two hikes in eighteen months which gets you 25% EPS growth without selling a single additional pack. This is what the sell-side is going to figure out in Q3, and it’s why the multiple goes from 9× to 22× before consensus catches up to the revisions. No amount of Arizona engineers chewing 30mg mint Zyns replaces this. KT&G has a lockdown on the engineers who make the world’s HBM. They can name their price.

An old way of boosting parametric yield: bin splits tomshardware.com/pc-components/…

$POET 太刺激了 现在没有了 $MRVL 大客户,而且是以这种违反 NDA 的方式失去客户,未来不好说。 建议朋友们最近先不要碰,别去赌反弹。 这家公司我在元旦期间推荐过,但后来越看越不对劲,我个人做过一段时间的波点后清掉了,问了一位光通信领域的大佬后,也就彻底不碰了 在群里说过,有兴趣的朋友可以联系我进群哦。