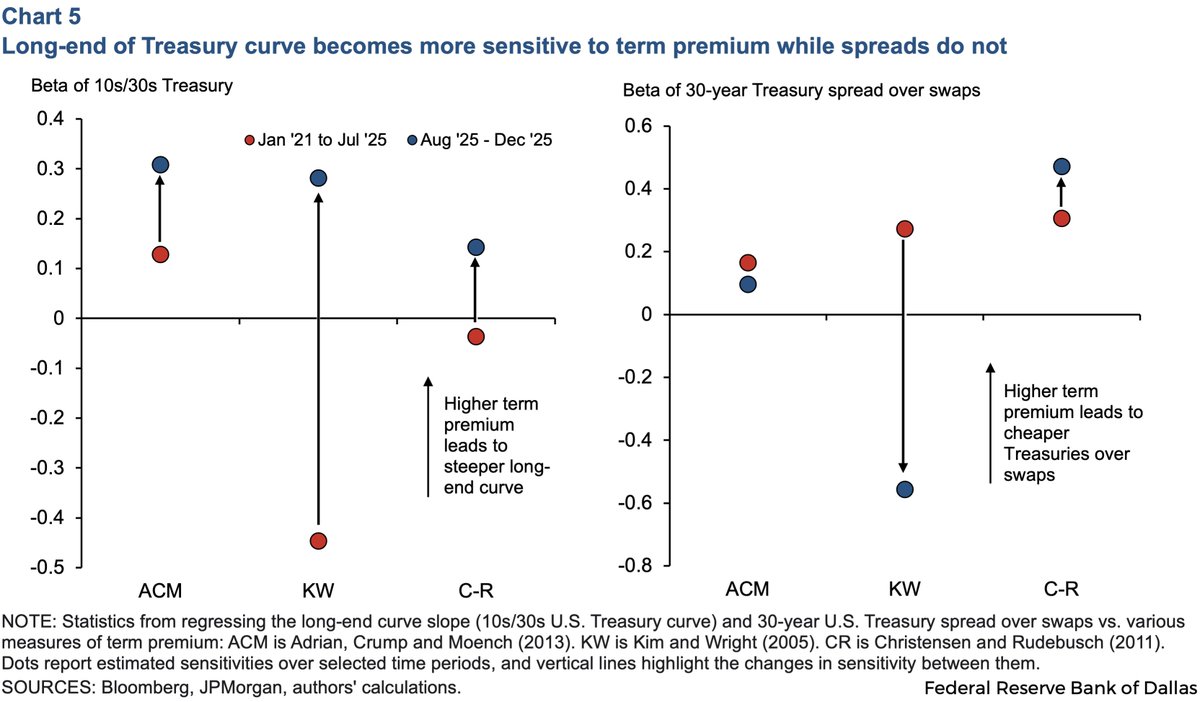

Going forward, if this type of flow from AI financing grows, the long end of the curve and long-maturity swap spreads may diverge from their historical relationship.

English

Hugodevere

1.1K posts

@hugodevere

Student of the game. Views my own.

The rapid unwinding of positions of the Treasury cash-futures basis trade amplified market stress in 2020, and the large and leveraged trade has only grown since. A new report from researchers at the Dallas Fed analyzes its ability to handle future shocks. dallasfed.org/research/econo…