Sabitlenmiş Tweet

j_dlo_g

9.6K posts

j_dlo_g

@j_dlo_g

Me recuerdas a mí cuando era gilipollas.

Katılım Aralık 2012

552 Takip Edilen80 Takipçiler

j_dlo_g retweetledi

Recordemos siempre esto.

El "listo". Catalán, buena familia, futbolista-empresario, visionario, MBA, charlas TED. Hundió la Copa Davis tras tirar por la borda un contrato de 25 años. Reventó Agora APP en concurso de acreedores con 8,6 millones evaporados. Cerró Kerad Games en pérdidas. Lo de las hamburguesas premium, cerrado. El restaurante gourmet, ni un año abierto. La Kings League, pinchando. Vendió la Supercopa a Arabia. Multado por la CNMV por información privilegiada. Y por el camino perdió a la madre de sus hijos por la camarera de La Traviesa.

Y luego está el "tonto" sevillano. El futbolista sin luces, ese al que imitaban en la tele como el paleto del sur, el andaluz que habla bruto. Pues el "tonto", a sus 40, acaba de comprar por 450 millones el club que lo formó en la cantera, para sacarlo del agujero en el que otros lo metieron. No es Warren Buffett el de Camas, pero ahí está, casado con Pilar Rubio y con cuatro niños como cuatro soles.

Y esto no va de sur contra norte. Yo no soy Manu Sánchez dándose golpecitos de andaluz en el pecho mientras mama de la PSOE. Esto va de que ya toca jubilar el cuento ese de que hablar con acento catalán es hablar culto, que un MBA garantiza un cerebro, y que el resto de España son vacas y panderetas. Somos un país, no el decorado del Eixample. Y resulta que en Camas también saben hacer cuentas.

Olé tus cojones, @SergioRamos.

ᴍᴀɴᴜ.@ESnomanu

Al final Piqué que era el listo, consiguió arruinar la Copa Davis y Sergio Ramos que era el tonto va a ser propietario del club de su vida.

Español

j_dlo_g retweetledi

Están usando a Chaves (caso ERE) como revulsivo electoral.

No sé si sois conscientes de que esto es como si sale Bárcenas a hacer campaña por el PP. Imagináoslo por un momento.

Ese es el marco con el que juega el PSOE.

PSOE de Málaga@PSOEmalaga

🔴 Juanma Moreno utilizó ayer la muerte de dos guardias civiles y el accidente de Adamuz. 🚫 Su moderación es pura impostura. 📰 +INFO 👉 f.mtr.cool/amuwqiztdb

Español

j_dlo_g retweetledi

Boomer entrando a la App del Santander para meter 5k€ en bonos del tesoro.

Español

j_dlo_g retweetledi

@b_bbirddd Lo peor de lo que ha pasado con Jon, aparte de que se haya cerrado la cuenta de X, es tener que ver la cara de acéfalo del esteinfraser apareciéndome cada dos por tres en el TL.

Español

j_dlo_g retweetledi

j_dlo_g retweetledi

El aviso de Funcas: la inmigración no soluciona el envejecimiento de España (y puede agravarlo)

El sistema migratorio español retiene a quien menos puede aportar.

🔸De los inmigrantes entre 20 y 54 años que llegaron entre 2021 y 2024, solo el 46% seguía residiendo en el país al cierre del periodo.

🔸La tasa de retención de los mayores de 54 años alcanza el 110%, fruto del asentamiento y del propio envejecimiento de los ya instalados.

🔸A esto se suma un perfil de llegada cada vez más envejecido: en 2024, el 17% de los recién llegados tenía más de 54 años, el cuarto dato más alto de la UE.

España deja escapar a quienes podrían sostener décadas de cotización y consolida a quienes pronto demandarán pensiones, sanidad y dependencia. La inmigración como receta demográfica compra tiempo y traslada al futuro una presión creciente sobre el Estado del bienestar.

Por @jgjorrin.

elconfidencial.com/economia/2026-…

Español

j_dlo_g retweetledi

Mientras esperamos el regreso de Jon González, hay quien también hacen muy buen trabajo: @pablogguz_, @SantiCalvo_Eco, @jgjorrin. Si me dejo a alguien, por favor, citadlo aquí, bajo este tuit. Si alguien creyó que la verdad se acallaría si Jon se cerraba la cuenta, se equivocaba.

Español

Y la Charo mirando y yéndose. Hay gente en esta mierda de país que no tiene solución.

EL MUNDO@elmundoes

Las brutales imágenes de Salvador, el anciano que fue arrastrado por un Cercanías en Pozuelo de Alarcón (Madrid)

Español

j_dlo_g retweetledi

Hemos pagado con fondos NextGen los pilares del estado del bienestar:

- pensiones

- IMV

- los chanchullos de Zapatero y el PSOE

Enhorabuena a todos

THE OBJECTIVE@TheObjective_es

Bruselas investiga si España ha pagado con fondos UE varios contratos de Huawei. Informa Pelayo Barro (@pelayobarro) theobjective.com/espana/2026-05…

Español

j_dlo_g retweetledi

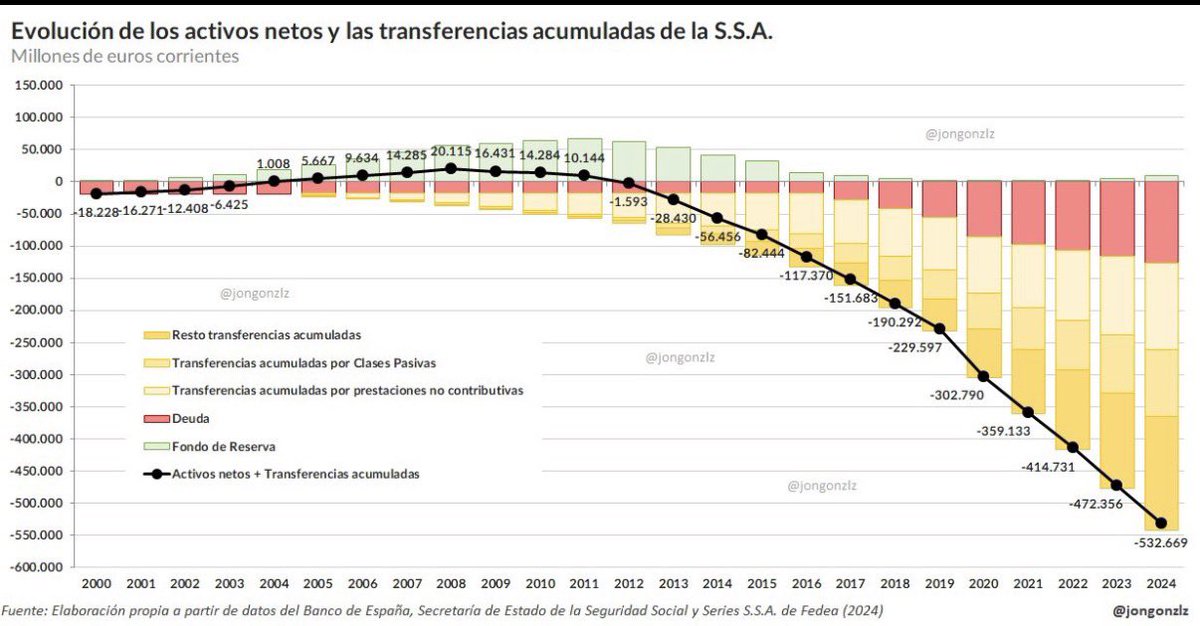

La Seguridad Social lleva más de una década financiando una parte notable de las pensiones con deuda y "transferencias" principalmente de otras administraciones públicas.

En 2024, sus ingresos ascendieron a 176.000 millones, mientras que tuvo unos gastos de más de 240.00 millones

EL MUNDO@elmundoes

La desviación de fondos europeos para pagar pensiones en España, en boca de la prensa de Alemania: "Absolutamente inaceptable" #Echobox=1778601614" target="_blank" rel="nofollow noopener">elmundo.es/economia/empre…

Español

j_dlo_g retweetledi

‼️💸 Bruselas confirma que España ha usado 10.200 millones de euros de fondos 'Next Generation' para gasto corriente elespanol.com/invertia/econo…

Español

j_dlo_g retweetledi

Andreas Schwab, presidente de la Comisión de Control Presupuestario: "¿Cómo pido yo a los alemanes que trabajen más mientras España paga pensiones con los fondos europeos?" #Echobox=1778648618" target="_blank" rel="nofollow noopener">elmundo.es/economia/2026/…

Español

Refundar el PSOE con Ábalos. Pues para eso mejor nos quedamos como estamos.

Vozpópuli@voz_populi

🟢 Exclusiva Vozpópuli. 📲 Los whatsapps de Susana Díaz a Ábalos que revelan la guerra para derrocar a Sánchez: “No hacemos mal equipo” 👇 Lee más información aquí: tinyurl.com/kmua8v28

Español

j_dlo_g retweetledi

j_dlo_g retweetledi

Yo no he realizado ninguna campaña de acoso contra Sarah Santaolalla.

Esta señora es la pareja de Javier Ruiz y colabora en el programa de la televisión pública que él presenta.

Eso no es intimidad, sino un posible conflicto de intereses pagado con dinero público.

Jon González trabaja en el sector privado, subía gráficos a Twitter y no se ha servido de nuestros impuestos ni de ninguna televisión pública.

Por lo que comparar ambos casos es absurdo.

Tu Primo del Barrio 🛠️@primodelbarrio

La derecha tuitera ha lanzado una nueva campaña para intentar silenciar a quienes exigen transparencia. Ahora atacan a Yago Álvarez, Eduardo Garzón o Carlos S. Mato. Quieren impunidad y victimizarse para no dar explicaciones. Es de un cinismo absoluto que esta cruzada la encabecen perfiles como Emilio M. Motilla, que atacó sin piedad la intimidad de Sarah Santaolalla, o que callan ante los métodos de Vito Quiles. Para ellos, el linchamiento personal es “libertad”, pero la ética y la transparencia son “persecución”. Sus ataques pretenden evitar que se conozcan los conflictos de intereses de quienes se posicionan con la élite económica. De esas personas no queremos saber su intimidad, ni que las despidan, ni que cierren sus cuentas. Simplemente queremos transparencia. No, no somos como vosotros.

Español

j_dlo_g retweetledi

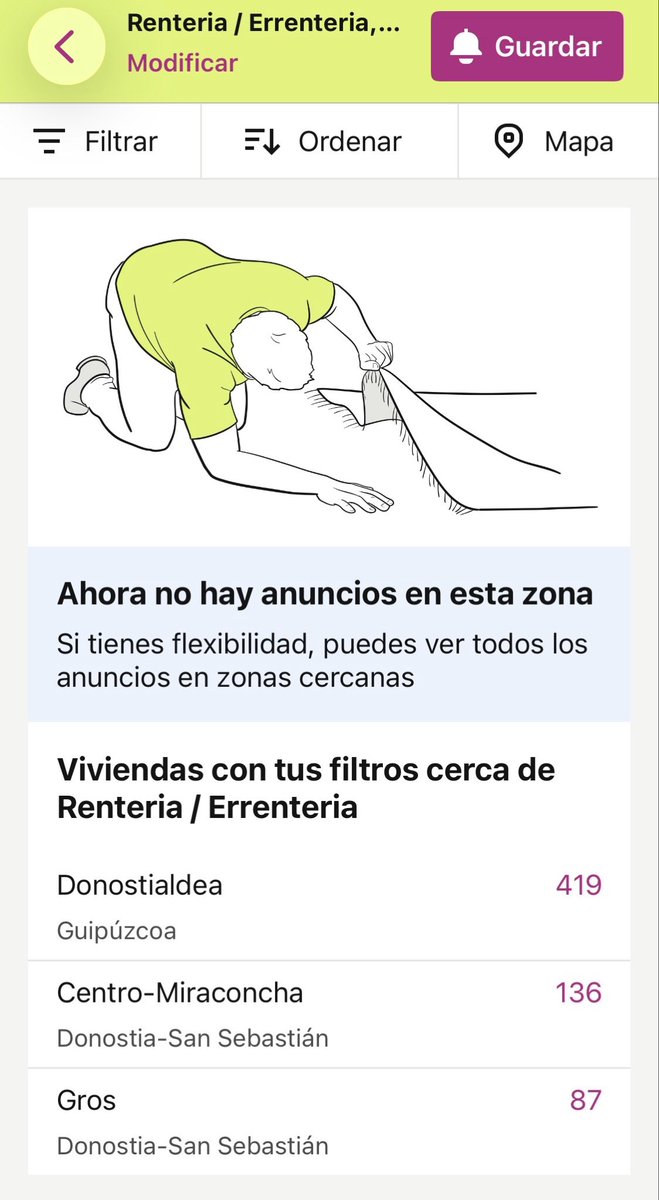

No me lo creía y lo he comprobado por mí mismo. Efectivamente, en Rentería, primera localidad del País Vasco en declararse “zona tensionada”, ya no hay pisos en alquiler. Lo que sí habrá, intuyo, son okupaciones.

A disfrutar de lo votado, amigos.

Español

j_dlo_g retweetledi

Este gráfico de Jon González es demoledor por 2 razones:

1- Es determinante para entender que el sistema de pensiones actual es un sistema completamente deficitario y abocado al empobrecimiento del trabajador actual.

2- Desenmascara al político farsante socialista cuando dice que la SS cotiza con superávit.

No importa la ideología que tengas, pero os prometo que en España se necesita más gente como Jon y menos como Garzón o @EconoCabreado

Español

j_dlo_g retweetledi

Seria volver por la puerta grande

En el podcast mas escuchado de hablahispana

HAZLO @JordiWild

Andrea MarGon ☘️@AndreaMarGon_

Ojalá Jon González fuera a contarle a @JordiWild todas las cosas que explica y que tanto han molestado a algunos. Esa audiencia joven debe ser consciente del sistema en el que vive.

Español