Jackson Gates

2.4K posts

Jackson Gates

@jacksongates

@ManresaVentures Previously at Affirm, Sweep (acq by Affirm), Pandora, Vulcan and Tenaya Capital. Married to @biancagates

San Francisco, CA Katılım Ağustos 2008

505 Takip Edilen1.8K Takipçiler

@omooretweets There are a few good counter examples here.

- Uber heavily relied on paid ads, subsidies and referral bonuses

- Airbnb was one of the largest Google Ads buyers in travel

- TikTok massive spending on Instagram/Snap early on and app install campaigns

English

In consumer, paid ads generally = lack of true product market fit

I have yet to see a generational startup with largely paid ad-driven growth…

andrew chen@andrewchen

lots of AI cos starting to experiment with paid marketing so here’s my take: Paid acquisition is a tax on your product's defensibility. the moment you can't out-spend the incumbents and competitors, you die. build channels that get cheaper as you grow or you're just renting your growth

English

I ridiculed the Metaverse (privately) when it was announced. But now as Ai is progressing, I think Mark was/is right but a little too early. Unfortunately people will want to live in the pink goo from the Matrix. I hate it. But I get it.

Autism Capital 🧩@AutismCapital

🚨 NEW: Meta finally pulls the plug on “The Metaverse”

English

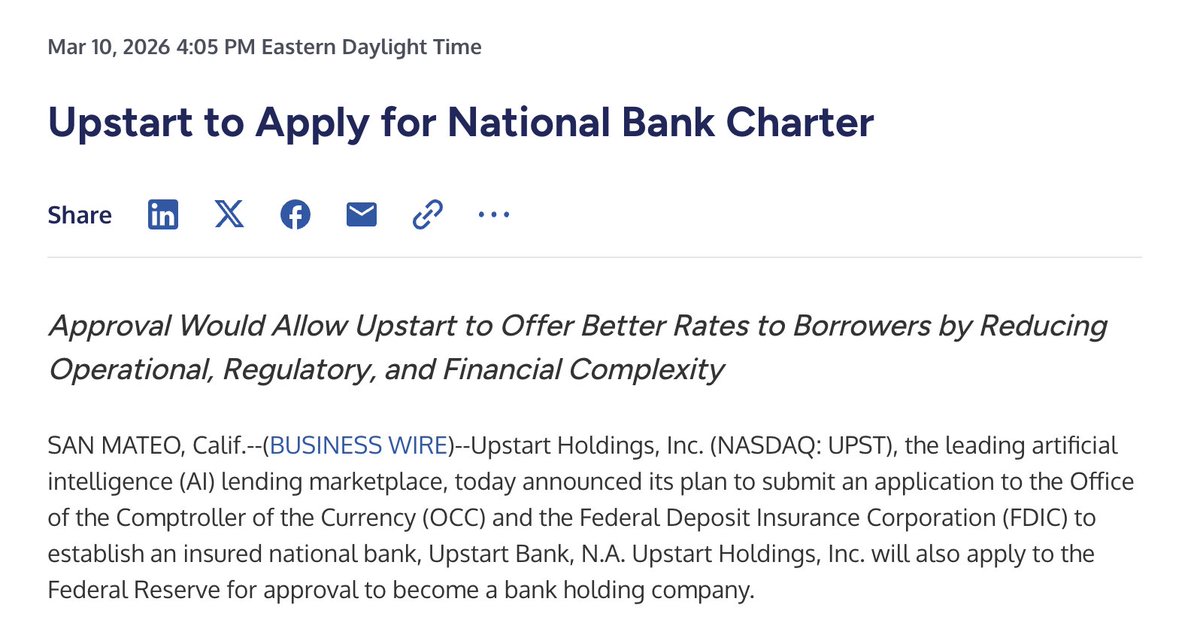

@regulatorynerd 3 reasons to get a charter - in order:

1) control your own destiny. Get as close to your regulator as possible.

2) reduce origination costs

3) fractional reserve banking - it’s amazing!

English

Block has another super power here, which is it can use its Industrial Loan Company for funding purposes. Likely why Affirm and PayPal have both applied for a similar charter.

matt ross@emcross23

Got a couple questions on this today. FWIW this is a nothing burger for Block. We do not sell any consumer loans. We historically had small pilot programs selling BNPL but it was never meaningful. We do sell majority of Square loans off balance sheet. But we have a diverse funding partnership strategy and in many cases have had decade long partnerships delivering strong returns to investors.

English

@kallasmaa @digitalpeyote @sytaylor Have you ever looked to see how many bps Visa/MC actually take on their card volume?

English

@digitalpeyote @sytaylor 0.5% should be enough to cover KYC and for you to make a profit.

English

All of crypto is pivoting to virtual cards and it's so weird to me as a fintech guy.

Like yeah.

It's a virtual card?

Romford, London 🇬🇧 English

@regulatorynerd @commbankerguy Good points. I suspect we had the same dynamic with stocks, bonds and land speculation pre SEC (1934). You can’t eliminate the assets once consumers want to buy that risk - but you can regulate and specifically demand uniform transparency under harsh penalties for issuers.

English

I agree — the fascinating thing that most regulators and policymakers aren’t grappling with is what happens when foreign CBDCs or quasi-CBDC and self-hosted wallets give consumers the ability to opt into an entirely different banking and monetary system.

The bank lobby is crying wolf over small business lending to try and hobble domestic stablecoins. But the real threat is borderless and digital. It’ll be like TikTok. One day everyone in Gen Z (and younger) will have it and we won’t be able to take it away.

Not rooting for it, but calling it like I see it.

English

I don’t care about yields and rewards as long as they are regulated like a Bank. The bankers that are arguing over this yield stuff are right about reduced lending being an outcome or higher rates, but it’s competition. adapt or die.

James E. Thorne@DrJStrategy

For the record. Banks are aggressively fighting the CLARITY Act (Digital Asset Market Clarity Act), stalling it in the Senate over one core issue: banning or severely limiting rewards/yields on stablecoins and crypto holdings. Their argument? If platforms like Coinbase or Circle offer 2-4% rewards on stablecoin balances (or even activity-based incentives), it could siphon trillions in deposits from traditional banks → hurting lending, community banks, and the whole fractional reserve system. ABA (American Bankers Association) and others rejected White House compromises allowing limited rewards (e.g., only for P2P payments, not idle holdings), calling it a dangerous loophole. They've lobbied hard, signed letters from thousands of bankers, and framed it as protecting financial stability. Yet here's the glaring hypocrisy: Mastercard (and partners) already enables crypto rewards cards that let users earn BTC, ETH, or other tokens as cashback on everyday spending: - Gemini Mastercard: Up to 4% back in crypto on categories like dining/gas. - MetaMask Card (launched/expanded 2026): Tiered crypto rewards (1-3%+). These rewards effectively give users a yield-like benefit on spending crypto/fiat equivalents, competing for wallet share and "draining" potential bank deposits by incentivizing crypto use. Mastercard operates fully regulated, partners with banks/fintechs, and funnels everything through traditional rails. No mass outcry from banks calling this an existential threat. So banks scream about "unfair competition" and deposit flight from crypto-native rewards/yields... but stay quiet (or partner) when Mastercard enables similar incentives at massive scale. It's not about principle or stability, it's about protecting incumbents from decentralized outsiders while cozying up to "inside-the-system" players. Regulatory capture 101: Clarity for crypto? Sure... as long as it kneecaps the competition and leaves bank-friendly rails untouched. Time to call out the double standard. If rewards are so dangerous, why the pass for Mastercard's crypto card ecosystem? Consumers deserve better than protectionism disguised as prudence. #CLARITYAct #Stablecoins #CryptoRewards #Banking #Fintech

English

@regulatorynerd @commbankerguy Yes. This is simple. If you hold consumer funds -> regulated. If you buy assets with those funds -> more regulation and disclosure needed.

English

With self custodial wallets, people are eventually going to find foreign issued coins that pay yield or whatever feature it is consumers care about at that point in time (related, each generation is different/wierd with money). Like I wouldn’t have put money in Yotta (fintech) or BlockFi (crypto), but a lot of people did and some of them had bad outcomes. Consumers will migrate based on incentives, even if it’s to unsafe and unstable substitute products.

Agree it’s adapt, compete or die.

English

@jevgenijs If you’re legit, get as close to your regulator as possible. Reduce risk and control your own destiny. Second benefit is the profit from fractional reserve banking.

English

@RogueCfpb Isn't he saying that subprime borrowers would be better off without any credit at all? Good credit already subsidizes bad credit. He wants to just take away access to credit. Which is dumb... of course.

English

In case we’re wondering, here’s one of the supporters of the 10% credit card cap explaining the root goal and, funny enough, the answer is … socialism

Let’s have the responsible card users pay more to cover the costs of the less responsible card holders. Because that’s definitely a very rational and sane way to drive more responsible card holders!

Joel Gombiner@joelgombiner

They're a form of predatory lending that transfers money from poorer borrowers to wealthier ones. Capping rates and reducing credit access will lead to BETTER financial outcomes for the people who are being taken advantage of, and slightly worse outcomes for people who are already doing well.

English

Lemkin is always on point. When Sweep was struggling, Mitch Kapor asked us how bad we wanted to survive? And if we were willing to cut off our arm with a pen knife like the climber trapped by a boulder in the movie 127 Hours. Hard truths are needed.

Jason ✨👾SaaStr.Ai✨ Lemkin@jasonlk

Growth slowed? Get the co-founders together in a room. Lock the door. Now you'll see the only team available to fix things. No one else is coming to help you. It's up to you. How badly do you want to get back to growth? Only founders can care enough to really do it. It's just you. Looking at each other. Deciding how badly you really want it. How much even harder you are willing to work. And how much pain you are willing to endure.

English

@mattaparker Only way to satisfy the request for "management experience" and more direct reports.

English

never seen this before.

Public founder:

“If you’re going to short my stock, here’s how to do it efficiently.”

Contrast that with:

“Shorts are market manipulators.”

Mike Cagney 🇺🇸@mcagney

So 50% of @Figure's stock float is being shorted. And it underscores why we have OPEN. If you are holding FIGR in a brokerage account, most likely they are lending out your stock to short sellers and you aren't getting paid. If you are fortunate enough to have a prime broker, they are paying you something close to fed funds for your stock loan. My guess is the borrow rate right now is over 20%. This isn't about whether you should be long or short FIGR (or me trying to cause a shorts squeeze), but about long shareholders getting paid. You can move your shares to OPEN (on the blockchain) and lend them out there. By doing so, you force whoever borrowed your shares to cover, and move to OPEN to borrow directly from you. And you can move your shares back to Nasdaq when you want to sell if you have concerns around OPEN liquidity/pricing.

English

@brezina Always. They provide an incredible amount of value to all sides of the network. Negotiate economics, assign risk, set and enforce rules, ensure liquidity. And they do it all for 12bps globally. Who is going to do a better job at a cheaper price than that?

English

PGA was a basketball guy. But he bought the Hawks to keep them in Seattle - then built a world class facility and won two Super Bowls. And all proceeds will go to his foundation and it's philanthropic programs. Incredible steward of this franchise.

Seattle Seahawks@Seahawks

Estate of Paul G. Allen Begins Sale Process for Seattle Seahawks

English

@rexsalisbury If you insult apple pie next we are really going to have to fight.

English

@jacksongates my new hobby is trolling you w/ anti-home ownership posts ;)

English

Homeownership vs Office Ownership.

Imagine telling a company:

"BEST way increase your valuation is to own your office"

Makes no sense.

But we tell every american:

"best way to build wealth is own a home."

English

"Crypto" can mean many things so it's dumb to say it's "dead". But what is going to be the catalyst? For internet and mobile, we knew that greater bandwidth + compute at cheaper prices would be the catalyst. And those things led to the iPhone moment. It was inevitable. For crypto - I don't see it unless you believe governments and societies are decaying and losing power. I see the opposite... If anything, stablecoins are the killer use case because governments will track every penny to every person.

Chris Dixon@cdixon

English

@bradr AI says "it's not just a cron job -- it's a revolution." ;)

English

honestly, "it's just a cron job" is such a bad take.

normal people do not know about or have access to a cron job. their closest approximation is their oven or iPhone.

a cron job is an incredible thing engineers take for granted. to set one up in a sentence is a revolution

English

Affirm should do a hostile takeover.

Scott Wessman@scottew

Stripe should go public by buying PayPal kidding, unless

English

best way to help 1st time homebuyers?

raise property taxes.

oh by the way, this actually raises tax revenue. unlike every other scheme to "help first time homebuyers", which costs a lot.

Crémieux@cremieuxrecueil

Lyman is right. Property taxes are one of the best types of taxes currently in use. They're a great way to help young people settle down to start families. If California's property taxes were shifted up to Texas' higher rates, the housing available to the young would increase.

English