Jaynit@jaynitx

>be John D. Rockefeller

>born 1839 in Richford, New York

>dad is a literal con man who sells fake cancer cures, has a secret second family

>mom is ultra-religious, holds the household together with prayer and rage

1850s:

>family moves constantly because dad keeps disappearing

>age 16, get your first job as a bookkeeper in Cleveland

>$0.50 a day

>never miss a cent

>track every penny in a little notebook, does this for the rest of his life

>call it "Ledger A"

1859:

>oil discovered in Pennsylvania

>black gold chaos

>everyone rushes in like maniacs

>you watch, calculate, wait

1863:

>age 23, invest in a refinery instead of drilling

>"drilling is gambling, refining is business"

>partner with Samuel Andrews

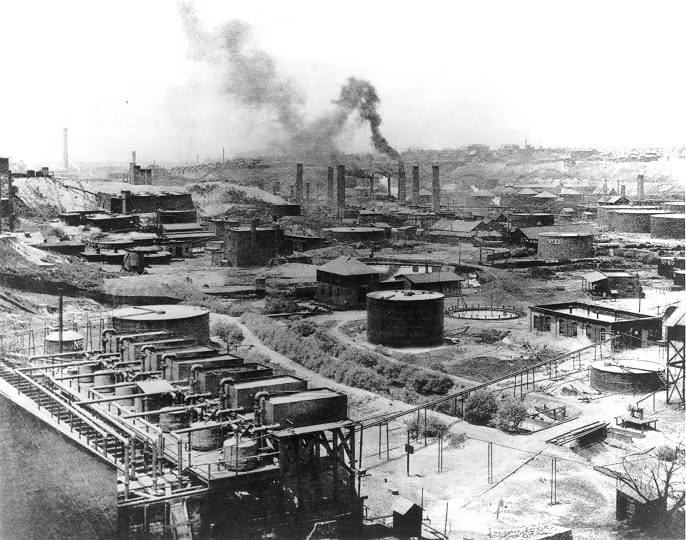

>first refinery goes up in Cleveland

1870:

>found Standard Oil

>$1 million capitalization

>the empire begins

1871-1879:

>execute "The Cleveland Massacre"

>buy or crush 22 of 26 Cleveland refineries in 2 months

>competitors get a choice: sell or die

>secret railroad rebates, you pay less to ship than everyone else

>competitors can't compete on price

>they fold

>repeat in Pittsburgh, Philadelphia, New York

>by 1879, control 90% of American oil refining

>the most complete monopoly in U.S. history

1880s:

>create the "Trust": a legal innovation to hold all companies under one roof

>lawyers: "this is... legal? technically?"

>you: "make it legal"

>Standard Oil Trust controls pipelines, refineries, barrels, even the railroads

>vertical integration before the term exists

>politicians, judges, newspapers, all on payroll

>called "The Octopus", tentacles everywhere

1890s:

>public hatred explodes

>muckrakers come for you

>Ida Tarbell writes a 19-part exposé; her father was ruined by you

>it's devastating, factual, and dripping with rage

>you say nothing publicly

>keep going to church every Sunday

1892:

>trust gets broken up in Ohio

>response: restructure as a holding company in New Jersey

>barely a speedbump

>Standard Oil of New Jersey now runs everything

1897:

>retire from day-to-day operations at 58

>shift focus to giving money away

>but you're still the richest man on earth and getting richer

1901:

>worth $200 million (~$7 billion today)

>oil keeps pumping

>money keeps compounding

>you can't spend it fast enough

1902:

>net worth hits $900 million

>adjusted for GDP share: you're worth $400 BILLION

>richer than Elon, Bezos, Gates combined

>no one has ever been this rich

>no one may ever be again

1904:

>Ida Tarbell's book "The History of Standard Oil" drops

>public opinion shifts hard

>antitrust heat intensifies

1911:

>Supreme Court rules Standard Oil is an illegal monopoly

>company broken into 34 pieces

>ExxonMobil, Chevron, BP America, all born from the corpse

>plot twist: you own shares in ALL of them

>breakup makes you even richer

>can't stop winning

1913:

>create the Rockefeller Foundation

>mission: "promote the well-being of humanity"

>$250 million seed money (billions today)

>fund medical research, universities, global health

>eradicate hookworm across the American South

>fund the research that creates penicillin

>basically invent modern philanthropy

1920s:

>fund the University of Chicago

>fund Rockefeller University

>fund Spelman College

>rebuild Versailles

>restore Colonial Williamsburg

>give away $540 million total (~$10B+ today)

>live like a monk, crackers, milk, golf, church

1930s:

>Great Depression hits

>you're still alive

>still rich

>people finally stop hating you

>now you're the nice old man who gives to charity

1937:

>die at 97

>outlived most of your enemies

>outlived the hatred

>left behind:

— the modern oil industry

— the template for monopoly capitalism

— the playbook for billionaire philanthropy

— a name that still means "rich" 100 years later

your descendants:

>Vice Presidents, Governors, bankers, senators

>Rockefeller Center stands in Manhattan

>five generations later, family still runs foundations

you gave more money away than any human before you.

you also destroyed more competitors than any human before you.

the original American titan, and no one's topped you yet.