@KLorenCompany @ashleevance anything that originated at MIT?

English

James Krellenstein

4.3K posts

@jbkrell

CEO and Co-Founder, @AlvaEnergyIo

Am I the only one who is NOT on GLP-1s, SSRIs or peptides ?

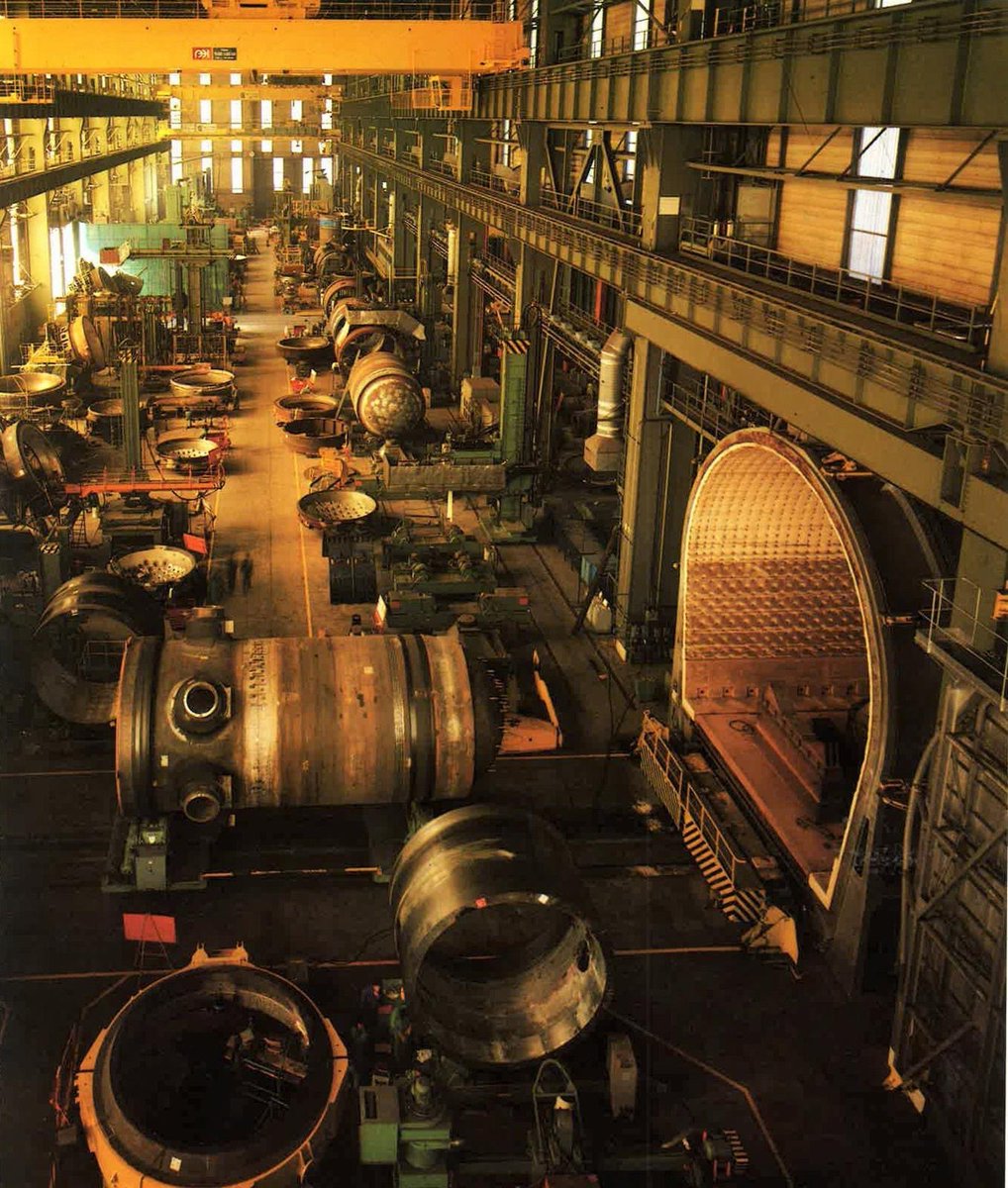

The Most Overlooked Opportunity in Nuclear? Why Nuclear Power Plant Uprates Beat Everything Else in the Race for New Capacity. Recent conversations about the budding nuclear renaissance often begin with the same list. Microsoft restarting Three Mile Island, tech companies partnering with advanced nuclear reactor vendors or the proposed Japanese funded US AP1000 fleet build. These announcements generate headlines, volatile valuations and investor decks. Meanwhile, forty Westinghouse pressurized water reactors (PWR) sit at roughly the same thermal power output they were commissioned at decades ago, operating within design margins calculated on transistorized computers before integrated circuits existed. Together, these plants hold between 6-10GW of additional capacity, the equivalent of eighteen to thirty 300MW SMRs, that could be unlocked faster and cheaper than any other nuclear source and perhaps even faster than new gas. My conversation with returning guests Robb Stewart (@nuclear_robb) and James Krellenstein (@jbkrell), CTO and CEO of Alva Energy (@alvaenergyio), made the case that power uprates at existing PWR plants represent the lowest-hanging fruit in the sector, bypassing the megaproject risks and nuclear supply chain rebuilding that make new nuclear construction so daunting for utilities. The components turn out to be far more manageable and anticlimactic than new build nuclear: non-safety-related secondary side equipment such as feedwater heaters and condenser tube bundles, alongside nuclear-grade steam generators that the fleet has already learned to replace during their month long scheduled outages using well-rehearsed industrial choreography. Alva’s approach avoids the traditional uprate bottleneck by building a separate standardized 250MW Second Turbine Generator Plant (2TGP) building diverting incremental steam from an uprated core without touching the existing turbine centerline. Most of the construction happens on a conventional, non nuclear island using mature supply chains and firm fixed price engineering, procurement, and construction contracts, leaving the outage window limited to a short tie in during a normal refueling cycle. Compared to a cohort of first of a kind nuclear steam supply system startups that accessed public markets through SPAC mergers and achieved substantial valuations in the hundreds of millions on compelling nuclear narratives this approach sounds deliberately boring. But perhaps boring is what our current moment demands. The question is whether the American nuclear zeitgeist can resist the allure of novelty long enough to pluck the low hanging gigawatts hiding in plain sight.

The Most Overlooked Opportunity in Nuclear? Why Nuclear Power Plant Uprates Beat Everything Else in the Race for New Capacity. Recent conversations about the budding nuclear renaissance often begin with the same list. Microsoft restarting Three Mile Island, tech companies partnering with advanced nuclear reactor vendors or the proposed Japanese funded US AP1000 fleet build. These announcements generate headlines, volatile valuations and investor decks. Meanwhile, forty Westinghouse pressurized water reactors (PWR) sit at roughly the same thermal power output they were commissioned at decades ago, operating within design margins calculated on transistorized computers before integrated circuits existed. Together, these plants hold between 6-10GW of additional capacity, the equivalent of eighteen to thirty 300MW SMRs, that could be unlocked faster and cheaper than any other nuclear source and perhaps even faster than new gas. My conversation with returning guests Robb Stewart (@nuclear_robb) and James Krellenstein (@jbkrell), CTO and CEO of Alva Energy (@alvaenergyio), made the case that power uprates at existing PWR plants represent the lowest-hanging fruit in the sector, bypassing the megaproject risks and nuclear supply chain rebuilding that make new nuclear construction so daunting for utilities. The components turn out to be far more manageable and anticlimactic than new build nuclear: non-safety-related secondary side equipment such as feedwater heaters and condenser tube bundles, alongside nuclear-grade steam generators that the fleet has already learned to replace during their month long scheduled outages using well-rehearsed industrial choreography. Alva’s approach avoids the traditional uprate bottleneck by building a separate standardized 250MW Second Turbine Generator Plant (2TGP) building diverting incremental steam from an uprated core without touching the existing turbine centerline. Most of the construction happens on a conventional, non nuclear island using mature supply chains and firm fixed price engineering, procurement, and construction contracts, leaving the outage window limited to a short tie in during a normal refueling cycle. Compared to a cohort of first of a kind nuclear steam supply system startups that accessed public markets through SPAC mergers and achieved substantial valuations in the hundreds of millions on compelling nuclear narratives this approach sounds deliberately boring. But perhaps boring is what our current moment demands. The question is whether the American nuclear zeitgeist can resist the allure of novelty long enough to pluck the low hanging gigawatts hiding in plain sight.

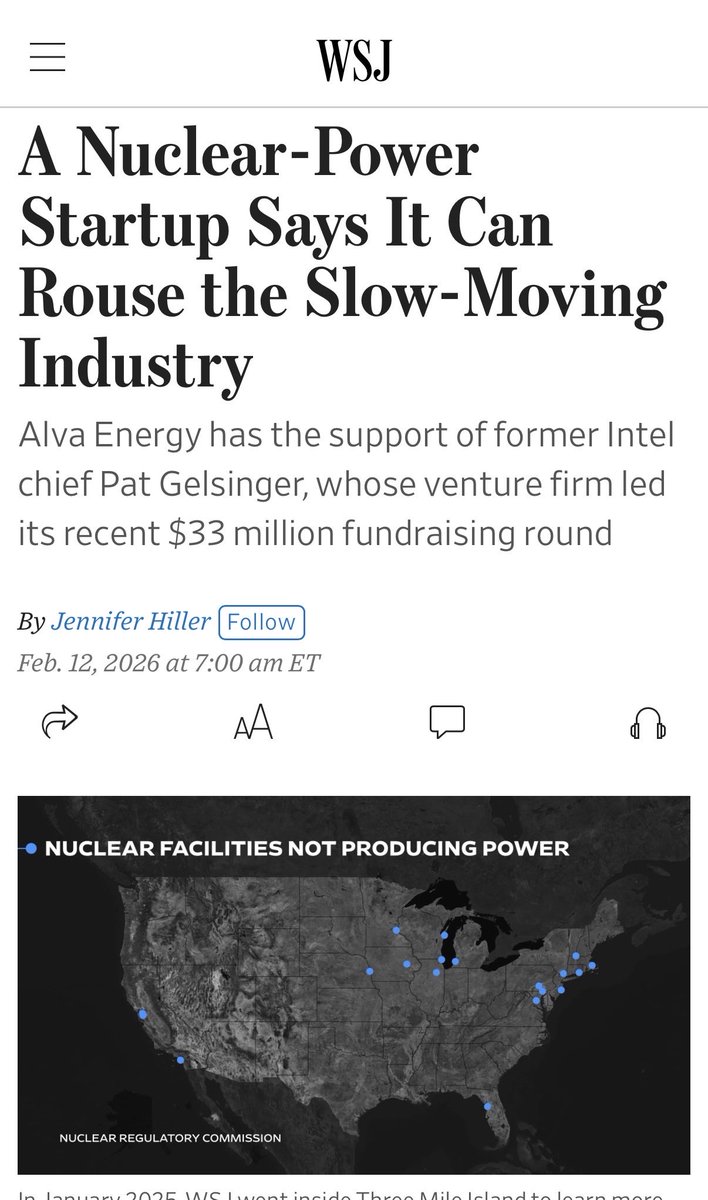

The Wall Street Journal covered the exciting news that Alva Energy, a nuclear energy startup company co-founded by James Krellenstein (@jbkrell), had raised $33 M in venture capital. The company has the goal of adding approximately 10 GWe of nuclear electricity generating capacity by uprating existing Pressurized Water Reactors by 200-300 MWe, requiring 30-40 individual projects. Uniquely, Alva believes they can dramatically improve the economics of power uprates with a several step process that minimizes cost and revenue-killing down time. Their public estimates indicate a cost per project of ~$1 B and a project duration of 5 years. Here is my understanding of the basic concept. Please share thoughts and corrections. Build a medium sized electricity generating steam plant adjacent to the operating unit while the unit continues to operate. During a properly selected outage window, replace existing steam generators and connect the new steam plant as an additional path for the steam generated by the plant. Use modern control systems that can dynamically balance steam flows for the new steam turbine configuration. It will include the existing ~1000 MWe turbine-generator and the 200-300 MWe turbine-generator. The reactor will need to be modified and the operating license amended to produce the additional 600-900 MW of thermal energy. Current NRC operating licenses are for MWth, not MWe. Power uprates are not uncommon, but they became rare during the period between 2008 and 2023 when there was so much excess capacity on the grid that nuclear plant owners were closing reactors. They couldn't sell power the power they produced for a profitable price in an over supplied market. In that situation, investing hundreds of millions in new capacity made no sense. According to @Jennifer_Hiller's WSJ article, Alva is targeting PWRs. It believes that most of the potential uprate capacity in BWRs has either been exploited or soon will be through existing processes. BWRs – obviously – do not need steam generator replacements as part of an uprate project. It's no secret that electricity demand is growing again or that there are customers who are keenly interested in contracting for more of the clean firm power that nuclear reactors produce in abundance. Note: If you are, like me, a @DecoupleMedia fan, you might feel like you know Alva Energy's co-founder quite well. James has been a frequent guest on @Dr_Keefer's popular nuclear energy/geopolitics/climate change podcast. A gift article link to the WSJ article is available in the comments.

Exclusive: The startup Alva Energy says it knows how to kick-start the slumbering nuclear-power industry—and former Intel CEO Pat Gelsinger is backing its efforts on.wsj.com/4bN5SZ7

Has no one at the @nytimes taken a linear algebra class?

We are not a serious country. 10 gigawatts… “first shovels hit dirt before 2030” China built 93 gigawatts of solar in a single month.