Sabitlenmiş Tweet

English

0x.Nya

2.6K posts

@jin_devilfruits

Gunmon & Class 2017. My brainfarts and occasionally alpha (NFA) https://t.co/P7KSs3bfaF

Finally solved. Thank you. It took a while but glad it is resolved :) @ether_fi

Day 109

x.com/jin_devilfruit… Day 94 and still nothing. @ether_fi

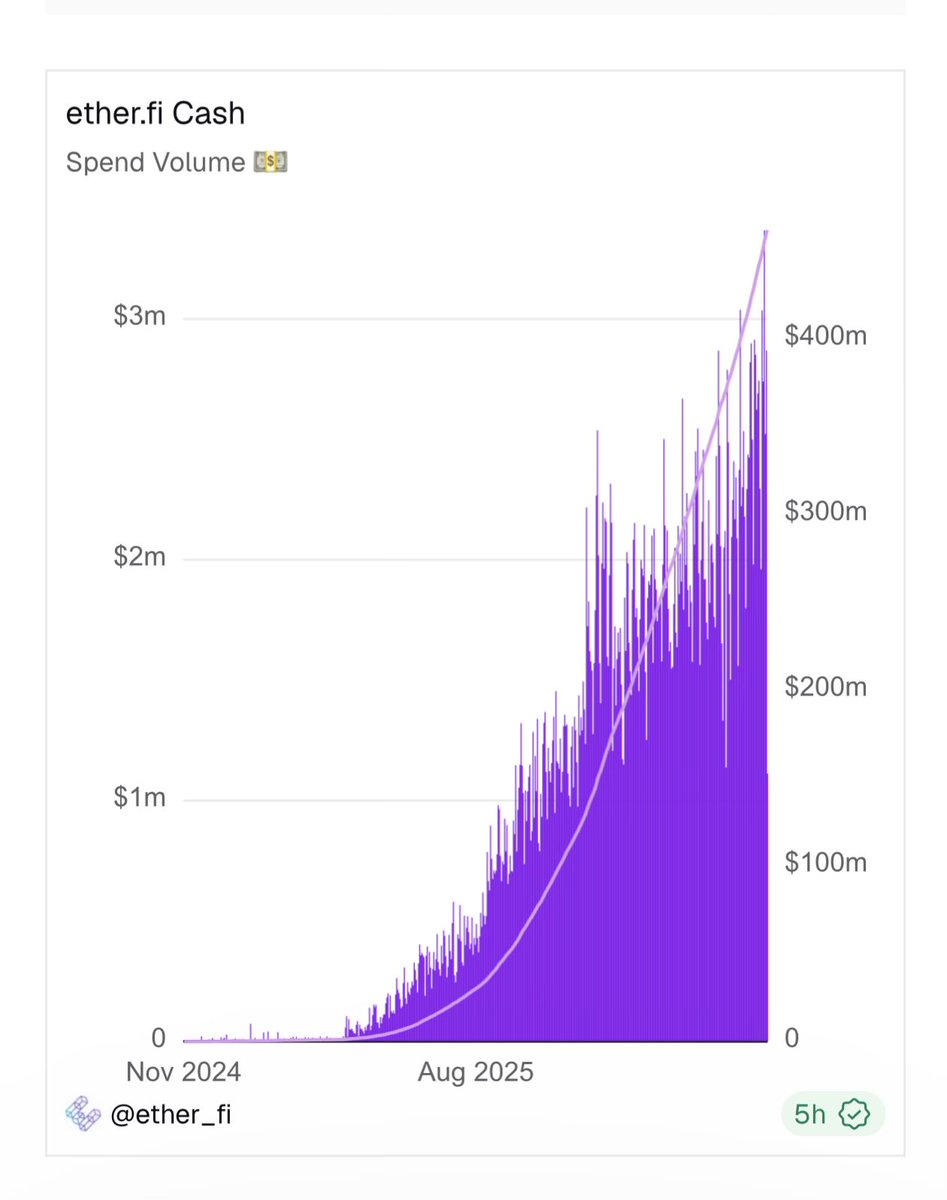

Today, EtherFi Cash hit an all-time high in spend volume. More and more users are choosing EtherFi because Cash makes it easy to grow your crypto and use it in daily life. Thank you for choosing EtherFi. Higher.

@ether_fi @MikeSilagadze still waiting bro