Joel Li

593 posts

Joel Li

@JoelLi

CEO @EVcom, an Everything EV platform

New York Katılım Mart 2019

963 Takip Edilen1.3K Takipçiler

The sentiment around KOSPI | $EWY (SK Hynix / Samsung) on

Crude Oil / LNG / Helium either:

Disrupting Supply or Compressing Margins are overblown.

The supply chain disruption and energy cost threats to SK Hynix, Samsung are sensationalized noise.

Here's why:

1. Crude Oil:

The a likely scenario if oil prices increase 31% and oil floats to $120/bbl:

In this case, the effect on oil has almost no material impact on SK Hynix and South Korean memory equities.

There are increased energy costs via oil-pegged LNG/JKM prices on Korean equities, mainly for companies surviving on razor-thin 5% to 10% margins.

However, a KEPCO 70% rate hike has little material affect on Samsung/SK Hynix, given memory prices have soared with Samsung doubling NAND prices Q2.

From disclosed financial from, their SK Hynix's annual electricity bill exceeds ₩1 trillion per DIGITIMES (~$750M). Which against FY2025 revenue of ₩97.15 trillion represents roughly 1–2% of revenue.

SK Hynix posted a 58% operating margin in Q4 2025. Against this backdrop, the energy cost shock is small:

If we model a 50% increase in energy costs:

- Hit to SK Hynix quarterly OP (₩19.17T): ~₩134 billion-~₩146 billion (0.76%)

- Hit to Samsung DS quarterly OP (₩16.4T): ~₩407 billion (2.4%)

Every 50% energy cost spike would shave roughly .7% off SK Hynix margins and 2.4% off Samsung operating margins.

Analysts project SK Hynix margins could reach 70%+ on conventional DRAM in 2026. Energy costs do not meaningfully threaten Korean semiconductor operating margins, even if they were to increase by 100%.

However, this is material to companies with low operating margins of 5-10%

The Losers: Traditional heavy manufacturing (steel, basic chemicals, standard flat glass).

The Winners: Samsung/SK Hynix.

The main risk is second-order effects on supply chains such as increased material costs. This is very hard to model, but in an example where:

an industrial company forces 30% price hikes on raw materials (chemicals, specialty gases), it barely dents the fabs.

Materials are roughly 15-20% of semiconductor COGS, so mathematically, a 30% spike in material costs only shaves an additional ~2% off SK Hynix's operating margins.

A combined 3-4% direct (utilities) and indirect (materials) energy headwind is easily absorbed by an oligopoly printing 70% margins (and increasing prices).

In majority of cases, the costs likely get passed down to hyperscalers through NAND/DRAM price hikes.

In the very worst case scenario of oil prices increasing 3x or 5x.

The main affect on oil increasing hundreds of percent are two factors:

- Global macroeconomic shock, causing global inflation (affecting every single company, from $GOOGL to $COST).

- KRW (South korean Won) USD/KRW exchange rate blowout.

KRW depreciation from sustained high oil is a real second order risk, but historically Korean memory exporters benefit from won weakness on the revenue side. The majority of Samsung/SK Hynix sales are dollar denominated wheras costs are won denominated. So a weaker KRW is actually margin accretive for exporters, which partially offsets the energy cost headwind.

But in an extreme case of oil prices hiking 5x, the only longs in that apocalyptic world are crude oil itself, defense contractors like $LMT / $NOC, domestic US energy producers, and the US Dollar.

This is unlikely to happen.

The financial media and algorithms will likely panic, but , if crude oil goes from $91 to $120 and KEPCO increases energy costs:

The data shows there's little affect on Samsung / SK Hynix in specific, and the main impact are on players with razer-thin operating margins.

2. LNG:

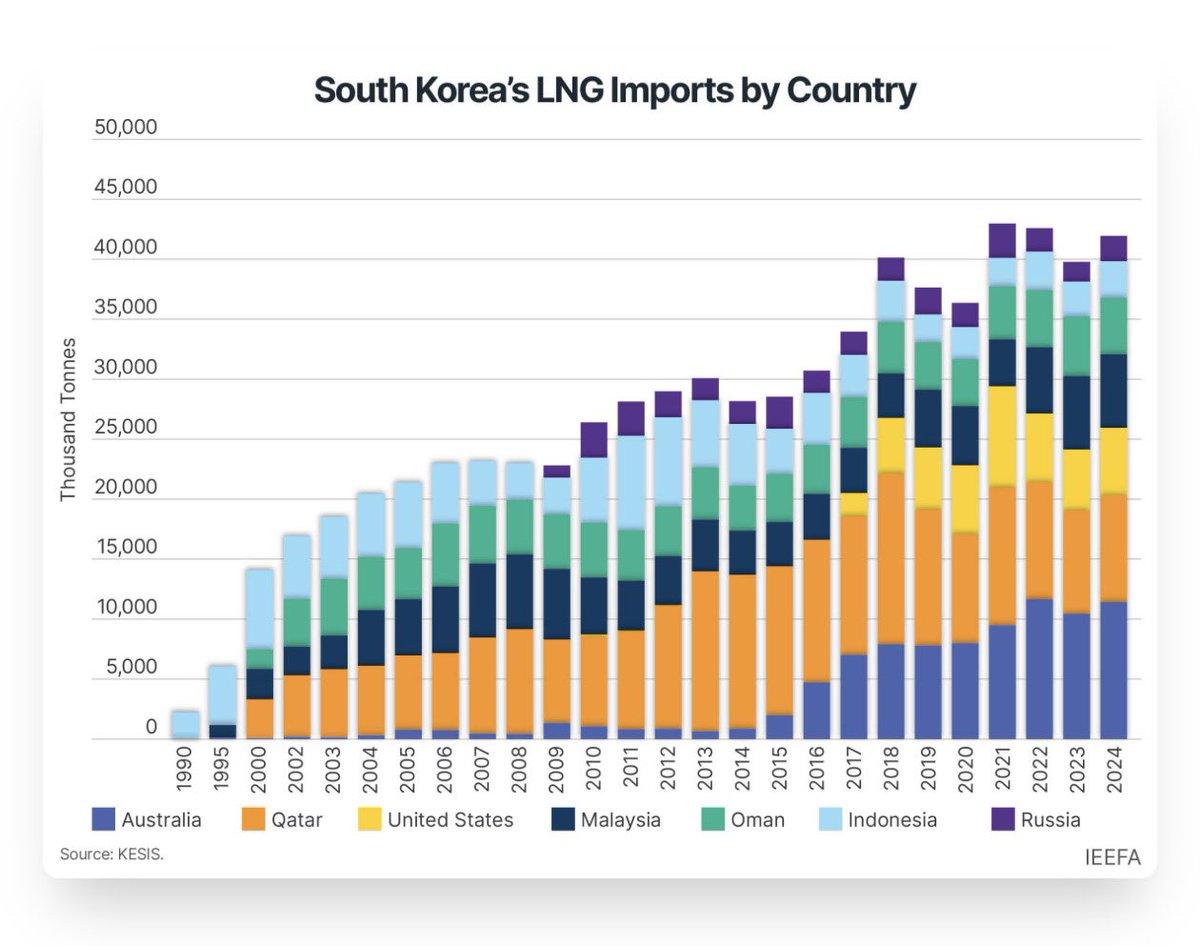

If the Hormuz closed, the majority of South Korea’s LNG imports would be unaffected.

The media has been quoting Hormuz + LNG flows going to China, INdia, SK, and Japan. But if we look at the trade data from South Korea, that’s just a fraction of their total imports.

Majority of imports arrive via Hormuz free routes, eg. Australia (24.6%), US (12.2%), Malaysia, Indonesia (~20%), and Russia/Sakhalin (~4.6%). Then the rest filled in with minor sources from Nigeria, Peru, Brunei, PNG, etc.

The 82% of 2024 important were long term contracts that were oil-indexed, and as we've modeled above, increasing energy costs would hurt opex by 1-2% per 50% increase, but given DRAM/NAND price hikes and operating margins hitting 70%+, this would make a very little dent.

Even if they did, costs would be passed onto hyperscalers.

South Korea learned their lesson from 2022 and diversified sources, and there's little impact on LNG supply disruption. The main concern is oil impacting hiking of LNG.

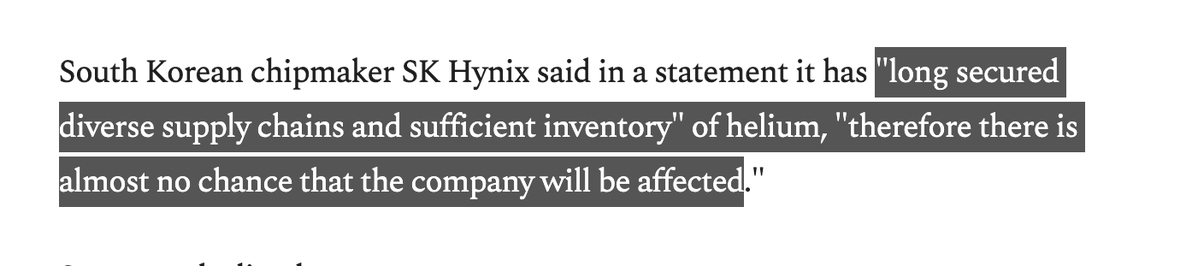

3. Helium:

SK Hynix statement: “Long secured diverse supply chains and sufficient inventory" of helium.

"Therefore there is almost no chance that the company will be affected [by helium].

The reality is larger players like $TSM to SK Hynix have diversified their supply chains against foreign events.

Helium is critical to semiconductor supply chains, but the media narrative is sensational. Especially when the largest memory company puts out an assertive statement that there’s no chance the company [SK Hynix] will be affected.

_

But to South Korean equities in Samsung/SK Hynix, fears around Oil/LNG/Helium look disconnected from reality:

The algorithms selling off SK Hynix because of helium and KEPCO rate hikes are acting on bad math. It is fundamentally a supply chain non-issue.

The main threat is oil and energy costs on global macroeconomic shock affecting everything from consumer goods to inflation.

March 3 "Black Tuesday" crash dropped KOSPI dropped 7.2% and SK Hynix fell 11.5% in a single session on exactly these energy security fears as the main catalyst. Of course, forced liquidations from leverage added fuel to the fire.

However, the disconnect between fundamentals and price action is the trade. If margins were actually threatened, the selloff would be justified.

But, the sell-off destroyed more value in one day than DECADES of hiked energy cost increases could have.

The fact that the math doesn't support the fear is precisely why it's Korea is a buy, as markets are selling off on emotion rather than looking at the structural expanding profitability despite increasing oil/energy costs.

English

@DanBTC916 Has it been bottomed? We still dont have a timeline for when Tesla could remove safety drivers. It may take months

English

We are starting to lightly add $TSLA shares again.

The last time we added TSLA was on 11/21/25 at $386.29

Dan ⚡️@DanBTC916

Yes, we added a little bit of $TSLA earlier today at $386.29 Posted real time thoughts and much more for Subs.

English

Having chatted with friends at other AVs, it seems the most likely way for legacy car OEMs to survive is to make autonomous vehicles for AV companies or they will have to scale back their manufacturing capacity.

There are already several hints that this is happening.

English

Joel Li retweetledi

It sure is a tall order 😂

Anyone can buy Tesla stock right now and come along for the ride.

There will inevitably be some bumps along the way, but, with a truly immense amount of work, I think these goals can be accomplished.

phil beisel@pbeisel

The final boss in Musk's 2025 Comp Plan is achieving $400B in EBITDA. Perspective: $238.24 billion: Saudi Arabian Oil Company (Saudi Aramco) achieved the highest annual EBITDA on record in 2022, driven by elevated global oil prices, higher sales volumes, and strong refining margins amid geopolitical tensions and post-pandemic demand recovery. This figure surpasses other major companies like ExxonMobil ($102.59 billion in 2022) and NVIDIA ($34.48 billion in fiscal 2024). For context, Aramco's 2023 EBITDA was approximately $236.81 billion, still leading but lower than 2022's peak. Let that sink in.

English

@DanBTC916 I doubt Tesla will rally unless deliveries exceed 500,000, and that seems unlikely.

English

If $TSLA beats Q3 delivery estimates, I’m anticipating a rally followed by a fade as traders take profit.

I think it will be healthy to see a near term pullback / consolidation after Q3 deliveries heading into Q3 2025 earnings, mainly to cool off technicals which can set up for the next move higher (if $TSLA tops guidance).

What are you guys expecting on Q3 deliveries?

English

@DanBTC916 @ChrisDungeon Has it not been priced in already? The market is expecting a very strong q3 and solid earnings call from Elon. If any failed for whatever reason, we would most likely see a sell off instead of a rally. Just my 2 cents

English

Been thinking over the weekend. I think Q3 earnings beat + topping Q4 guidance heading into the shareholder meeting will surprise the market and trigger a huge rally.

Giving a lot of weight on guidance.

Good point on incentives being aligned leading up to the shareholder meeting.

Going to be adding shares and calls on all dips. If we get a massive earnings + guidance beat, will take some profit on calls into the shareholder meeting.

English

Might not be obvious to most $TSLA holders...

Q3 deliveries and EPS will be bangers 🔥

How do I know this?

Because Elon's comp plan vote is Nov 6th.

No better way to lock in support than with a major beat. Yes, it's short-term thinking but beats and price spikes are euphoric.

English

JUST IN: 🇺🇸 President Trump says Elon Musk will face "very serious consequences" if he funds Democrats.

English

Joel Li retweetledi

Abruptly ending the energy tax credits would threaten America’s energy independence and the reliability of our grid - we urge the senate to enact legislation with a sensible wind down of 25D and 48e. This will ensure continued speedy deployment of over 60 GW capacity per year to support AI and domestic manufacturing growth.

English

Joel Li retweetledi

Joel Li retweetledi

@Teslarati Not correct. We are building a production line to enable 1000/month Optimus production, but that is still many months away.

English

@SawyerMerritt $7500 accounts for more than 10% of an average EV.

I do hope the EV tax credit could stay.

English

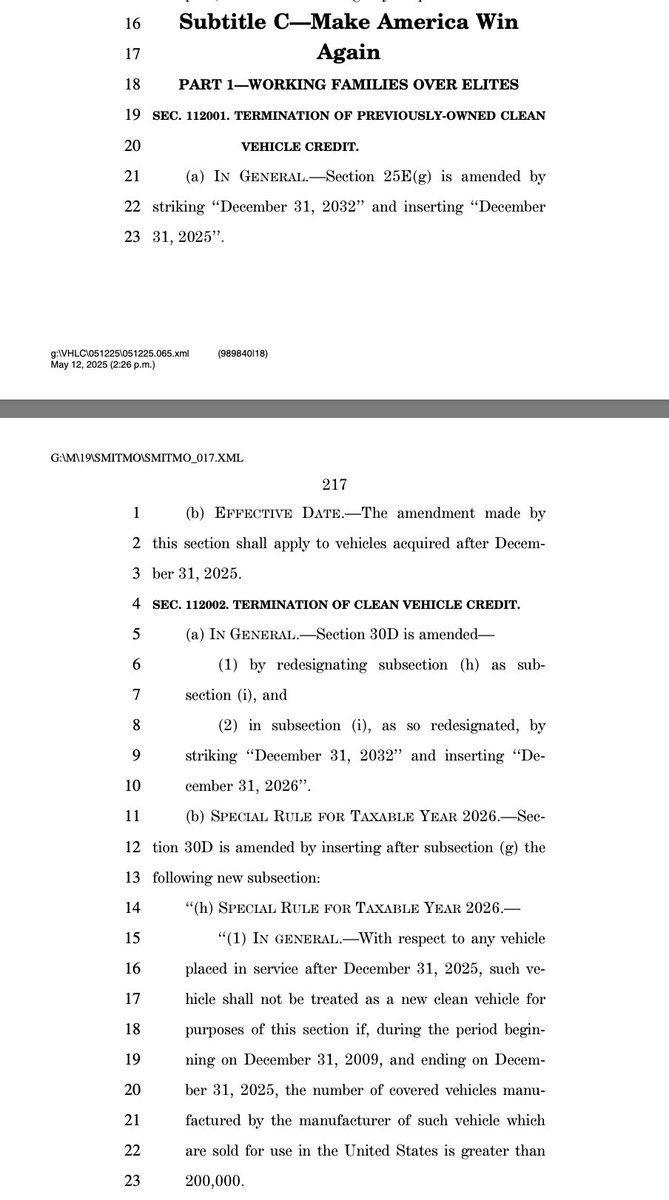

BREAKING: Republicans in Congress are looking to end the $7,500 Federal EV credit on December 31, 2025, along with the $4,000 previously-owned clean vehicle credit, according to new bill text just released.

"With respect to any vehicle placed in service after December 31, 2025, such vehicle shall not be treated as a new clean vehicle for purposes of this section if, during the period beginning on December 31, 2009, and ending on December 31, 2025, the number of covered vehicles manufactured by the manufacturer of such vehicle which are sold for use in the United States is greater than 200,000."

Republicans also want to end the Clean vehicle credit, Commercial clean vehicle credit and alternative fuel vehicle refueling property credit on Dec 31, 2025.

This is according to a new draft of the bill. Details and timeless could certainly change. This bill would still need to pass the House and Senate to enact these changes.

Full bill text: docs.house.gov/meetings/WM/WM…

English

JUST IN: 🇺🇸🇨🇳 Treasury Secretary Bessent says China tariffs could always return to April 2 levels.

English

FSD mistakenly follows a bus into a stop, and when the bus stops, FSD must swerve left to avoid it. 😂

English

Joel Li retweetledi

Joel Li retweetledi

A new adventure awaits for the XPENG X9!

The right-hand drive X9 has a one-way ticket to Thailand as the first stage of its global expansion. Join EV.com now to find out more about the X9’s journey to Thailand and beyond!

EV.com@EVcom

There's something special about these EVs...👀 #ev #ev2025 #expansion @XPengMotors

English

Joel Li retweetledi

The Best Electric Wagon? Meet the NIO ET5 Touring. @NIOGlobal #ElectricWagon #EVLife #WagonsOfInstagram #ElectricVehicles #EVReview #electriccar #NIO

English