Kate Terry

809 posts

Kate Terry

@kateterry

Co-founder & CEO @SurroundInsure. I build beautiful insurance products. #insurtech #insurance

Cambridge, MA Katılım Ağustos 2008

847 Takip Edilen798 Takipçiler

Kate Terry retweetledi

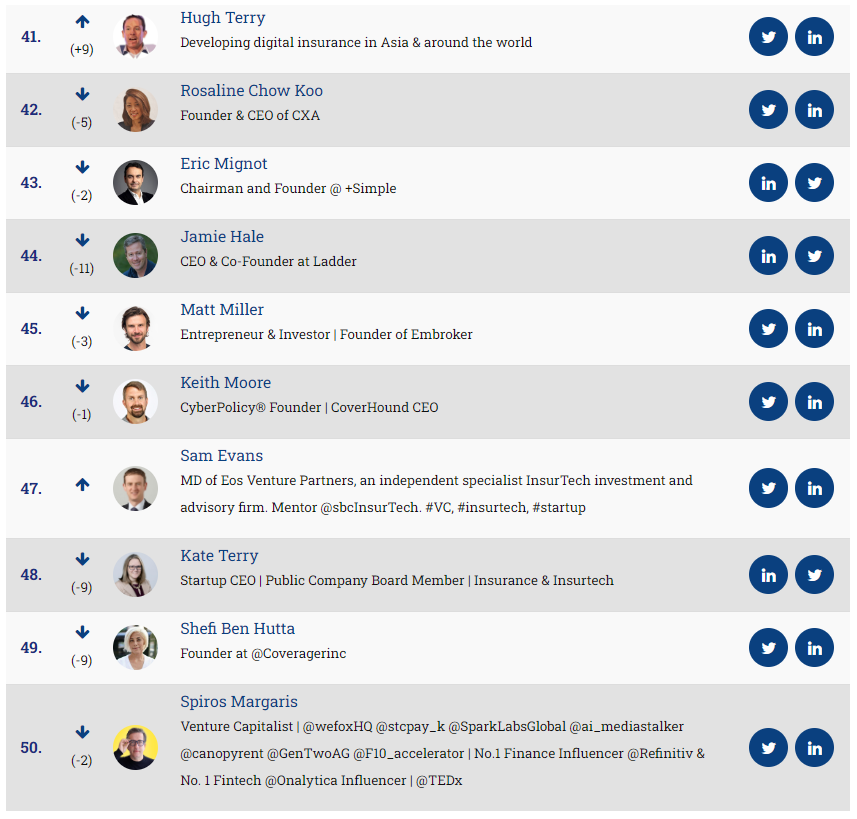

July's #50insurtech influencer list is out now! See here for the complete top: insurtechnews.com/influencers

Congrats @DigitalInsurer @RozChowKoo @MignotEric @halejamie @matlasmiller @M00RE @Sam_C_Evans @kateterry @shefibenhutta @SpirosMargaris

#insurance #insurtech

English

@skylarromines The fancier the chocolate, the worse it tastes. Cheap Easter bunnies and Hershey's Kisses are the best.

English

Hey - who wants to fight about something?

Do it in my comments section. Thanks, new algo.

English

@Nick_Lamparelli @ErikLinnartz The three largest carriers in the US know as much about you as the NSA. This comment is beyond uninformed- border level propaganda.

English

Now that AI tools have become more available and common, people fear that $LMND has no moat.

But what creates a moat in the age of AI?

Data!

This is why I think no company will be able to compete with Lemonade in insurance👇

AI basically means using statistics to predict the next step. To get accurate statistics, you need data. The more data you have the better your predictive model can be.

Large insurance companies have almost zero data on their customers. They might have some basics like an address, marital status and a name, but only the agents that work to obtain the clients have more information. So even if large companies build the perfect AI model, they will not be able to differentiate very much between customers

Newer insurance companies like $LMND, $ROOT, $HIPO, Trōv, Clearcover and Embroker can obtain more data. But as far as I am aware, none of them offers a complete list of insurance products like Lemonade, and all products require (in part) their own data collection. This means Lemonade has a head start in data collection.

Overcoming a head start in data collection can only be achieved by taking on more customers faster, but if you don’t yet have the statistics to know how to price, this can be extremely expensive because you might underprice heavily and lose a lot more money on claims than you have obtained in in force premium.

So what is the moat exactly?

Newer insurance companies would have to invest unreasonable amounts of money to obtain a lot of customers while still losing money on them. And incumbent companies would have to change their business structure completely. Both are unrealistic. Especially since $LMND trades for close to its cash position, an investor with a lot of money would probably be better off just buying a big chunk of the $LMND stock.

Let me know if you agree with this take. I am curious to expand my understanding of this stock!

English

@ErikLinnartz @dangerquenk We had this specific piece of data available in my first insurance product management job in 2005, in a graphical interface that didn’t require business users to write SQL queries…

English

$LMND collects more data per customer. The insurance giants have had more customers for more years so they might have more data in total, but a lot of the detailed information is stuck at the agent. For example, how much time between entering the room or website and taking the policy is potentially important data to understand how careful someone is.

English

@ErikLinnartz This is…a really big misunderstanding of what kind and how much data large insurance carriers have. When you include recent-ish historical data, there a big handful that likely have two orders of magnitude more data than Lemonade. And lots of data scientists and engineers.

English

Remote work as a precursor to using gen AI open.substack.com/pub/katescover…

English

@Nick_Lamparelli I can still hear that really satisfying noise they made.

English

@kateterry Omg! As a kid those were awesome. There was Mitchel’s dept store in downtown Haverhill that used those tubes into the 80’s

English

How much does customer experience lag behind price when it comes to insurance sales? Let's put it this way...customers will use carrier pigeons, fax machines, USPS, walking, dog sleds, carrier tortoises and more over a good digital experience, if it will save them money!

English

@BillyJura @ProRiskMgmt It’s a pretty good match with per capita income by county.

English

@Ryan_Hughes_Ins That assumes the model vendor knows 1) agencies aren’t carriers 2) AMSes exist 3) download is a thing. 75% of the time, they seem to know none of the above 🤷♀️

English

Agreed. I see a lot of “we have models that can help automate processes.” I don’t believe the models alone have much value. The value proposition should include a specific workflow that your model solves for.

For example:

“We can use models to automate data extraction from policies.”

Should read

“For policies that don’t download, our models can decrease by 80% the time that your CSR’s spend inputting policy information into your AMS.”

Clinton Houck@ClintHouck

Every Insurtech that's also "AI", develop unique value propositions. "We have a proprietary model, and can get to 95% accuracy" are now table stakes in every pitch.

English

@BillyJura Amen. Especially daylight savings time (but also term limits!)

English

Worst part of the eclipse so far? The mosquitos are out in force…

English

@BrandonDendas Aw thanks! It’s all home grown, so I’m pretty darn proud of our team!

English

@kateterry Thanks for the feedback, @kateterry! BTW your company is doing some great things on the Local SEO front. 👌🏼

English

❗Looking to the Insurance X Community for feedback on this one❗

So I've been sending these personalized videos to insurance agency principals and owners via email & Linkedin.

What are your thoughts on this approach and the quality of the content?

(aka. roast me in the comments below.)

English

@jeffroth77 @ClintHouck This. Can stay at home through the progression of dementia, for example, for a much longer time if there’s a spouse to provide 24hr supervision (with help, 🤞)

English

@ClintHouck Or does it just mean you are more likely to have a caretaker when you are old? Hence, policy less likely to be triggered.

English

I've been looking at LTC policies recently... Came across a company that gives you a 5% discount if you're married... Guess it does extend life expectancy.

Manhattan, NY 🇺🇸 English