Sabitlenmiş Tweet

haYN Capital

615 posts

@killapabkai

Look for value where value can be found. posts NFA. please challenge any of my posts/ideas Check out my Substack: https://t.co/WOED4chq9T

“Samsung adviser warns the AI-driven memory super-cycle may lose momentum by 2028 as Chinese chipmakers aggressively expand DRAM and NAND production. “ scmp.com/tech/tech-tren…

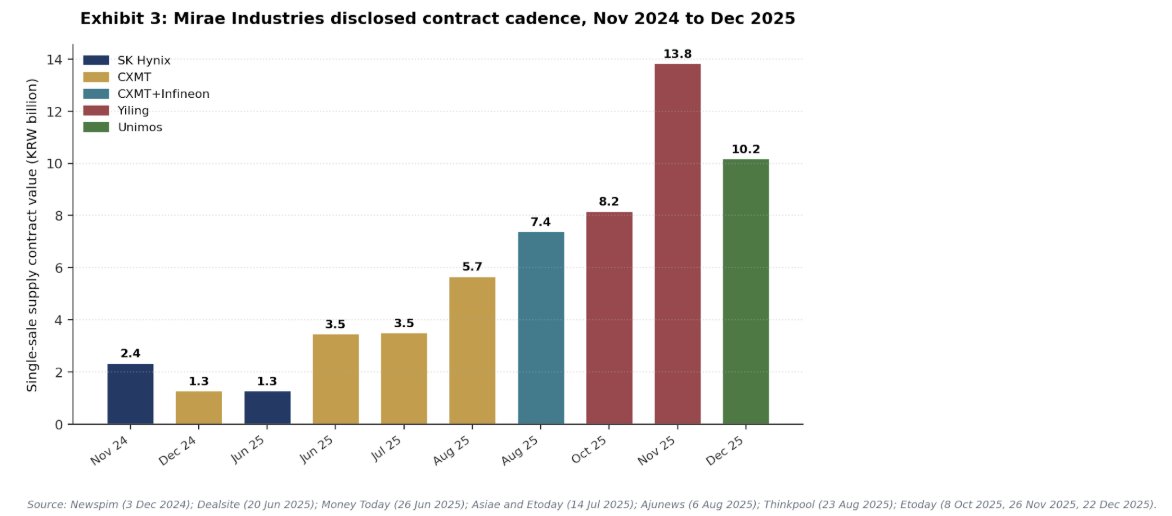

$025560.KS Mirae just reported a monster Q1: Revenue: ₩20.7B, +336% YoY Op profit: ₩4.9B, ~15x YoY Net income: ₩5.9B At ~₩111B mkt cap, that’s ~7x LTM earnings, ~5-6x blended 2026, and ~4.7x if Q1 annualizes. Korean semi equipment comps trade far richer.

Risk Management 101 | Episode 5: When Books Get Chaotic (22m) When positioning gets whippy, most people freeze. The best PMs have a process In my intro series Episode 5 I break down; how to know if your thesis is actually broken (vs. just noise), how Tier 1 multi-manager PMs handle "red boxes" when positions go against them, and the four things I check every single day 🎯 Timestamps 03:11 Is my thesis broken? 06:15 Multi-manager "red boxes" 12:26 Four things I watch every day 16:50 What to actually do **Many of you asked for a YouTube channel. It's under construction. Organized playlists on way**