Sabitlenmiş Tweet

krupal patel

637 posts

krupal patel

@krupalp55304514

investor & trader in stocks market.✌️ jay shree krishna ❤️. To learn about Trading & investing watch my YouTube video. 👇👇👇👇👇

Katılım Aralık 2020

146 Takip Edilen35 Takipçiler

@piyush_trades Itna to mere pappa ka aek tukda land (zamin) ka worth hai🤣

Filipino

I’m worth ₹12.5 Crores (21 yrs old)

I received ₹48 Lakhs today.

English

Once you start controlling your emotions trading is blessing for you ❤️

English

English

@baapofchart Bhai Apke Followers ka routine: 👇

Getup ☀️

Ask for Refund 💵

Sleep 😴

Repeat 🔁

English

My Daily Routine :

5 Am : Wake up

5 Am to 5 : 30 Am : Prayer 🤲

5:30 am to 6 :30 Am : Cycling 🚴♀️ and exercise

6:30 Am to 7 Am : Fresh up

7 Am to 8 Am : Trading Preparation

8 Am to 9 Am : Breakfast, making YouTube Videos and Tweet .

9:15 Am to 3: 30 PM : Trading and live classes

3:30 Pm to 5 PM : Power nap 😴

5 Pm to 6 PM : Cycling and Chai ☕️

6 Pm to 8 PM : Zoom meeting

8 PM to 9 Pm : YouTube videos and rest time .

9 Pm to 11 PM : Giving time to myself for learning and family time .

Around 11:30 Pm : Sleeping time .

Share your Daily Routine.

English

Ugro Capital Ltd.

Market Cap : ₹ 2,536 Cr.

10Yrs Sales CAGR : 66%

10Yrs PAT CAGR : 37%

ABOUT THE COMPANY

UGRO Capital was incorporated as Chokhani Securities in 1993 and subsequently listed on the BSE in 1995. Shachindra Nath, the Executive Chairman and Managing Director, acquired the Company in July 2018, and the company was subsequently renamed and recapitalized as UGRO Capital Limited.

The company is a Data Tech Lending platform which solves the small business credit gap in India with the help of its formidable distribution reach and Data-tech approach. The company is backed by marquee Private Equity funds and family offices.

It is a technology focused, small business lending platform. It is focused on addressing capital needs of small businesses by providing customized loan solutions. It strives to build a strong SME financing platform based on sectoral understanding supplemented by a fully integrated technology and analytics platform.

The company’s ability of Data Analytics and strong Technology architecture allows for customized sourcing platforms for each sourcing channel. GRO Plus module which has uberized intermediated sourcing, GRO Chain, a supply chain financing platform with automated end to end approval and flow of invoices, GRO Xstream platform for co-lending, an upstream and downstream integration with fintechs and liability providers and GRO application to deliver embedded financing option to MSMEs.

The credit scoring model GRO Score (2.0) a statistical framework using AI / ML driven statistical model to risk rank customers is revolutionizing the MSME credit by providing on-tap financing like consumer financing in India UGRO has pioneered the ‘Lending as a Service’ (LaaS) model in India and has effectively operationalized Co-lending relationship with various Large Public Sector Banks and large NBFCs and built a sizeable LaaS book of more than 15% of its AUM through the GRO Xstream platform.

Business area of the company

The company is engaged in the business of lending and primarily deals in financing MSME sector with focus on Healthcare, Education, Chemicals, Food Processing/FMCG, Hospitality, Electrical Equipment & Components, Auto Components and Light Engineering segments.

Loan products

Business Loans- Secured

Business Loans- Unsecured

Plant & Machinery Loan

Supply Chain Finance

GRO X

INVESTMENT THESIS

Robust Technology Framework

Differentiated Credit Approach

Formidable Distribution Strength with ability to cater to every credit of MSME

Strong Corporate Governance Standards

Experienced Leadership Team

Lending as a Service

Operationalizing GRO Xstream Platform to transition the business to LaaS Model

1.Robust Technology Framework

UGRO has developed proprietary technology sourcing platforms which are customized for each distribution channel at the heart of which lies its Business Rule Engine (BRE) which is product agnostic and distribution channel agnostic and is purely based on behavior of end customers. All customer data is stored in a data lake which can be used for any kind of machine learning model.

2.Differentiated Credit Approach

UGRO adopted a sectoral lending approach to identify homogeneity among the heterogeneous MSME segment. It juxtaposed Cash flow-based banking analysis and repayment behavior of MSMEs to the sector in which they operate to develop their proprietary AI / ML based scoring Model GRO Score. GRO score is built on the tripod of data that is Banking, Bureau and GST to analyze 20,000+ data points and deliver < 60 mins credit decisioning

3.Formidable Distribution Strength with ability to cater to every credit of MSME

UGRO was formed with the intent to cater to all credit needs of every MSME. It offers multiple products namely Secured LAP, Affordable LAP, Micro Enterprises Loans, Machinery Loans, Unsecured Business Loans and Supply Chain Financing to address various credit needs of MSMEs. It operates through four broad distribution channels to service the entire MSME segment right from Prime customers (10% - 12% ROI segment) to Micro customers (25+% ROI Segment).

4.Strong Corporate Governance Standards

Creating an institution that is built to last requires strong corporate governance standards. U GRO was founded with the philosophy of being institution owned, board controlled and management run. U GRO Capital’s Board is majorly independent. The Governance standards are further strengthened by strong policies and processes enshrined in the Articles of Association.

5.Experienced Leadership Team

Company has hired industry leaders that have a proven track record of delivering results & they possess the right acumen necessary in the build out phase of any organization. Setting the right team in place has helped the company tide through the crisis effectively. Business operations are independently managed by the CXO team which makes UGRO truly a professionally driven organization.

6.Lending as a Service

UGRO is pioneering Lending as a Service (LaaS) business model in India by successfully harnessing and operationalizing Co-lending Partnerships with multiple Banks and NBFCs. Currently the Company has operationalized 10+ Co-lending partnerships across large Public Sector Banks and NBFCs.

7.Operationalizing GRO Xstream Platform to transition the business to LaaS Model

GRO Xstream platform to ultimately connect providers of capital with originators of loans and facilitate multiple liability partnerships in the form of Co-lending, Co-origination, Direct Assignment and others. GRO Xstream would be powered by UGRO Score and would support Multi Rule Engine basis requirements of various lenders.

INDUSTRY OVERVIEW

Overall credit growth for FY22 is estimated to be 8.3%, the same is expected to be in the range of 8.9% - 10.2% in FY23. Improvement in profitability of BFSI companies for FY23 is anticipated to improve on the back of higher credit growth and decline in credit provisions. Disbursement growth bounced back to pre-covid level across multiple retail products along with recovery in the corporate segment. Corporate segment growth was primarily driven by improved utilization levels and working capital requirements. MSME segment has seen robust growth of over 30% on the back of robust recovery in overall business activity and extension till March 2023.

Lending to MSMEs is well supported by various measures taken to formalize the sector. We observe more GST compliance with the GST collection amount increasing

by 26.9% in FY22. Digital payments are a large part of the Indian banking system, digital transactions grew close to 90%, from 232,000 to 430,000 over FY19 to FY21, primarily led by UPI. The value of digital payments in India is expected to touch $1 trillion by FY26, as compared to

$300 billion in FY21. As per the economic survey of FY22 over 66 lakh MSMEs registered on Udyam portal and 95% of those were micro enterprises.

BUSINESS OVERVIEW

UGRO’s mission is “To Solve the Unsolved'' - India’s $ 600+ Bn SME credit availability problem. The company lends exclusively to MSMEs and caters to all the borrowing needs through a diverse range of product offerings like Secured LAP, Affordable LAP, Micro Enterprises Loans, Machinery Loans, Unsecured Business Loans and Supply Chain Financing the lend to customers right from the prime segment (<10% interest rates) to the micro

enterprises (20-25% interest rates). Additionally undertake co-lending with FinTech and smaller NBFC Partners to expand reach and lend to the micro enterprises through the length and breadth of India. While having maintained a keen focus on the initial prime / near-prime target segment, the company has also worked towards addressing a broader demographic as per efforts to solve India’s MSME credit gap.

UGRO Capital Found Philosophy (DataTech Approach)

U GRO capital was incorporated on the belief that MSME credit gap in India could be solved by use of Data and Technology. Back in 2018 the management was of the opinion that MSME lending market would gravitate towards being an on-tap consumer lending market and this would be heavily facilitated by the rapid scale of digitalization prevalent in the Indian Economy. The management envisioned that the digital wave would democratize data through India stack including ocen and Account Aggregation Network which would support new age underwriting business models for MSME lending and in turn reduce customer TAT.

Use of Data Analytics

The key to developing such an underwriting framework was an in -depth understanding of MSME business models and thus U GRO decided to adopt a sectoral approach for the same. It shortlisted 8 sectors after careful filtration of 180+ sectors in an 18-month process involving extensive study of macro and microeconomic parameters carried out alongside market experts like CRISIL eight shortlisted sectors include Healthcare, Education, Chemicals, Food Processing/FMCG, Hospitality, Electrical Equipment and Components, Auto Components and Light Engineering. The company further narrowed down on selected sub-sectors based on contribution to overall sector credit demand and risk profiling.

For very small businesses we released that their behavior was influenced by cash flow availability rather than broad sector trends and thus Micro Enterprises was adopted as the 9th sector. These 9 sectors together constituted 50% of SME credit demand and thus was a sizable opportunity to operate within MSME lending.

Use of Technology

U GRO has recognized the importance of this digital transformation and has been at the forefront of its adoption, It is one of the first implementers of ocen in India, and have designed & implemented Government e- Marketplace.

Company has developed proprietary technology platforms for each distribution channel which are customized to support various business needs.

GRO Plus: Supports branch-based business and is designed to support customers onboarded in metro cities through intermediaries. It has completely integrated every element of underwriting digitally and allows intermediary to use application directly for onboarding, servicing and training

GRO Chain: Specifically designed for catering to supply chain business and supports real time disbursement. Suppliers can upload invoices on this module which can be in turn approved by the anchor on the module itself, real time disbursement can be made available against the invoices approved by anchors.

GRO Direct: Platform built to allow non-intermediated loan applications from eligible SMEs. The company plan to launch GRO X app which would allow SMEs to directly apply for loans through their mobile phones

GRO Xstream : Currently being used as a sourcing module for Partnership and Alliances channel however the same will eventually evolve into a marketplace powered by BRE connecting Asset originators on one hand with liability partners on the other. It currently allows seamless API integrations with the systems of each of the partners & hence allowing the Company to achieve record TATs.

Business Updates

1) For every 100 applications, 30 loans are disbursed.

2) Early warning signal for the stressed customer is not the bureau, not the banking but the GST. Bureau typically takes 4‐5 months lag before stress is reported. Banking early warning is a little better but still, one doesn't know till the cheque bounces. In GST, the moment the sale starts going down, that is the first and your primary early warning signal. This is the Company's hypothesis and with this,it built and included that as a major parameter in GRO Score.

3) For collection, the company has built out a large litigation team and early warning system developed by a data analytics team which gives warning signals to in-house call centers.

4) 56% of loan origination is done through intermediaries.

5) UGRO Capital has recently launched its first brand campaign, a one‐of‐its‐kind 3D animation film, Fund Island for the launch of its most awaited digital solution for small businesses. UGRO Capital’s newly launched GRO X App enables MSMEs across India to obtain collateral‐free instant credit for immediate working capital requirements and to manage their financial liquidity. This app‐based lending, which the Company has launched, is basically to serve the needs of very small merchants.

Expansion Plans:

•UGRO plans to open 20-25 micro enterprise branches in the first two quarters, eventually reaching a total of 250 branches across the country in the next 24-30 months.

•U GRO aims to do specific need-based lending in the future, but for now, it is not defined for the end purpose.

•UGRO plans to steadily increase the percentage of off-book AUM and reach a 50-50 balance sheet by 2025.

•U GRO has launched its direct-to-customer model and has 66 lenders on board to support its liability engine.

•U GRO's target of INR 20,000-plus-crores AUM by FY '25 is still in line, and they are building a generational institution for India.

English

🔴My Portfolio down by 2% Today

🤔What about you ?

English

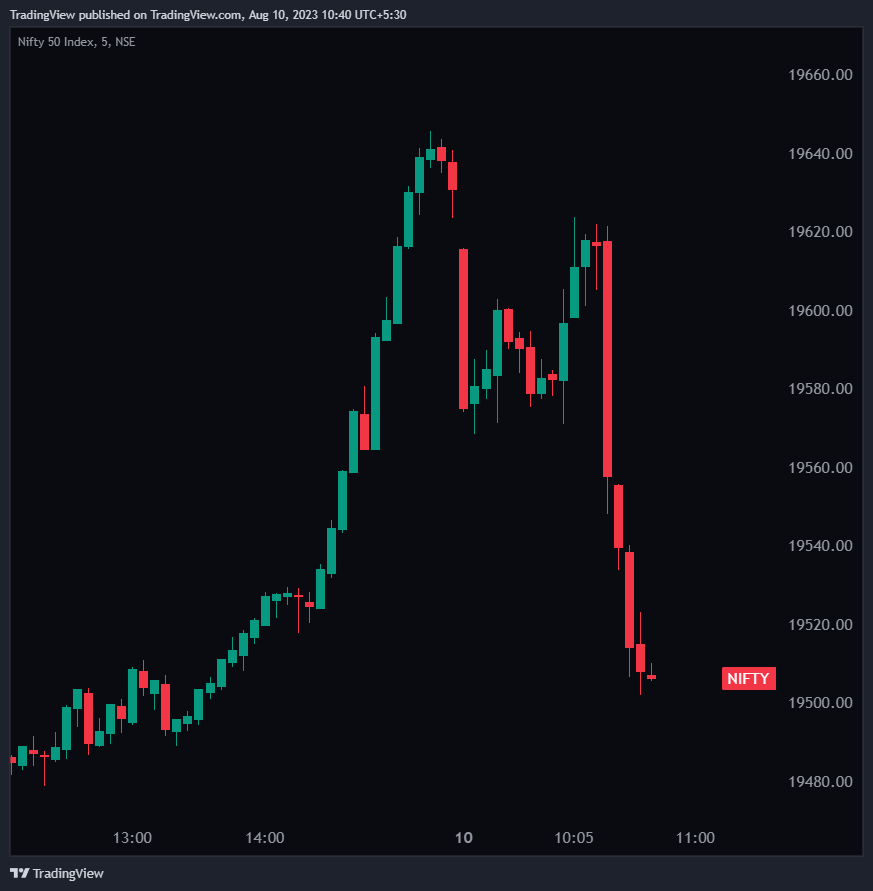

Will #Nifty50 hit new all time high tomorrow?

English

You have : ₹1000000 Only

You can invest only in 1 Stock

Which stock it will be & why ?

English

krupal patel retweetledi

Hello Fam,

You can find 3 Stock Screeners Below:-

1. Breakout Stocks

chartink.com/screener/stock…

2. Potential Breakout Stocks

chartink.com/screener/stock…

3. NR-7 Stocks

chartink.com/screener/nr-7-…

Like and RT To Reach max people.

BOOKMARK IT.

#Trading #Swingtrading #Investing

English