LJH

1.3K posts

LJH

@kyle_ljh

create your bio page on https://t.co/7JzWLcBFau

Katılım Aralık 2025

1.3K Takip Edilen1.1K Takipçiler

English

$MU $DRAM $SNDK Memory investors. Write this down.

"Today, Non-HBM DRAM has actually higher profitability than HBM. NAND has strong profitability as well."

-@MicronCEO on CNBC.

The entire portfolio is firing. Bears are in denial.

Trade Whisperer@TradexWhisperer

$MU @MicronCEO on CNBC. Three things the bears need to hear. One. Non-HBM DRAM is more profitable than HBM today. The entire portfolio is firing. Two. A meaningful supply ramp does not even begin until 2028. And even then, supply will not catch demand for a considerable period of time. Three. Revenue grew nearly $10B from Q1 to Q2. Another $10B from Q2 to Q3. "Bringing up supply is a very long lead item. DRAM needs new capacity. New capacity takes new construction. Construction is a long lead time item. So earliest that we see in the industry meaningful ramp ... gradually happen overtime starting in 2028 timeframe. So I do not see supply catching up to demand for considerable period of time here." "Today, Non-HBM dram has actually higher profitability than HBM. NAND has strong profitability as well, so we are managing the mix of the business, keeping in mind long-term considerations and absolutely, data center is the biggest growth driver. We are well positioned with our product portfolio, including HBM, to address these demand trends."

English

@YahooFinance Since when this is new?

Its been like that for awhile now.

English

$NVDA is trading lower after CEO Jensen Huang said the company now has zero market share in China. 📉 finance.yahoo.com/sectors/techno…

English

WSJ reports Goldman Sachs will contribute roughly $150 million as a founding investor.

English

@pizzapastamcd1 可是上游还有什么合适的车吗,存储,芯片,代工厂,通信和服务器都涨翻了。我看好的就一个海力士sk的adr ipo过段时间,剩下我就买云服务了

中文

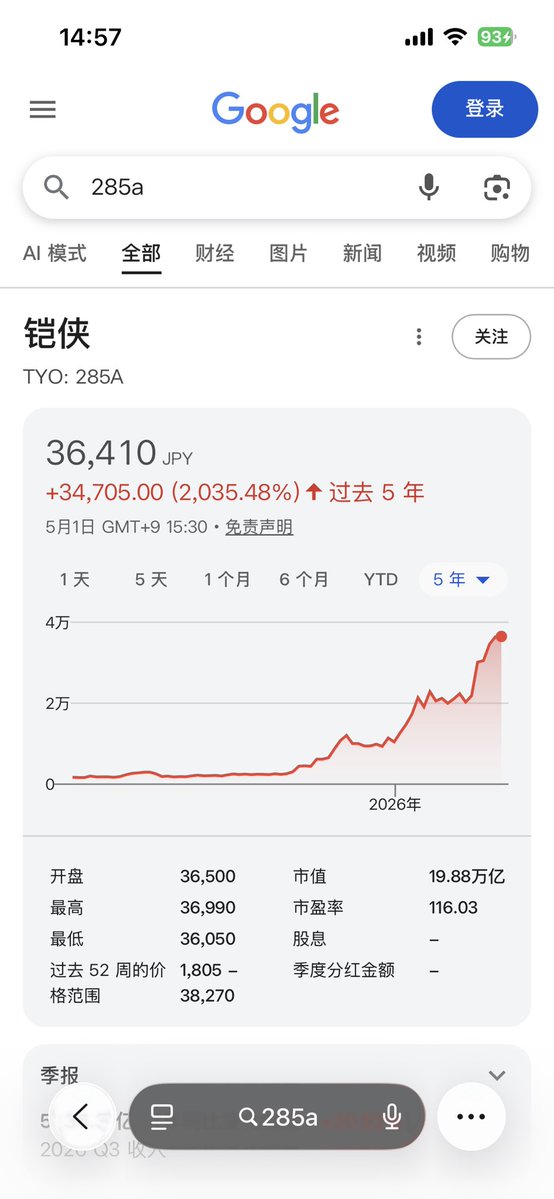

凯侠才是最疯狂的那个,不买半导体你今年回报10%左右甚至更低,买了你就在泡沫和大回调之间摇摆

決算グラフ化芸人|統計を学んでいたはずの化学系技術者@ChemStat66667

intelの株価ヤベーなと思って1年の株価パフォーマンスを調べたらもっとヤバいのがいっぱいいた。 相対的にNVIDIAがオワコンに見えて引くレベル。

中文

LJH retweetledi

JUST IN: China orders its companies to ignore US sanctions on refiners linked to Iran.

English

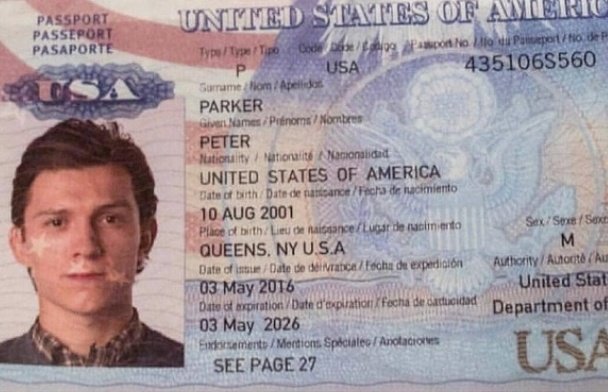

May 3, 2026

Peter Parker's passport expires today

English

Anthropic is in talks to buy inference chips from UK startup Fractile.

This isn’t a chip-supply story. It’s a margin story.

Training gets the headlines.

Inference is where the money goes.

Every Claude prompt, agent task, and enterprise call = ongoing compute demand with no ceiling.

Fractile’s chips are built for efficient AI inference — potentially available next year.

What Anthropic really wants:

→ Cheaper inference

→ More supply options

→ Less leverage for Nvidia, Google & Amazon

Control the inference. Control the margin.

That’s what scaling an AI lab looks like now.

English

JUST IN: Trump says the U.S. will withdraw “a lot further than 5,000” troops from Germany.

English

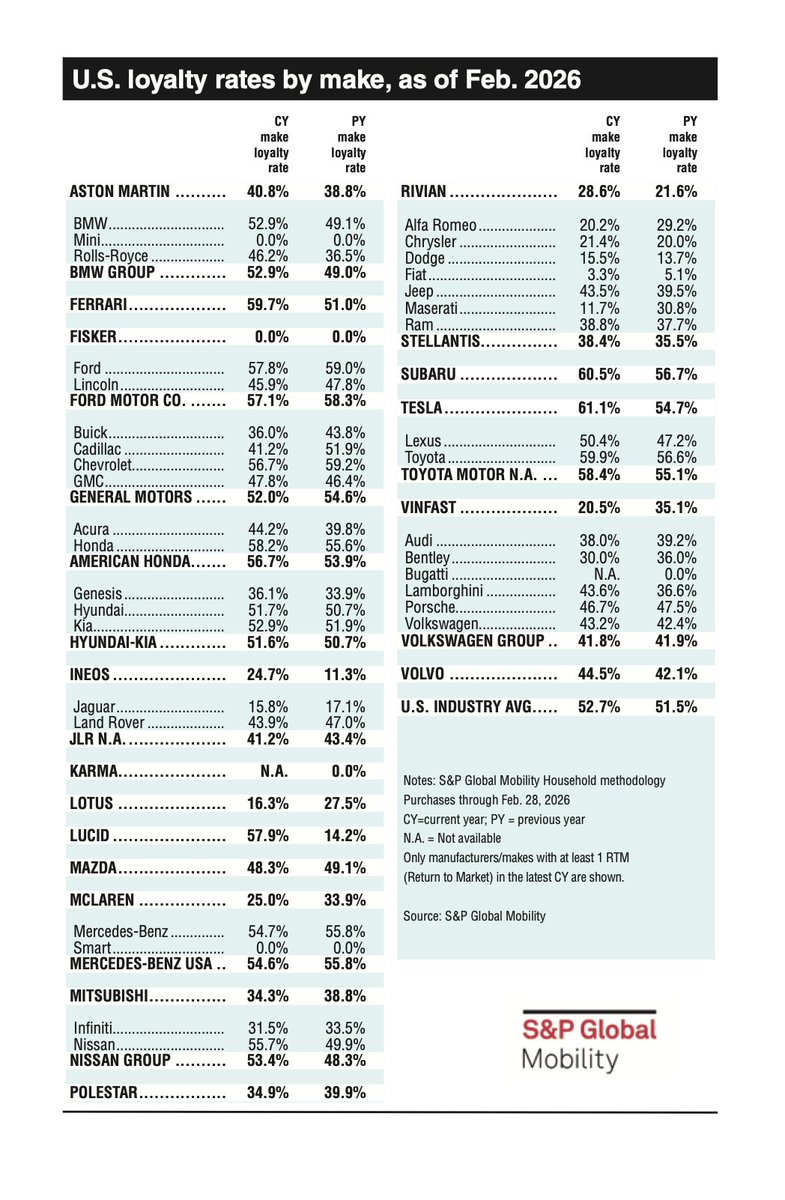

U.S. loyalty rates by make, February 2026

1. Tesla — 61.1%

2. Subaru — 60.5%

3. Toyota — 59.9%

4. Ferrari — 59.7%

5. Honda — 58.2%

6. Ford — 57.8%

7. Lucid — 57.9%

8. Chevrolet — 56.7%

9. Nissan — 55.7%

10. Mercedes-Benz — 54.7%

11. BMW — 52.9%

12. Kia — 52.9%

13. Hyundai — 51.7%

14. Lexus — 50.4%

15. Mazda — 48.3%

16. GMC — 47.8%

17. Porsche — 46.7%

18. Rolls-Royce — 46.2%

19. Lincoln — 45.9%

20. Volvo — 44.5%

21. Acura — 44.2%

22. Land Rover — 43.9%

23. Lamborghini — 43.6%

24. Jeep — 43.5%

25. Volkswagen — 43.2%

26. Cadillac — 41.2%

27. Aston Martin — 40.8%

28. Audi — 38.0%

29. Ram — 38.8%

30. Buick — 36.0%

31. Genesis — 36.1%

32. Mitsubishi — 34.3%

33. Polestar — 34.9%

34. Infiniti — 31.5%

35. Bentley — 30.0%

36. Rivian — 28.6%

37. McLaren — 25.0%

38. INEOS — 24.7%

39. Chrysler — 21.4%

40. Alfa Romeo — 20.2%

41. VinFast — 20.5%

42. Lotus — 16.3%

43. Jaguar — 15.8%

44. Dodge — 15.5%

45. Maserati — 11.7%

46. Fiat — 3.3%

47. Mini — 0.0%

48. Smart — 0.0%

49. Fisker — 0.0%

Eesti

How are you @CitronResearch

Citron Research@CitronResearch

Citron is Short $SNDK — They Don't Ring a Bell at the Top We don't need Anthropic to announce they're making NAND. Samsung is already the 800-pound gorilla, and they've been running this playbook for 30 years. While TV pundits pound the table herding retail into cattle cars, Western Digital, the long time investor, sold a significant portion of its holdings days ago, 25% lower. Ask yourself why. Because they know the cycle is approaching a peak, and they're not waiting for the bell. The market is pricing SanDisk like it's $NVDA. There's one problem: NVIDIA has a moat. SanDisk sells a commodity. We've seen this movie before 2008, 2012, 2018. It's never different this time. Memory is a cycle, and cycles peak. Samsung has a 30-year history of choosing market share over margins. They wait for pure-plays like SanDisk to get comfortable at 50% gross margins, then flip the switch. But this time it's worse. Every $SNDK bull should read attached article Samsung just told the world they won't sell anything under 50% margins and they're moving their best chips into the same premium SSD market SanDisk calls home. They're not just the capacity gorilla anymore. They're going after SanDisk's best customers with cheaper, newer technology. And the only thing keeping supply tight right now? Samsung's temporary yield problems in another product line. That bottleneck has an expiration date. With double the capacity of the 2018 peak waiting in the wings, this "shortage" is a supply mirage that can vanish in a single earnings call. Hockey shout-out: Shorting $SNDK is skating to where the puck is going. By the time the cycle normalizes, this stock will already be much lower. technetbooks.com/2026/02/samsun…

English

🇺🇸 15 years ago today, the United States killed Osama bin Laden.

English